The history of Southern Copper Corporation (formerly Southern Peru Copper Corporation) can be divided into four distinct phases:

Phase 1: Foundation and Development in Peru (1952-1970s)

- Founding and Strategy: Established in 1952 as a joint venture between ASARCO, Newmont, and other firms to explore copper deposits in Peru.

- Early Operations: The Toquepala mine commenced production in 1960, marking the start of large-scale operations. The company built essential infrastructure, including smelting facilities in Ilo, railways, and port facilities.

- Expansion: The Cuajone mine was commissioned in 1976, significantly increasing production capacity.

Phase 2: Restructuring and Public Offering (1980s-1990s)

- Technological Upgrades: The company invested heavily in modernizing mining and refining processes, such as the acquisition of the Ilo smelter in 1994 to enhance refining capabilities.

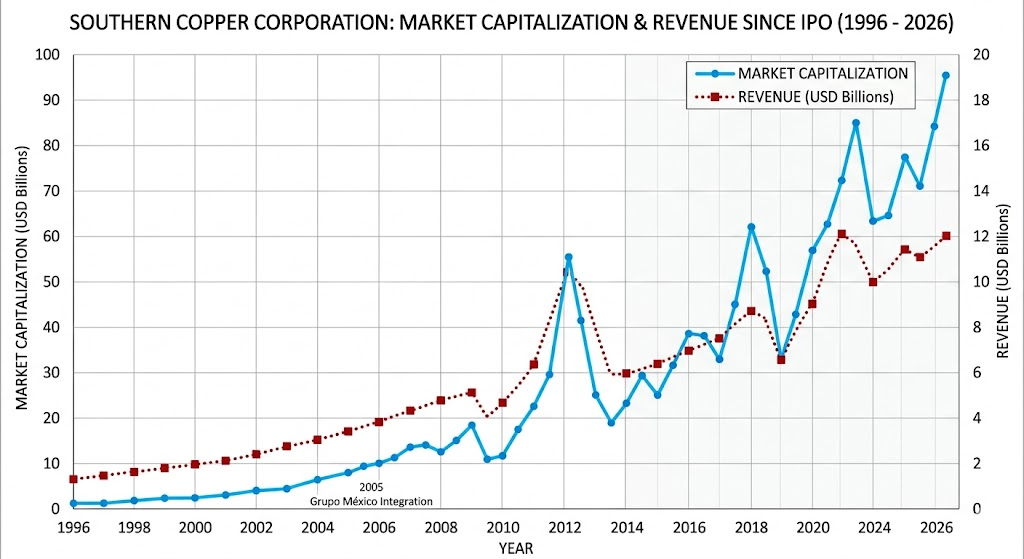

- Capital Market Integration: In 1996, the company underwent a major restructuring and officially listed on the New York Stock Exchange (NYSE) and the Lima Stock Exchange (BVL), transitioning into a publicly traded corporation.

Phase 3: Integration into Grupo México (1999-2005)

- Change in Control: In 1999, the Mexican mining giant Grupo México acquired ASARCO, thereby gaining controlling interest in Southern Copper.

- Corporate Consolidation: In 2005, the company acquired Minera Mexico from Grupo México, expanding its footprint from Peru into Mexico. This created the vertically integrated entity seen today, officially rebranding as Southern Copper Corporation (SCCO) to reflect its expanded scope.

Phase 4: Leadership and Sustainable Growth (2006-Present)

- Capacity and Reserve Expansion: The company continued to invest in major brownfield projects, such as the Toquepala expansion, solidifying its position as one of the world’s largest copper producers by reserves.

- Modernization and ESG Focus: The company has shifted focus toward sustainable development, investing significant capital into environmental protection infrastructure, operational automation, and water recycling to meet global ESG standards.

Southern Copper Corporation (SCCO) maintains a dominant competitive position in the copper mining industry. Below is an analysis of its core advantages, primary competitors, and market risks.

Core Competitive Advantages

- Industry-Leading Cost Structure: SCCO consistently ranks in the lowest quartile of the global copper cash cost curve. This efficiency is driven by high-grade ore, optimized open-pit mining technology, and significant economies of scale.

- Massive Reserve Base: The company holds one of the largest copper reserves among publicly traded firms globally. This provides a robust foundation for long-term operations, allowing it to navigate price volatility with financial stability.

- Vertical Integration: By owning and operating its own smelting and refining facilities, SCCO is shielded from external treatment and refining charge (TC/RC) market volatility, granting the company superior profit margin control.

- Geographical and Operational Balance: Assets are strategically distributed across Peru and Mexico, with strong sales penetration in the US market. This geographic footprint provides a buffer against regional political or economic instability.

Primary Competitors

SCCO competes with global mining giants and specialized copper producers:

- Freeport-McMoRan (FCX): A US-based copper and gold producer operating the massive Grasberg mine, standing as SCCO’s most direct competitor in North American and global markets.

- Codelco: The state-owned Chilean copper company and one of the world’s largest producers, representing significant state-backed scale and resource control.

- Hudbay Minerals (HBM): Frequently compared to SCCO by analysts regarding growth potential and operating leverage, particularly regarding portfolio optimization.

- Global Diversified Majors: Companies like BHP, Rio Tinto, and Glencore compete directly with SCCO in terms of output capacity and extraction technology.

Market Challenges and Risks

- Political and Regulatory Risks: Operations in Peru and Mexico face complex political environments, labor regulation shifts, and pressure from resource nationalism that can affect tax regimes.

- ESG and Social Responsibility: As a large-scale miner, SCCO must commit massive capital to decarbonization, water management, and waste treatment. Maintaining community “social license to operate” is critical for advancing major projects like Tia Maria in Peru.

- Capital Expenditure Pressure: To maintain output levels against declining ore grades, the company has an extensive capital expenditure pipeline (exceeding $15B). This can constrain free cash flow if copper prices remain volatile or if global economic growth slows.

- Substitutes: While technical performance gaps persist, metals like aluminum can serve as substitutes for copper in certain industrial applications during periods of extreme price divergence, impacting long-term demand elasticity.

Analyst Insight:

Market observers characterize SCCO as having a dual advantage as a “cost leader” and “reserve owner.” Although some financial institutions maintain neutral ratings due to regional political exposure, SCCO’s strong net profit margin (consistently above 30%) and significant cash flow generation position it as a benchmark company for both defensive and growth-oriented investors looking to capitalize on the energy transition-driven copper demand.

Source:

- https://www.southerncoppercorp.com/

- https://en.wikipedia.org/wiki/Southern_Copper_Corporation

- https://southerncoppercorp.com/eng/know-our-history/

- https://tracxn.com/d/companies/southerncopper/__aLZTsqQlBFuomFbZCOJdQjUlBdV_WVBk9_hcF9xZnyc

- https://thebull.com.au/us-news/analyst-names-top-us-metals-stocks-amidst-structural-shift/

- https://www.marketbeat.com/stocks/NYSE/SCCO/competitors-and-alternatives/

- https://dcfmodeling.com/products/southern-copper-corporation-scco-porters-five-forces-analysis/

Back to Southern Copper page