Foundation and Initial Launch (2009-2011)

Uber was founded in 2009 in San Francisco by Travis Kalanick and Garrett Camp, originally under the name UberCab. The idea was conceived after the founders struggled to hail a cab during a snowy winter night in Paris. In 2010, the company officially launched its smartphone application, initially offering premium premium black car services exclusively in San Francisco. In 2011, the company officially shortened its name to Uber and began expanding to major cities including New York, Seattle, and Paris.

Explosive Global Expansion and Regulatory Conflict (2012-2016)

In 2012, Uber introduced UberX, a lower-cost option allowing drivers to use their own personal vehicles to transport passengers. This move triggered the rapid global adoption of the sharing economy model. During this period, Uber aggressively entered international markets, which led to intense legal battles, driver strikes, and regulatory resistance from traditional taxi industries worldwide. Despite these hurdles, Uber continued to innovate, launching its carpooling service UberPool in 2014 and debuting its food delivery platform Uber Eats in 2015, effectively entering the logistics sector.

Leadership Restructuring and Corporate Transformation (2017-2019)

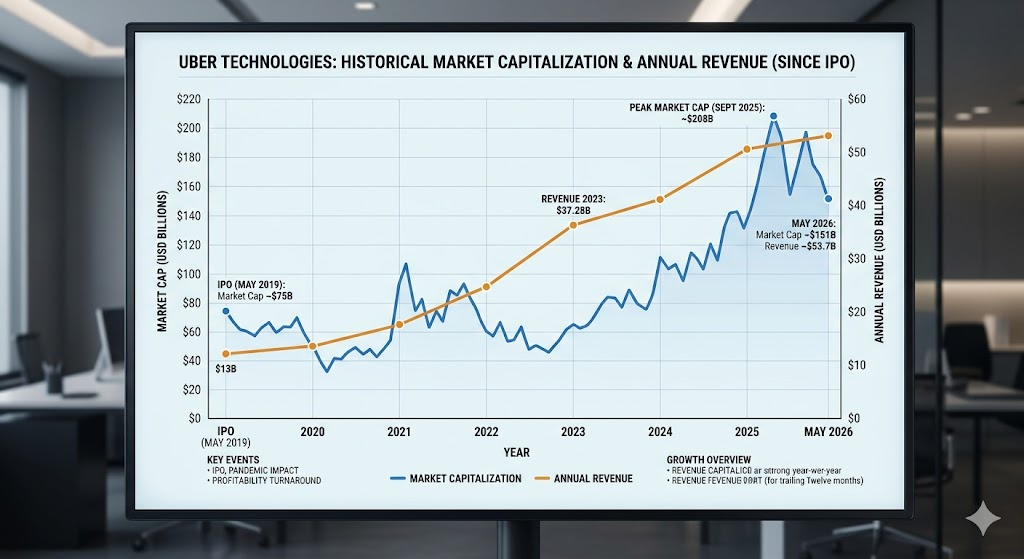

Rapid global expansion eventually led to internal corporate culture crises and public relations challenges. In 2017, co-founder Travis Kalanick resigned as CEO under pressure from investors. Dara Khosrowshahi was appointed as the new CEO, initiating a period of cultural overhaul and regulatory compliance. During this phase, Uber adopted a consolidation strategy, selling its unprofitable regional operations in China, Russia, and Southeast Asia to local competitors like Didi and Grab. In May 2019, Uber officially went public on the New York Stock Exchange.

Pandemic Resilience and Dual-Engine Growth (2020-2023)

The outbreak of the COVID-19 pandemic in 2020 severely impacted Uber’s core ride-hailing business due to global lockdowns. However, this crisis accelerated the growth of Uber Eats. The food delivery segment experienced exponential growth and temporarily eclipsed ride-hailing revenues, sustaining the company through the downturn. As pandemic restrictions lifted, mobility services recovered. Uber initiated a strict profitability plan, divesting non-core assets such as its autonomous driving unit ATG, and achieved its first-ever full-year GAAP operating profit in 2023, leading to its inclusion in the S&P 500 index.

Platform Integration and Sustainable Mobility (2024-Present)

Today, Uber operates as an integrated super-app combining mobility, delivery, grocery, freight, and advertising. The strategic focus centers on platform synergy and digital advertising monetization. The company is actively driving a green transition, committing to becoming a fully zero-emission platform by 2040. Furthermore, Uber continues to expand strategic partnerships with autonomous vehicle technology providers, gradually deploying driverless cars and delivery bots into its existing global network to shape the future of urban transportation.

Core Businesses and Competitor Landscapes

As the world’s largest mobility and logistics platform, Uber operates in a competitive landscape characterized by intense regional dominance and cross-industry convergence, structured across two primary segments: mobility and delivery.

Mobility Segment

In North America, Uber’s most direct rival is Lyft (capturing approximately 24% market share). Lyft operates primarily in the US and Canada with a focused portfolio in ridesharing and micromobility, engaging Uber in continuous pricing and driver incentive optimization.

Globally, Uber competes with entrenched regional giants. In Europe and Africa, Bolt exerts pricing pressure through a low-commission model. In the Asia-Pacific region, Ola dominates in India, while Didi Chuxing holds absolute market control in China. Uber manages relations with formidable former rivals like Didi and Southeast Asia’s Grab primarily through strategic minority equity stakes.

Delivery and Local Logistics Segment

In food, grocery, and retail delivery, Uber competes with highly specialized e-commerce platforms. In the United States, DoorDash maintains market dominance with over 66% share, placing significant competitive pressure on Uber Eats. In response, Uber Eats has expanded beyond restaurant delivery into non-food retail and grocery distribution via partnerships with major retailers like Costco and Carrefour.

Internationally, the delivery segment remains highly fragmented, with Uber competing against dominant regional players such as Delivery Hero, Just Eat Takeaway, Wolt in Europe, and Rappi in Latin America.

Uber’s Core Competitive Advantages

Flywheel Effect of a Dual-Engine Platform

Uber’s primary strategic asset is its balanced portfolio across both mobility and delivery. This dual-engine architecture acts as an operational hedge against economic cycles and macro disruptions (exemplified during the pandemic when delivery growth offset severe mobility declines).

Cross-platform synergy is highly efficient: the mobility user base provides a low-cost, high-conversion funnel for the delivery ecosystem.

Customer Lock-in via Uber One

The global Uber One subscription base has surpassed 50 million members. This unified membership program spans both mobility and delivery services, driving over 50% of the platform’s total gross bookings. The subscription model significantly increases Customer Lifetime Value (LTV) and reduces churn.

Asset-Light Autonomous Vehicle (AV) Open Platform Strategy

In navigating the transition to autonomous driving (Robotaxi), Uber has adopted an open platform strategy rather than pursuing the vertically integrated manufacturing model favored by companies like Tesla. Uber positions itself as the premier global distribution and dispatch marketplace for autonomous fleets, integrating over 30 AV technology partners including Waymo, Zoox, and Juvo.

By avoiding capital-intensive hardware manufacturing and maintenance, Uber leverages its network of over 160 million monthly active platform consumers to serve as the critical commercialization and dispatch engine for AV providers.

Strategic Threats and Competitive Risks

- Disruption Pace of Autonomous Technology: If vertically integrated operators like Tesla’s Robotaxi network or Waymo’s proprietary fleet scale faster than anticipated and bypass Uber’s network to interface directly with consumers, it could disrupt Uber’s traditional driver-dependent marketplace dynamics.

- Global Labor Regulation and Classification: Regulatory scrutiny surrounding the classification of independent contractors versus employees remains a persistent risk (such as shifting gig-economy legal frameworks in Europe and the US). Reclassification mandates would significantly increase platform operating costs.

- Low Loyalty and Multi-Homing Behavior: The prevalence of multi-homing—where consumers cross-shop fares between Uber and Lyft, and drivers operate multiple apps concurrently—limits long-term brand lock-in and restricts pricing flexibility, requiring continuous marketing and incentive deployment to maintain network liquidity.

Source:

- https://www.uber.com

- https://investor.uber.com

- https://www.sec.gov

- https://www.lyft.com

- https://www.doordash.com

- https://waymo.com

Back to Uber page