UnitedHealth Group (UNH) reported its first quarter 2026 financial results, showing continued revenue growth even as rising medical costs and specific expenditures impacted profit margins.

Here is a summary of the latest earnings report:

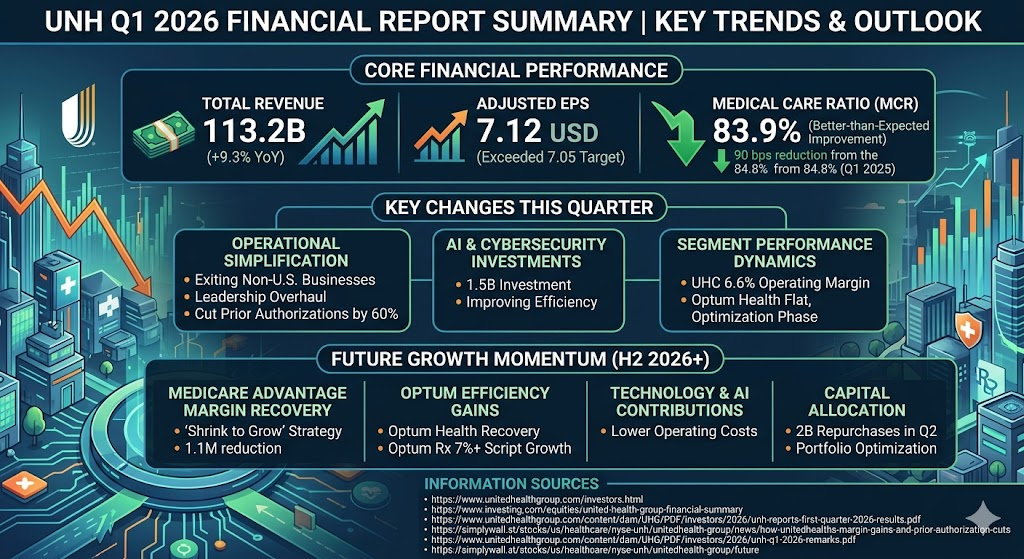

Core Financial Performance

- Total Revenue: Revenue reached 113.2B this quarter, an increase of approximately 9.3% year-over-year, reflecting steady expansion in the insurance business and Optum health services segments.

- Adjusted Earnings Per Share (Adjusted EPS): Approximately 7.12 USD, slightly exceeding market expectations of 7.05 USD.

- Medical Care Ratio (MCR): The MCR rose to 84.3% this quarter, higher than the 82.2% reported in the same period last year. This reflects pressure from increased outpatient surgery volumes and high prescription drug costs.

Business Segment Performance

- UnitedHealthcare (Insurance): Revenue reached 87.5B. Growth was supported by steady increases in Medicare Advantage membership, despite challenges from lowered government reimbursement rates. Total membership remains above 51 million.

- Optum (Health Services): Revenue grew to 62.4B. Optum Health (clinical services) and Optum Rx (pharmacy benefit management) were the primary growth engines, with Optum Rx script volume increasing by 7% year-over-year.

Key Highlights and Future Outlook

- Medical Cost Pressures: Markets are closely monitoring the continued recovery in medical demand among seniors (such as hip and knee surgeries), which is the main driver behind the rising MCR.

- 2026 Full-Year Guidance: The company maintained its full-year adjusted EPS guidance range of 30.25 USD to 30.75 USD, indicating management’s confidence in operational efficiency improvements and cost control for the second half of the year.

- Cash Flow and Shareholder Returns: Operating cash flow reached 8.6B this quarter. The company continues to return value to shareholders through dividends and share repurchases.

In the first quarter 2026 earnings report, UnitedHealth Group (UNH) demonstrated significant strategic shifts and operational adjustments. Compared to previous quarters burdened by cyberattacks and surging costs, this quarter’s key changes focused on profitability recovery and structural simplification:

1. Better-than-Expected Improvement in Medical Care Ratio (MCR)

The most notable change this quarter was the MCR decreasing to 83.9%, down 90 basis points (0.9%) from 84.8% in the same period last year. This indicates that the company has successfully addressed previous medical demand pressures through premium repricing and effective cost controls, serving as a core driver for the stock price rebound.

2. Operational Simplification and Strategic Transformation

Management emphasized “modernization” and “decentralization” during this quarter:

- Exiting Non-U.S. Businesses: The company officially decided to refocus on the U.S. domestic healthcare market and has completed the sale of overseas operations such as Optum UK.

- Leadership Overhaul: Nearly half of the top 100 leadership positions have been refreshed, reflecting a profound cultural and management transformation within the company.

- Significant Reduction in Prior Authorizations: Announced a plan to remove 60% of prior authorization requirements by the end of 2026 to simplify medical processes and reduce administrative friction.

3. Upward Revision of Full-Year Financial Guidance

Based on the strong performance in the first quarter, UNH raised its profit forecast for the full year 2026:

- Adjusted EPS: Increased from the previous 17.75 USD to above 18.25 USD.

- This move signaled to the market that the company has moved past its operational low point and entered a period of earnings recovery.

4. Concrete Investments in AI and Technology

The company disclosed an investment of approximately 1.5B in Artificial Intelligence (AI) and Cybersecurity this quarter. These investments are primarily aimed at improving administrative efficiency, automating care management, and enhancing system stability, which are expected to be the main growth engines for the Optum segment’s profitability in the coming years.

5. Performance Dynamics Across Business Segments

- UnitedHealthcare: Strong profit performance with operating margins rising to 6.6%, largely due to pricing adjustments across all business lines.

- Optum Health: Performance remained relatively flat, primarily affected by the restructuring of value-based care membership and cost pressures, and is currently in an operational optimization phase.

Looking ahead to the second half of 2026 and beyond, UnitedHealth Group (UNH) is shifting its growth momentum from profitability recovery toward structural growth. The primary drivers are as follows:

1. Medicare Advantage Pricing and Margin Recovery

- Shrink to Grow: In 2026, the company adopted a disciplined pricing strategy, choosing to accept a loss of approximately 1.1M members (primarily in low-margin markets) in exchange for higher premium revenue and improved profit margins. This strategy is expected to yield results in the second half of the year by stabilizing the overall Medical Care Ratio.

- 2027 Bidding Strategy: UNH anticipates that medical trends will remain elevated at around 10% in 2026. Consequently, the operational focus in the coming quarter will be on optimizing product design for 2027 to maintain its leadership position in government programs.

2. Efficiency Gains in the Optum Segment

- Optum Health Transformation: This segment is entering a period of return on investment for its value-based care initiatives. Following contract adjustments and organizational simplifications initiated in late 2025, margins are expected to gradually recover in the second half of 2026.

- Optum Rx Script Volume Growth: Driven by increased demand for new medications, particularly GLP-1 weight-loss drugs and specialty pharmaceuticals, script processing volume is expected to maintain a growth rate of over 7%.

3. Tangible Contributions from AI and Digital Transformation

- 1.5B Investment Case: The company plans to invest approximately 1.5B in AI and cybersecurity in 2026. A key focus is the removal of 60% of prior authorization requirements, which is expected to significantly lower administrative costs and enhance clinical decision-making efficiency.

- Operating Cost Ratio Leverage: By utilizing AI to automate claims processing and care management, management expects to effectively suppress the administrative expense ratio even as revenue grows.

4. Capital Allocation and Shareholder Returns

- Share Repurchase Program: The company expects to complete approximately 2B in share repurchases by the end of the second quarter of 2026, which will directly support full-year EPS performance.

- Portfolio Optimization: By divesting non-core assets (such as remaining businesses in Brazil and South America, as well as Optum UK), UNH is concentrating more resources on high-growth healthcare service markets within the United States.

Financial Guidance Summary

The company has raised its full-year 2026 adjusted EPS target to above 18.25 USD, indicating that growth momentum remains strong under the dual drivers of cost control and pricing adjustments in the second half of the year.

Source:

- https://www.unitedhealthgroup.com/investors.html

- https://hk.investing.com/equities/united-health-group-financial-summary

- https://www.unitedhealthgroup.com/content/dam/UHG/PDF/investors/2026/unh-reports-first-quarter-2026-results.pdf

- https://simplywall.st/stocks/us/healthcare/nyse-unh/unitedhealth-group/news/how-unitedhealths-margin-gains-and-prior-authorization-cuts

- https://www.unitedhealthgroup.com/content/dam/UHG/PDF/investors/2026/unh-q1-2026-remarks.pdf

- https://simplywall.st/stocks/us/healthcare/nyse-unh/unitedhealth-group/future

Back to United Health page