Here is the summary of Verizon’s (VZ) latest quarterly earnings report (Q1 2026):

Key Financial Performance

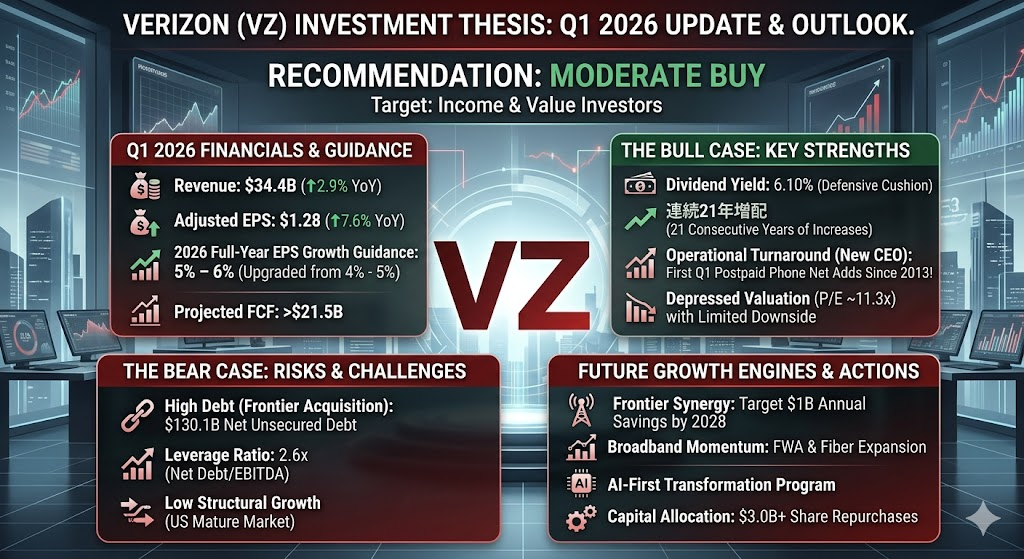

- Revenue: $34.4 billion, a year-over-year (YoY) increase of 2.9%.

- Adjusted EPS: $1.28, up 7.6% YoY, marking the best growth rate in four years.

- Profitability: Gross margin stood at 60.30%, operating margin at 23.93%, and net profit margin at 14.65%, with diluted EPS at $1.20.

Operational Highlights and Guidance

- Upgraded Guidance: Verizon raised its full-year 2026 adjusted EPS growth guidance to 5% to 6%, up from the previous forecast of 4% to 5%.

- Subscriber Growth: The company expects full-year postpaid phone net additions to reach the upper end of its previously guided range.

- Core Business Targets: Management reaffirmed its goal of achieving 2% YoY growth in both Mobility and Broadband service revenues.

Verizon demonstrated significant signs of a successful turnaround in its latest quarter (Q1 2026), driven by key operational changes and strategic milestones:

1. New CEO Leadership and Margin Focus

This quarter showcased the early strategic impact of newly appointed CEO Dan Schulman. The company shifted its focus toward disciplined promotional spending. While this approach slowed down device upgrade revenue, it significantly enhanced profitability, driving adjusted EPS growth to its highest rate since 2021.

2. Postpaid Phone Subscriber Breakout

Verizon achieved a major operational inflection point by breaking a decade-long seasonal pattern:

- Postpaid Phone Net Adds: The company added 55,000 net new postpaid phone subscribers. This represents Verizon’s first positive Q1 net add performance since 2013, fueled by strong new customer acquisitions.

- Broadband Momentum: Total broadband net additions reached 341,000, which included 214,000 Fixed Wireless Access (FWA) subscribers and 127,000 fiber broadband users.

3. Closure of the Frontier Acquisition

The company successfully finalized its $20 billion acquisition of Frontier Communications. This transaction immediately onboarded 2.2 million fiber customers, cementing broadband as a core growth vehicle. Management projects this combination will unlock $1 billion in annual cost synergies by 2028.

4. Balance Sheet and Capital Allocation Changes

- Debt Management: Due to the Frontier transaction, net unsecured debt increased to $130.1 billion, raising the net unsecured debt-to-adjusted EBITDA leverage ratio to 2.6x. However, Verizon already paid off about half of Frontier’s debt by the end of Q1 and expects to clear nearly all remaining Frontier debt by the end of 2026.

- Share Share Repurchases: Verizon completed $2.5 billion in share repurchases during the quarter, putting it on track toward its full-year buyback goal of at least $3.0 billion.

These fundamental updates provided management with the visibility to lift full-year EPS guidance and subscriber growth expectations.

Looking ahead to the upcoming quarters of 2026, CEO Dan Schulman and management explicitly noted during the earnings call that Q1 represents the operational low point for the year. As strategic initiatives deepen, growth momentum in the next quarter and beyond will be driven by four core engines:

1. Synergy Realization from Frontier and Fiber Expansion

With the Frontier Communications acquisition officially closed, Verizon’s fiber footprint has expanded to 30 million passings. Over the coming quarters, the focus shifts to cross-selling and bundling existing mobility customers into fiber broadband. Furthermore, management expects cost synergies to begin scaling, moving toward the target of $1 billion in annual run-rate savings by 2028, which will progressively support margins in the quarters ahead.

2. Execution of the AI-First Transformation Program

The company is aggressively rolling out its structured Transformation Program, which spans 10 major pillars with the goal of building an AI-first organization. By deeply integrating AI into customer service and daily operations, Verizon aims to further optimize the Cost of Acquisition (CoA) and Cost of Retention (CoR). This continuous enhancement of customer experience is expected to keep churn low and sustain the strong unit economics observed in Q1.

3. Sustained Double-Digit Growth in Broadband and FWA

Broadband continues to act as the primary top-line growth vehicle. Alongside the newly integrated fiber assets, 5G Fixed Wireless Access (FWA) is expected to maintain its robust momentum, tracking at a pace of over 200,000 net adds per quarter. This expansion is driven by broader mid-band spectrum deployment, which supports higher Average Revenue Per User (ARPU) and offsets legacy voice stagnation.

4. Acceleration in Core Service Revenue

Mobility and Broadband service revenue grew by 1.6% YoY in Q1, which management characterized as the absolute trough for the year. Backed by healthy new customer inflows, as evidenced by the unexpected positive Q1 postpaid phone net adds, the company expects growth rates to accelerate sequentially in the upcoming quarters to achieve its full-year service revenue growth target of 2% to 3%, reaching approximately $93 billion.

Verizon’s EPS trajectory over the next year exhibits clear signs of expansion and recovery. Following the stronger-than-expected Q1 profitability (Adjusted EPS of $1.28), both management and market consensus are increasingly optimistic about the company’s bottom-line outlook.

The core drivers and expectations for the EPS trend over the next 12 months include:

1. Upgraded Full-Year 2026 Official Guidance

Backed by robust Q1 performance, Verizon raised its full-year 2026 adjusted EPS growth guidance to 5% to 6%, up from the previous forecast of 4% to 5%. In absolute terms, the company now expects full-year adjusted EPS to land between $4.950 and $4.990.

2. Consensus Forecasts and Quarterly Trajectory

Wall Street consensus aligns tightly with management’s updated outlook, currently modeling full-year fiscal 2026 EPS at approximately $4.96.

Based on typical seasonal patterns and current operational visibility, the quarterly EPS trajectory over the coming year is projected as follows:

- Q2 2026 (Expected July): Sell-side consensus anticipates adjusted EPS to normalize around $1.24.

- Q3 2026: Expected to sustain strong performance at roughly $1.23.

- Q4 2026: Anticipated to experience a typical seasonal dip to around $1.15 due to holiday promotions and year-end customer acquisition costs.

- Q1 2027 (Outlook): As synergy realization deepens, analysts project next year’s opening quarter EPS could scale further to approximately $1.30.

Looking out over the next 12 months, the market expects Verizon’s rolling forward EPS to grow by about 5.85%, pushing toward $5.25.

3. Structural Tailwinds Backing EPS Expansion

- Disciplined Promotional Spending: The new CEO’s strict approach to promotional subsidies is actively expanding EBITDA margins (Adjusted EBITDA margin expanded by 140 basis points to 38.9% in Q1), which directly flows down to support EPS growth.

- Frontier Synergy Inception: The initial phase of the targeted $1 billion annual run-rate cost savings from Frontier will begin contributing to operating income sequentially.

- Share Count Reduction: Verizon’s $2.5 billion in share repurchases completed in Q1, toward a full-year target of at least $3.0 billion, will reduce the weighted average shares outstanding, providing a technical lift to EPS.

Verizon is an exceptional asset for defensive, income-focused investors prioritizing cash flow yield and capital preservation. However, it is not suited for growth-oriented investors seeking high capital appreciation or multiple expansion.

The Bull Case: Why You Should Buy

- Elite, Protected Dividend Yield: At the current price, Verizon offers a highly attractive forward dividend yield of 6.10%. Backed by 21 consecutive years of dividend increases, this yield provides a massive psychological cushion and concrete cash return in a volatile macro environment.

- Operational Turning Point Under New Leadership: Q1 2026 proved that the strategic pivot initiated by CEO Dan Schulman is working. By breaking a decade-long seasonal curse and delivering an unexpected 55,000 postpaid phone net adds, Verizon demonstrated it can acquire and retain high-value subscribers while maintaining promotional discipline.

- Depressed Valuation with Limited Downside: Trading at a trailing P/E of roughly 11.3x and a forward P/E of around 9.6x, VZ sits at the bottom of its historical valuation range. The market has already priced in an ultra-low growth profile, limiting further de-risking. Wall Street’s consensus 12-month price target of $50.59 implies an approximate 9% capital upside.

- Upgraded Guidance and Strong Cash Generation: Management’s decision to lift full-year 2026 adjusted EPS growth guidance to 5% to 6% signals internal confidence. Projected full-year free cash flow (FCF) exceeding $21.5 billion provides more than enough coverage for both dividend commitments and deleveraging.

The Bear Case: Risks to Consider

- The Frontier Debt Load: Taking on Frontier Communications for $20 billion expanded Verizon’s fiber footprint to 30 million passings, but it also bloated net unsecured debt to $130.1 billion, pushing its leverage ratio to 2.6x. While management paid down roughly half of Frontier’s debt in Q1 and intends to clear the rest by year-end, carrying high debt in a higher-for-longer interest rate environment remains a headline risk.

- Low Structural Top-Line Growth: The US telecom market is highly mature and saturated. Verizon’s 5-year CAGR hovers at a sluggish 1.4%. While broadband and 5G FWA are compounding nicely, they primarily offset the erosion of legacy voice and wireline revenues rather than generating explosive top-line growth.

Tactical Action Plan

- For Income & Value Investors: Accumulate shares in the $45 to $47 range. This allows you to lock in a ~6% yield while waiting for Schulman’s AI-first operational efficiencies and Frontier’s targeted $1 billion annual cost synergies to materialize and drive a modest valuation rerating.

- For Growth & Momentum Investors: Avoid or underweight. The opportunity cost of tying up capital in a slow-growth telecom stock is too high when compared to high-beta technology or AI infrastructure sectors where your capital could achieve better velocity.

Source:

- https://www.verizon.com/about/news/verizons-transformation-actions-deliver-growth-profitability-1q26-company-raises-adjusted-eps

- https://www.verizon.com/about/sites/default/files/Verizon-Earnings-Press-Release_0.pdf

- https://seekingalpha.com/news/4585661-what-is-next-for-verizon-after-strong-q1-2026-earnings-and-fiber-expansion

- https://www.marketbeat.com/stocks/NYSE/VZ/earnings/

- https://www.investing.com/news/transcripts/earnings-call-transcript-verizon-q1-2026-earnings-beat-expectations-93CH-4639160

- https://www.stocktitan.net/sec-filings/VZ/10-q-verizon-communications-inc-quarterly-earnings-report-ccd6f5d56ac0.html

- https://www.allinvestview.com/earnings/VZ/q1-2026/

- https://statementdog.com/analysis/VZ

- https://www.macromicro.me/stocks/info/VZ

Back to Verizon page