Welltower (WELL) Q1 2026 earnings summary:

Financial Highlights

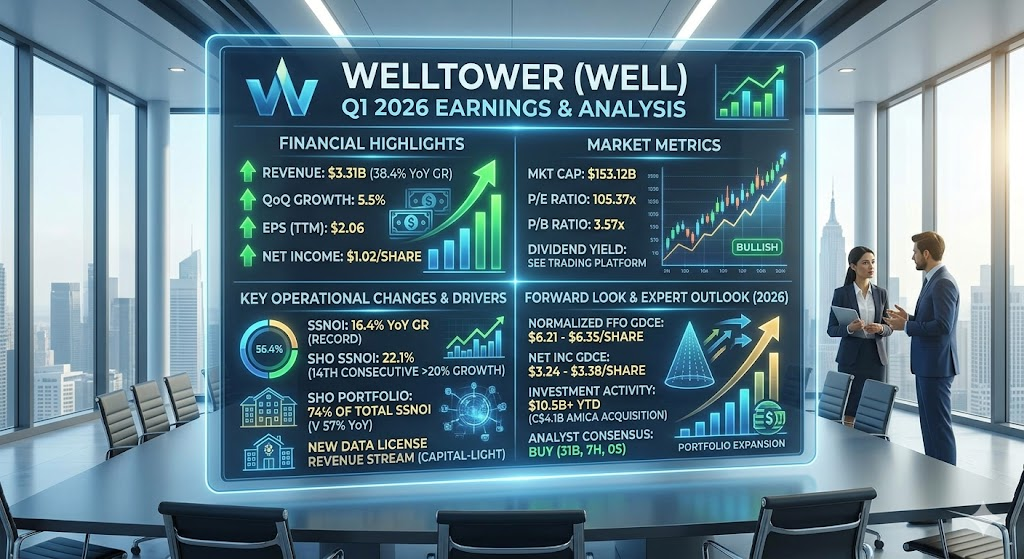

- Revenue: 3.31B

- QoQ Growth: 5.5%

- YoY Growth: 38.4%

- EPS (TTM): 2.06

Market & Valuation Metrics

- Market Cap: 153.12B

- P/E Ratio: 105.37x

- P/B Ratio: 3.57x

- Dividend Yield: Please refer to your trading platform for real-time data.

Welltower (WELL) reported exceptional results for Q1 2026, characterized by record operating metrics, aggressive capital deployment, and an upward revision of its full-year guidance.

1. Key Financial Highlights

- Earnings and Revenue:

- Revenue: $3.35 billion, an increase of 38% year-over-year.

- Normalized FFO (Funds From Operations): $1.47 per diluted share, representing 23% year-over-year growth.

- Net Income: $1.02 per diluted share.

- Operating Performance:

- Total Portfolio Same-Store NOI (SSNOI): Grew 16.4% year-over-year, the highest in the company’s history.

- Seniors Housing Operating (SHO): SSNOI surged 22.1%, marking the 14th consecutive quarter of growth exceeding 20%. Organic revenue growth reached 9.5%, fueled by a 370 basis point increase in occupancy and 5.0% growth in Revenue Per Occupied Room (RevPOR).

- Margin Expansion: Operating margin increased 320 basis points to 30.9%, driven by tight expense control (only 0.4% growth in expense per occupied room).

2. Strategic Changes & Operational Developments

- Accelerated Investment Activity: The company reported $10.5 billion in year-to-date investment activity. This includes $3.2 billion closed in Q1 (37 of which were off-market) and an additional $7.3 billion either closed or under contract subsequent to quarter-end.

- Portfolio Enhancement: On April 1, 2026, Welltower completed the C$4.1 billion acquisition of a 38-property Canadian seniors housing portfolio from Amica Senior Lifestyles.

- Capital-Light Revenue Stream: A notable strategic shift is the introduction of a data science platform licensing initiative. Welltower is now licensing its proprietary models to external partners, including Public Storage and a global private equity firm, creating a new source of capital-light income.

- Balance Sheet Strength: Despite the high volume of acquisitions, the company successfully reduced its Net Debt to Adjusted EBITDA ratio to 2.7x (down from 3.3x in Q1 2025).

3. Full-Year 2026 Outlook

Following the strong first-quarter performance, management raised its full-year guidance:

- Normalized FFO Guidance: Raised the midpoint by $0.11 to a range of $6.21 to $6.35 per diluted share.

- Net Income Guidance: Revised to a range of $3.24 to $3.38 per diluted share.

- Growth Drivers: The guidance update is supported by expectations for strong SHO portfolio performance and continued accretive capital deployment.

Welltower (WELL) enters the coming quarters with significant momentum, driven by a self-reinforcing cycle of operational excellence and aggressive capital allocation. Here are the primary growth catalysts:

1. Sustained SHO Portfolio Momentum

- Operating Leverage: The Seniors Housing Operating (SHO) portfolio is the primary engine. With 14 consecutive quarters of >20% Same-Store NOI growth, the company is benefiting from favorable supply-demand dynamics. Supply remains constrained due to high construction costs and tighter financing, while demand is surging due to the aging 80+ demographic, which is expected to grow at a 5.4% CAGR through 2030.

- Occupancy Targets: The company is aggressively targeting occupancy levels toward 95%. Given that revenue growth continues to significantly outpace expense growth, the continued improvement in occupancy is expected to drive further margin expansion toward the 35% NOI margin target.

2. Accretive Capital Deployment

- Portfolio Integration: The $10.5 billion in total investment activity (year-to-date) will begin to provide a meaningful lift in subsequent quarters. Specifically, the C$4.1 billion acquisition of the Amica senior living portfolio, which closed on April 1, will contribute a full quarter of earnings starting in Q2.

- Strategic Recycling: Welltower continues its “re-investment” strategy, disposing of lower-growth outpatient and post-acute assets and redeploying the proceeds into higher-yielding, premium senior housing properties. This shift permanently enhances the quality and growth profile of the total portfolio.

3. Scaling Capital-Light Revenue

- Data Science Licensing: The newly launched data science platform is a major strategic pivot. By licensing proprietary analytical tools to external partners (such as Public Storage and global private equity firms), Welltower is generating high-margin, “capital-light” revenue. This stream requires no balance sheet risk and scales efficiently, providing a diversified earnings base outside of traditional real estate leasing.

4. Financial Flexibility as a Competitive Edge

- De-leveraging Success: By successfully reducing the Net Debt to Adjusted EBITDA ratio to 2.7x, Welltower has created significant “dry powder.” In a high-interest-rate environment, this low leverage gives the company a distinct advantage over peers, allowing them to remain the “buyer of choice” for distressed or capital-constrained sellers without relying heavily on expensive external debt financing.

Summary

The growth narrative for the upcoming quarters is shifting from pure real estate appreciation to an integrated operator-investor model. With a scarcity of new supply and a robust pipeline of high-quality acquisitions, Welltower is well-positioned to maintain its leadership in the senior housing space while utilizing its data platform to buffer earnings against traditional real estate cycles.

The outlook for Welltower (WELL) over the next year is characterized by robust earnings growth, primarily driven by strong operational leverage in its core Seniors Housing Operating (SHO) portfolio and significant capital deployment.

2026 Full-Year Guidance

Following its Q1 2026 earnings release, management raised its full-year guidance, reflecting high confidence in the company’s growth trajectory:

- Normalized FFO (Funds From Operations): This is the primary metric for REITs. The guidance was raised to a range of $6.21 to $6.35 per share (midpoint $6.28).

- Net Income: Expected to be in the range of $3.24 to $3.38 per share.

Key Drivers for Earnings Growth

The projected trajectory for the next four quarters is underpinned by the following factors:

- SHO Operational Leverage: The Seniors Housing Operating segment is expected to remain the primary engine of growth. Management anticipates Same-Store NOI (SSNOI) for this segment to grow between 16.5% and 21.5% for the year, as occupancy rates continue to climb toward the 95% target.

- Accretive M&A Integration: With $10.5B in year-to-date investment activity, the company will see full-quarter contributions from these new assets (such as the C$4.1B Amica portfolio) in the coming quarters. This scale is expected to be immediately accretive to FFO per share.

- Diversified Earnings via Data Licensing: The expansion of its proprietary data science platform into a licensing business provides high-margin, capital-light revenue. This reduces the company’s dependency on traditional real estate cycles and adds a stable, non-cyclical income stream to the earnings profile.

- Balance Sheet Efficiency: By reducing its Net Debt to Adjusted EBITDA ratio to 2.7x, Welltower has significantly lowered its interest expense burden. This financial flexibility allows the company to pursue growth opportunities without the need for dilutive equity issuance or high-cost debt in a volatile interest rate environment.

Summary

Welltower’s earnings growth is shifting from “asset accumulation” to “operational optimization and scale.” The company is effectively leveraging its industry-leading data analytics to capture higher margins than traditional competitors. Analysts generally view the 2026 earnings targets as achievable, provided that the current supply constraints in the senior housing market persist and occupancy gains continue at the projected pace.

Note: This summary is based on official company guidance and current market analysis. Investment decisions should be based on your own financial assessment and risk tolerance.

Analyzing Welltower (WELL) requires balancing its strong operational momentum against its current valuation premiums. As of late May 2026, the stock is trading near its all-time highs (around $216), and market sentiment remains largely bullish, though cautious regarding short-term volatility.

1. Market Valuation & Analyst Sentiment

- Current Standing: Trading at ~$216, the stock has seen a significant run-up over the past year. Analysts remain overwhelmingly positive, with a consensus “Buy” rating.

- Price Targets:

- Average: Analysts’ average 1-year price targets cluster in the $235–$240 range.

- High/Low: Targets range from as low as $97 (conservative outlier) to as high as $273 (optimistic bull case).

- Valuation Context: With a P/E ratio exceeding 100x, the stock is priced for perfection. Investors are paying a premium for its leadership in the senior housing space, making the stock sensitive to any misses in quarterly earnings or FFO (Funds From Operations) growth.

2. The Bull Case (Potential Upside)

The “upside” thesis is built on sustained operational excellence:

- Demographic Tailwinds: The 80+ population cohort is growing at a 5.4% CAGR. Welltower’s heavy exposure to private-pay Senior Housing Operating (SHO) assets makes it a direct beneficiary of this aging trend.

- Pricing Power & Scarcity: Limited new supply due to high construction costs and tight lending creates a “moat” around existing high-quality assets. Occupancy is trending toward the mid-90% range, and margins are expanding toward 35%.

- Strategic Transformation: The transition toward a “capital-light” model (data science licensing with partners like Public Storage) adds a non-real estate, high-margin revenue stream that could warrant a higher valuation multiple.

3. The Bear Case (Risk Factors & Downside)

The primary risks center on valuation and macro sensitivity:

- “Priced for Perfection”: Given the significant rally, any deceleration in Same-Store NOI growth (currently >20% for SHO) could lead to a sharp pullback.

- Capital Allocation Pressure: Welltower is aggressively deploying capital ($10.5B+ YTD). Investors are monitoring whether the company can continue to execute these large acquisitions without overstretching its balance sheet or relying too heavily on equity dilution, even though they have successfully de-leveraged to a 2.7x Net Debt/EBITDA ratio.

- Macro/Interest Rate Sensitivity: While Welltower is a private-pay play, rising long-term interest rates can compress REIT valuations broadly, even if the company’s internal operations remain strong.

Expert Summary

Welltower is currently in a “High Quality, High Price” category.

- For the Long-Term Investor: The fundamental outlook remains robust. The company is effectively transitioning into a data-driven operator, which differentiates it from traditional REITs.

- For the Tactical Investor: The stock is currently trading at a premium. Given the historical volatility near all-time highs, entry points should be managed carefully. If the stock retraces toward the $190–$200 support levels, it often presents a more attractive risk-reward profile for those who believe in the multi-year demographic thesis.

Key Monitoring Metric: Watch for the SHO Same-Store NOI growth in the next two quarterly reports. If this remains above 20%, it will likely continue to anchor the bull case and support a move toward the $240+ target.

Disclaimer: This analysis is based on market data as of May 2026 and is for informational purposes only. It does not constitute personalized financial advice. Please assess your own risk tolerance before making investment decisions.

Source:

- https://statementdog.com/analysis/WELL

- https://finance.biggo.com.tw/quote/WELL/financial

- https://www.investing.com/news/transcripts/welltowers-q1-2026-earnings-beat-expectations-93CH-4645791

- https://seekingalpha.com/news/4582086-welltower-outlines-2026-normalized-ffo-of-6_21-6_35-while-accelerating-10_5b-investment-pace

- https://www.prnewswire.com/news-releases/welltower-reports-first-quarter-2026-results-302756203.html

Back to Welltower page