Union Pacific Corporation (UNP) Q1 2026 Earnings Summary

Union Pacific released its Q1 2026 financial results on April 23, 2026, delivering results that exceeded market expectations and set multiple first-quarter records.

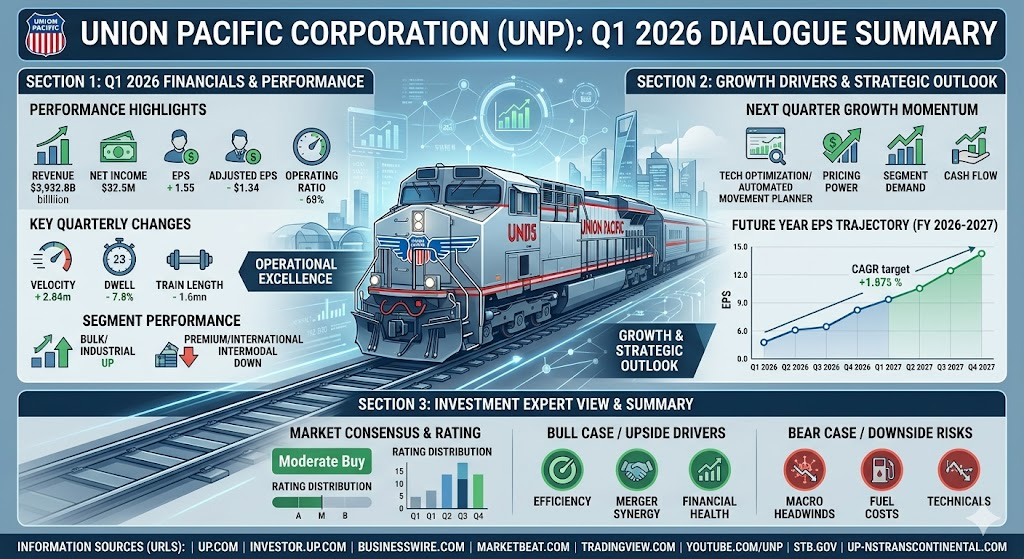

Financial Highlights

- Revenue: 6.2B USD, up 3% year-over-year.

- Net Income: 1.7B USD, up 5% year-over-year.

- EPS: 2.87 USD, up 6% year-over-year.

- Adjusted EPS: 2.93 USD, up 9% year-over-year (surpassing consensus estimates of 2.85 USD).

- Operating Ratio: Improved by 80bps to 59.9%, indicating significant gains in operational efficiency.

Operational Analysis

- Pricing and Volume: Core pricing remained strong. Freight revenue (excluding fuel surcharges) grew 3% to 5.285B USD, driven by a 3.25% pricing contribution. While total volume declined slightly by 0.75%, growth in domestic intermodal, coal, and grain shipments offset weakness in international intermodal business.

- Cost Management: Despite inflationary pressures from wages, benefits, and fuel costs, the company successfully limited the growth of total operating expenses to 3%—matching revenue expansion—by improving productivity and reducing headcount.

- Cash Flow: Cash flow from operations reached 2.44B USD, up 10% year-over-year, with a cash flow conversion rate of 88%. The company used cash to pay down 1.2B USD in debt and deployed 0.9B USD toward capital expenditures.

Full-Year Outlook

The company reaffirmed its full-year 2026 guidance:

- EPS: Expected to grow in the mid-single digits.

- Operating Ratio: Continued improvement projected.

- Long-Term Goal: Remains committed to achieving a CAGR of high-single to low-double digits for EPS through 2027.

In Q1 2026, Union Pacific (UNP) demonstrated exceptional operational execution and pricing discipline. Here are the most significant changes and operational highlights from the quarter:

1. Record-Breaking Operational Efficiency

The most notable change was the use of technology and management initiatives to drive productivity to historical highs, successfully offsetting inflationary cost pressures:

- Operational Metrics: Freight car velocity improved by 9%, and average terminal dwell time improved by 11%, reaching a record-best of 19.7 hours.

- Labor and Automation: Despite a 5% reduction in headcount, labor productivity rose by 7%, driven by technological investments such as the Automated Movement Planner.

- Resource Optimization: Average train length increased by 3%, allowing the company to move more freight while running fewer trains.

2. Divergence in Revenue Segments

While total revenue grew 3%, the performance across business segments varied significantly, reflecting structural shifts in market demand:

- Growth Areas: Bulk cargo grew 10%, bolstered by grain exports (particularly to Mexico and China) and steady coal shipments. Industrial products rose 5%, driven by demand for materials related to LNG terminal facilities and data center construction.

- Weakness: The Premium segment declined 5%, dragged down by a 28% drop in international intermodal volume, primarily due to lower West Coast import volumes and shifts in customer mix. Notably, domestic intermodal business set a record for the third consecutive quarter.

3. Strategic Pricing Power

Against a backdrop of a 0.75% decline in total volume, Union Pacific relied on core pricing strength to drive revenue growth:

- Pricing and Mix Effects: Core pricing and product mix contributed 325 basis points to revenue growth, successfully offsetting the 75-basis-point drag from volume declines.

- Margin Defense: The adjusted operating ratio improved by 80 basis points to 59.9%, demonstrating strong pricing discipline and profit protection despite an uneven macroeconomic environment.

4. Key Management Decisions and Capital Planning

- M&A Progress: The company continued to push forward with its merger with Norfolk Southern, submitting revised filings in late April 2026—a critical step in its bid to become the first true transcontinental railroad in the U.S.

- Capital Allocation Discipline: While the annual capital expenditure plan remains unchanged at 3.3B USD, the company has explicitly signaled a “pause in share repurchases,” prioritizing cash flow for debt reduction (1.2B USD repaid in Q1) and strategic infrastructure projects.

- Guidance Transparency: The company updated its EPS outlook following the Q1 results, explicitly incorporating merger-related expenses into its guidance to provide greater transparency to investors.

In summary, Q1 2026 for Union Pacific was a quarter where “execution” outweighed “market growth.” By optimizing internal operations to offset macroeconomic headwinds and maintaining flexible pricing, the company managed to deliver record profits despite moderate volume pressure.

The growth momentum for Union Pacific (UNP) for the upcoming quarter and the remainder of the year is primarily driven by operational productivity, strategic pricing, and long-term synergy potential from its proposed merger. Based on the Q1 earnings report and management commentary, here are the key growth drivers:

1. Sustained Operational Productivity Gains

The company is focused on further improving its Operating Ratio through technology.

- Tech-Enabled Efficiency: The continued rollout of the Automated Movement Planner is expected to further enhance train velocity, reduce terminal dwell times, and optimize locomotive and labor allocation.

- Network Fluidity: Management aims to sustain the record-level terminal dwell time of 19.7 hours achieved in Q1. Maintaining this efficiency is critical to lowering variable costs per unit and maximizing operating leverage.

2. Core Pricing Power

Despite volume sensitivity to macroeconomic conditions, Union Pacific has demonstrated robust pricing discipline.

- Pricing and Mix Optimization: The company will continue to utilize strategic pricing to offset inflationary pressures and optimize its cargo mix. Even if overall volumes remain muted, the pricing contribution from high-margin segments, such as industrial products and domestic intermodal, will serve as the primary engine for profit growth.

3. Major Strategic Catalyst: Transcontinental Merger

Progress on the merger with Norfolk Southern remains a long-term growth anchor.

- Merger Process: Following the submission of revised filings in late April 2026, the potential for establishing the first true U.S. transcontinental railroad continues to be a major focus. Management anticipates that this network will save shippers 3.5B USD annually, which should improve market share and allow for structural cost optimizations through network integration.

4. Structural Demand in Key Sectors

While global trade remains fragmented, specific industries continue to provide growth support:

- Energy and Infrastructure: With the ongoing surge in data center construction and LNG terminal facilities, the Industrial Products segment is expected to see sustained demand for construction materials and related inputs.

- Agricultural Exports: Shipments to Mexico and China remain reliable sources of volume and revenue, serving as an important buffer against volatility in other trade lanes.

5. Capital Allocation and Financial Flexibility

The company’s current capital strategy is designed to strengthen profitability:

- Cash Flow Prioritization: With share repurchases paused, cash is being prioritized for debt reduction (1.2B USD repaid in Q1) and core network investment. This strategy effectively lowers interest expenses and improves the quality of EPS.

- Guidance: The company reaffirmed its 2026 full-year EPS growth target of mid-single digits and remains committed to a long-term EPS CAGR target of high-single to low-double digits through 2027.

Potential Headwinds

- Fuel Costs: Management has signaled that fuel prices, particularly if sustained above 4 USD per gallon, pose a challenge to profit margins in the second quarter.

- Macroeconomic Uncertainty: Continued fragmentation in global supply chains and geopolitical tensions present ongoing risks to the International Intermodal segment.

In summary, growth momentum in the coming quarter will depend less on a broad macroeconomic recovery and more on the company’s internal execution and its ability to advance the transcontinental merger to secure future market share.

Union Pacific (UNP) has maintained a disciplined and forward-looking outlook for its EPS trajectory over the next 12 months. Based on management guidance and consensus analyst projections, here is the outlook:

1. 2026 Full-Year Guidance: Mid-Single-Digit Growth

The company has reaffirmed its guidance for the full year 2026, projecting reported EPS to grow in the “mid-single digits” year-over-year. This guidance accounts for potential merger-related expenses and reflects a strategic balance between productivity gains and inflationary pressures.

2. Consensus EPS Projections

Market consensus estimates point to a steady upward trend in earnings over the next four quarters:

- FY 2026 Estimate: Analysts generally project full-year 2026 EPS to fall within the range of 12.53 USD to 12.62 USD.

- FY 2027 Outlook: EPS is expected to grow to approximately 13.48 USD in 2027, representing a year-over-year increase of roughly 7.5% to 9%.

3. Key Variables Impacting EPS

- Positive Drivers:

- Operating Leverage: As the company continues to deploy the Automated Movement Planner and other technological tools, efficiency gains are expected to directly expand profit margins.

- Pricing Discipline: Robust pricing power remains the cornerstone of EPS growth, allowing the company to defend margins despite macroeconomic volatility.

- Capital Structure Optimization: The decision to pause share repurchases and prioritize debt repayment is successfully reducing interest expenses, thereby improving the quality and sustainability of bottom-line earnings.

- Potential Headwinds:

- Energy Costs: Management has explicitly signaled that if diesel prices sustain levels above 4 USD per gallon, it will exert direct pressure on quarterly operating margins.

- Volume Volatility: Persistent weakness in international intermodal traffic, if not offset by domestic growth, could limit top-line expansion and subsequently dampen EPS acceleration.

4. Long-Term Strategic Targets (Through 2027)

The company remains committed to its long-term financial target: achieving a compound annual growth rate (CAGR) for EPS in the “high-single to low-double digits” through 2027. This indicates that management is focused on structural margin expansion through network integration and scale rather than just short-term operational tweaks.

In summary, Union Pacific’s EPS trajectory over the next year is expected to be modestly growth-oriented, characterized by a careful balancing act between internal productivity improvements and external cost pressures. As merger synergies are gradually realized heading into 2027, the market expects a shift toward more pronounced earnings expansion.

As of May 2026, market sentiment and analyst consensus on Union Pacific (UNP) lean toward a Moderate Buy, reflecting confidence in its operational efficiency despite broader economic uncertainties.

1. Analyst Consensus and Price Targets

- Consensus Rating: The stock holds a “Moderate Buy” rating among the 22 analysts covering the company. The breakdown typically shows roughly 13–15 “Buy” ratings, 7–8 “Hold” ratings, and rarely any “Sell” ratings.

- Price Targets: The average 12-month price target ranges between 280 USD and 291 USD.

- Upside Potential: With the stock recently hitting 52-week highs near 275 USD, the immediate upside based on the average target is modest (approximately 5% to 8%). However, more bullish analysts (e.g., from firms like Benchmark and Wolfe Research) have set targets as high as 300–310 USD, implying a potential upside of 10% to 15%.

2. Bullish Case (Potential Upside)

- Operational Excellence: UNP is currently recognized for its superior efficiency, evidenced by record-setting terminal dwell times and freight car velocity. Analysts highlight this “operational pivot” as a durable competitive advantage.

- Merger Synergy: The proposed merger with Norfolk Southern remains a key catalyst. Analysts generally view this as a “favorable scenario regardless of the outcome”—if approved, it provides significant long-term growth and cost synergies; if blocked, the company’s standalone operational strength remains highly attractive.

- Financial Health: With a perfect Piotroski Score of 9, the company demonstrates exceptional financial robustness. The decision to pause share buybacks to prioritize debt reduction has been well-received, strengthening the balance sheet and supporting long-term dividend stability.

3. Bearish Case (Downside Risks)

- Economic Headwinds: UNP’s growth is heavily tied to industrial production and global trade flows. Continued weakness in International Intermodal or a failure of the freight market to re-accelerate later in 2026 could cap revenue growth.

- Valuation & Technicals: Having reached 52-week highs, some quantitative models and valuation analyses suggest the stock is becoming fully valued or even slightly overextended, which may invite short-term profit-taking.

- Cost Pressures: Sustained fuel costs—particularly if diesel prices remain above 4 USD per gallon—remain a tangible threat to operating margins.

Summary for Investors

Union Pacific is currently positioned as a “quality compounder.”

- For Long-term Investors: The stock is often viewed as a core industrial holding due to its “hard-to-replicate” rail infrastructure and strong margin profile.

- For Tactical Traders: The stock is trading near record highs; while the fundamental momentum is positive, the potential for near-term volatility exists if economic data weakens or if the merger approval process faces unexpected delays.

Disclaimer: This analysis is based on market data as of May 22, 2026. Stock market investments carry inherent risks. Please conduct your own due diligence or consult with a financial advisor before making investment decisions.

Source:

- https://www.tradingview.com/news/tradingview:e45d8a0407ec6:0-union-pacific-reports-q1-2026-net-income-1-7b-diluted-eps-2-87-operating-ratio-60-5/

- https://www.businesswire.com/news/home/20260423915569/en/Union-Pacific-Reports-First-Quarter-2026-Results

- https://www.investing.com/news/company-news/union-pacific-q1-2026-slides-record-earnings-operational-gains-shine-93CH-4633349

- https://ca.investing.com/news/stock-market-news/union-pacific-earnings-call-transcript-union-pacific-beats-q1-2026-forecasts-stock-rises-93CH-4583481

- https://www.marketbeat.com/stocks/NYSE/UNP/earnings/

- https://www.youtube.com/watch?v=z-L-4TkfxCw

- https://www.tradingview.com/news/urn:summary_document_transcript:quartr.com:3356766:0-unp-merger-aims-to-create-a-transcontinental-railroad-boosting-efficiency-and-customer-service/

- https://www.stb.gov/resources/major-railroad-mergers/

- https://www.up-nstranscontinental.com/

Back to Union Pacific page