Wells Fargo (WFC) released its first quarter 2026 (1Q26) financial results on April 14, 2026. The performance exceeded analyst expectations for EPS but was slightly soft on the revenue side. Below is a summary of the latest quarterly report:

Core Financial Data

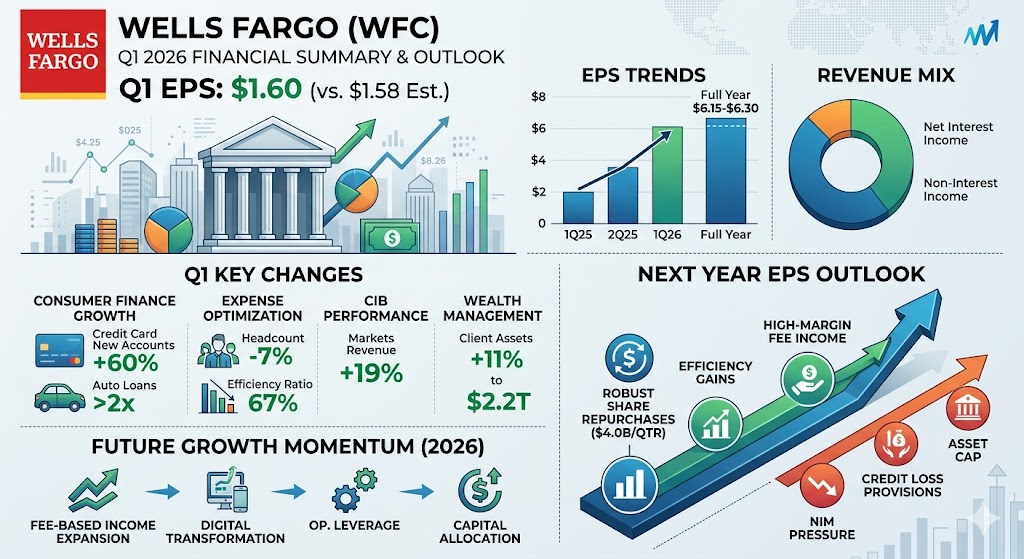

- Earnings Per Share (EPS): $1.60 (up 15% YoY), higher than the market expectation of $1.58.

- Revenue: 21.45B (up 6% YoY), slightly lower than the market expectation of 21.76B.

- Net Income: 5.3B (up 15% YoY).

- Net Interest Income (NII): 12.1B (up 5% YoY).

- Non-Interest Income: 9.4B (up 8% YoY), primarily driven by increased investment advisory fees and trading revenue.

Assets, Liabilities, and Efficiency

- Total Loans: Up 11% YoY to 996B, with strong growth in commercial loans and credit cards.

- Total Deposits: Up 7% YoY to 1.45T.

- Return on Equity (ROE): 12.2%.

- Return on Tangible Common Equity (ROTCE): 14.5%.

- Efficiency Ratio: 67%.

Segment Performance

- Consumer Banking and Lending: Revenue up 7% YoY. Credit card new accounts grew by nearly 60%, and auto loan originations increased more than twofold.

- Commercial Banking: Revenue up 7% YoY.

- Corporate and Investment Banking (CIB): Banking revenue grew by 11%, while markets revenue increased significantly by 19%.

- Wealth and Investment Management: Revenue up 14% YoY, with client assets reaching 2.2T (up 11% YoY).

Capital and Shareholder Returns

- Total capital returned to shareholders this quarter was 5.4B, including 4.0B in common stock repurchases.

- CET1 Ratio: 10.3%, within the company’s target range of 10% to 10.5%.

- Headcount: Decreased 7% YoY, reflecting ongoing expense management.

Market Reaction and Outlook

Despite the EPS beat, the revenue miss and pressure on Net Interest Margin (NIM) caused concerns regarding earnings quality. Following the release, WFC shares fell approximately 4.92% in pre-market trading. The company reaffirmed its full-year 2026 NII guidance of approximately 50B.

Based on the financial report and analysis of Wells Fargo (WFC) for the first quarter of 2026, the key changes this quarter can be summarized as follows:

Business Structure and Growth Momentum

- Strong Performance in Credit Cards and Consumer Loans: New credit card accounts grew by nearly 60%, and auto loan originations increased more than twofold, indicating significant expansion in the consumer finance sector.

- Explosion in Investment Banking and Markets: Within the Corporate and Investment Banking (CIB) segment, markets revenue surged by 19%, serving as a major engine for revenue growth and partially offsetting the pressure of slowing interest income growth.

- Expansion of Wealth Management Assets: Client assets grew 11% YoY to reach 2.2T, driving steady growth in advisory fee income within non-interest income.

Cost and Efficiency Optimization

- Workforce Reduction: Headcount decreased by 7% compared to the same period last year, reflecting the company’s ongoing execution of strict expense management and digital transformation policies to offset cost pressures from rising wages.

- Maintenance of Efficiency Ratio: Despite increased investment costs, the company maintained an efficiency ratio of 67% through staff reductions and process optimization.

Financial Health and Margin Pressure

- Challenges to Net Interest Margin (NIM): While Net Interest Income (NII) continued to grow, margin space was compressed due to rising deposit costs and shifting market expectations for interest rate cuts. This was a primary reason for the pressure on the stock price following the earnings release.

- Provisioning for Losses: To address potential economic volatility, the company maintained a cautious approach to asset quality management, particularly regarding commercial real estate and credit card loan loss prevention.

Increased Shareholder Returns

- Large-scale Buybacks: Out of the 5.4B returned to shareholders this quarter, as much as 4.0B was allocated to common stock repurchases, demonstrating an active stance and confidence in capital allocation under the current capital framework (CET1 ratio of 10.3%).

Based on Wells Fargo (WFC) management guidance and market analysis, the growth momentum for the upcoming quarter (2Q26) and the remainder of 2026 is primarily driven by the following core areas:

1. Continued Expansion of Fee-based Income

The company is actively reducing its reliance on Net Interest Income (NII) and shifting toward lower capital-intensity fee income:

- Corporate and Investment Banking (CIB): Benefiting from the recovery in capital market activities, management expects continued growth in advisory and equity/debt underwriting services.

- Wealth Management: As Client Assets (AUM) reach historical highs between 2.2T and 2.5T, asset-based advisory fees are expected to increase alongside market valuations.

2. Digital Transformation and Penetration in Consumer Finance

- Credit Card Business: The momentum from the 60% growth in new accounts in 1Q26 is expected to translate into growth in receivables and interest income in 2Q26 and beyond. The company continues to invest in digital payment platforms to enhance customer engagement and revenue per customer.

- Auto and Mortgage Loans: As the interest rate environment stabilizes or trends downward, loan originations are expected to maintain growth, particularly following the standout performance of auto loans in 1Q26.

3. Expense Management and Operating Leverage

- Ongoing Streamlining Plans: Although headcount decreased 7% YoY in 1Q26, the company remains committed to further optimizing its Efficiency Ratio. Reducing operating expenses through digital automation will create operating leverage that directly contributes to EPS growth.

- Reduction in Legal and Regulatory Costs: As regulatory remediations from previous years near completion, related legal and settlement expenses have dropped significantly. These saved resources are being redirected toward technology development and growth-oriented investments.

4. Capital Allocation and EPS Accretion

- Share Repurchases: The company expects to maintain strong buyback momentum in 2026 (targeting approximately 4.0B per quarter). This will continue to reduce the number of shares outstanding, boosting EPS growth even in a flat revenue environment.

5. Macroeconomic Outlook and Reaffirmed Guidance

- Management reaffirmed the 2026 NII guidance of approximately 50B. Despite uncertainties in deposit costs, the company anticipates that stronger U.S. economic growth momentum in the second half of the year will support commercial loan demand.

Based on the guidance from Wells Fargo (WFC) management during the 1Q26 earnings call and subsequent market analysis, the Earnings Per Share (EPS) for the coming year is expected to show a steady upward trend, driven by the following factors:

1. 2026 EPS Growth Forecast

Market analysts estimate that the full-year EPS for 2026 will reach a range of $6.15 to $6.30, representing double-digit growth compared to 2025. The growth trajectory is expected to be stronger in the second half of the year as the macroeconomic environment stabilizes.

2. Core Growth Drivers

- Boost from Share Repurchases: The company plans to maintain a robust buyback momentum of approximately 4.0B per quarter throughout 2026. This large-scale reduction in share count is the most direct lever for boosting EPS, as it increases earnings per share by reducing the denominator, even if revenue growth remains flat.

- Improved Operating Efficiency: With the continued reduction in headcount (down 7% YoY as of 1Q26) and digital transformation lowering operating costs, operating leverage is expected to expand further, converting more revenue into net profit.

- Contribution from Non-Interest Income: Driven by a recovery in capital markets boosting investment banking fees and wealth management advisory fees, growth in these high-margin businesses will effectively offset the pressure on Net Interest Income (NII) caused by narrowing interest margins.

3. Potential Risk Factors

- Narrowing Net Interest Margin (NIM): If deposit costs rise faster than loan yields, or if the timing and magnitude of Federal Reserve rate cuts differ from expectations, it could squeeze NII.

- Credit Loss Provisioning: While asset quality remains stable for now, a potential economic slowdown in the second half of 2026 might require the company to increase provisions for credit card and commercial real estate loan losses, which would directly detract from quarterly net income.

- Asset Cap Restrictions: Although management remains optimistic about the removal of the asset cap, the bank’s ability to expand its balance sheet remains restricted until the cap is formally lifted.

4. Summary of the Trend for the Coming Year

In summary, WFC’s EPS trajectory over the next year will shift from being interest-margin dependent to being efficiency and capital-allocation dependent. The massive buyback program provides a solid floor for EPS, while growth in fee-based income remains the key variable that could drive EPS to exceed market expectations.

Source:

- https://www.wellsfargo.com/assets/pdf/about/investor-relations/earnings/first-quarter-2026-financial-results.pdf

- https://za.investing.com/news/company-news/wells-fargo-q1-2026-slides-earnings-beat-offset-by-revenue-miss-93CH-4211343

- https://sites.wf.com/outlook/

- https://matrixbcg.com/blogs/growth-strategy/wellsfargo

- https://www.zacks.com/stock/quote/WFC/detailed-earning-estimates

- https://www.investing.com/equities/wells-fargo-comp-earnings

Back to Wells Fargo page