Pfizer reported its Q1 2026 financial results on May 5, 2026, delivering performance that exceeded Wall Street consensus. As the pandemic-era revenue base normalizes, growth is increasingly driven by recently launched and acquired products, particularly within oncology.

Core Financial Metrics

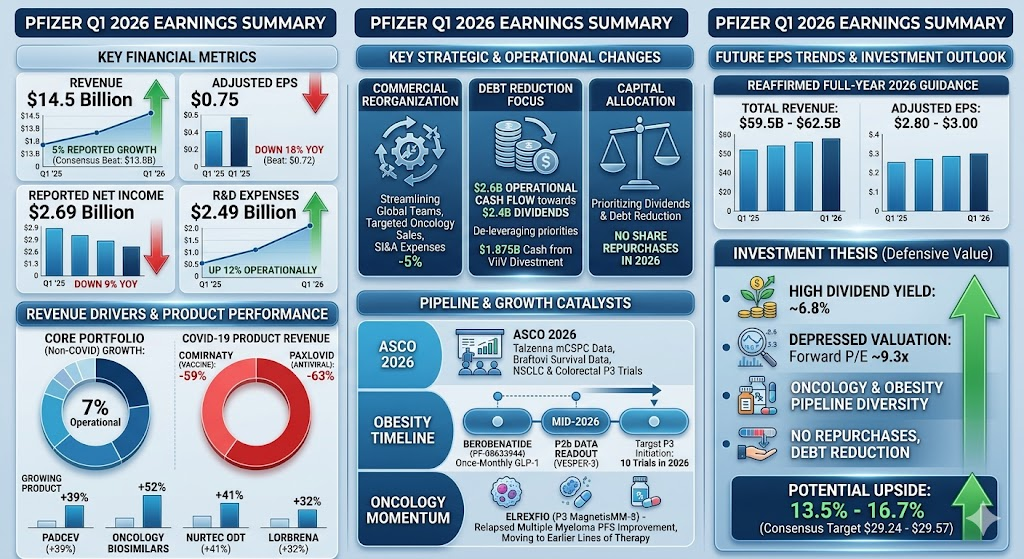

- Revenue: $14.5 billion, up 5% on a reported basis (2% operational growth) compared to the prior-year quarter, beating market estimates of $13.8 billion.

- Adjusted Diluted EPS: $0.75, down 18% year-over-year but ahead of the consensus estimate of $0.72.

- Reported Net Income: $2.69 billion, a decrease of 9% from Q1 2025.

- Research & Development (R&D) Expenses: $2.49 billion, increasing 12% operationally due to intensified investments in late-stage oncology and obesity pipeline assets.

Revenue Drivers and Product Performance

- Decoupling from COVID-19: Excluding contributions from Comirnaty (vaccine) and Paxlovid (antiviral), Pfizer’s core non-COVID portfolio achieved solid 7% operational revenue growth.

- New and Acquired Portfolios: Launched and acquired assets (largely driven by the Seagen acquisition) posted a combined 22% operational revenue jump, totaling $3.1 billion.

- Padcev (Urothelial Cancer): Up 39% operationally, driven by market share expansion in first-line treatments.

- Oncology Biosimilars: Grew 52% operationally worldwide.

- Nurtec ODT (Migraine): Surged 41% operationally from strong acute and preventive demand.

- Lorbrena (Lung Cancer): Rose 32% operationally.

- COVID-19 Product Declines: Comirnaty fell 59% operationally, and Paxlovid dropped 63% operationally due to lower baseline infection rates and transitioning contract dynamics.

Pipeline and Strategic Updates

- Pipeline Milestones: Highlighted positive Phase 3 data readouts for Padcev in muscle-invasive bladder cancer and Phase 2 progression-free survival gains for atirmociclib in breast cancer.

- Legal Commitments & Settlements: Secured patent litigation settlement agreements extending the exclusivity of Vyndamax in the US out to 2031. Management noted this substantially de-risks the post-2028 operational outlook.

- Capital Allocation: Management expects to continue prioritizing debt reduction and supporting dividend commitments. No share repurchases have been executed in 2026 to date, and none are projected in current guidance.

Full-Year 2026 Guidance Reaffirmed

Pfizer maintained all components of its full-year outlook despite the first-quarter outperformance:

- Total Revenue: $59.5B to $62.5B (including approximately $5 billion anticipated from COVID-19 products).

- Adjusted Diluted EPS: $2.80 to $3.00.

- Adjusted R&D Expenses: $10.5B to $11.5B.

- Net Cost Savings: On track to hit the majority of the targeted $7.2 billion savings program by the end of 2026.

Pfizer’s Q1 2026 results highlighted a fundamental inflection point as the company transitions into the post-pandemic era. Beyond beating consensus estimates, management detailed several structural and strategic shifts during the earnings call that will dictate long-term operational trajectories:

1. Commercial Reorganization Taking Effect

Starting this quarter, Pfizer fully implemented its newly redesigned global commercial organizational structure. The move is designed to streamline commercial execution, eliminate redundant layers, and optimize specialized field forces to fully integrate the newly acquired oncology pipeline (following the Seagen merger). Preliminary results showed a 5% operational decline in Selling, Informational, and Administrative (SI&A) expenses, showcasing early progress in structural cost containment.

2. Prioritizing Debt Reduction and Shifting Capital Allocation

In response to the prevailing interest rate environment, Pfizer explicitly prioritized debt reduction and supporting dividend commitments over other capital allocation strategies.

- Management reaffirmed that no share repurchases will be executed in fiscal year 2026.

- With gross leverage sitting at roughly 2.8x at quarter-end, the company deployed its $2.6 billion operational cash flow primarily to cover its quarterly dividend obligations ($2.4 billion). It plans to continue paid-downs on debt using operating income and proceeds from non-core asset divestments, such as the $1.875B received from ViiV Healthcare this quarter.

3. Gross Margin Compression via Royalty Dynamics

While top-line numbers beat expectations, the adjusted gross margin for the quarter compressed to approximately 76%. This margin pressure was driven by product mix shifts and an increase in accrued royalty expenses. Additionally, Q1 2025 benefited from a favorable royalty estimation adjustment, which created a high year-over-year comparison base.

4. Significant Patent Litigation Settlement De-risking 2028+

The most material operational de-risking event of the quarter involved a comprehensive patent litigation settlement for Pfizer’s key rare disease blockbusters, Vyndaqel and Vyndamax.

- The settlement successfully secures market exclusivity for the franchise in the United States out to 2031.

- Management stressed that this resolution significantly mitigates loss-of-exclusivity (LOE) risks post-2028, substantially increasing confidence in achieving high single-digit revenue compound annual growth rates (CAGR) from 2029 through 2031.

5. Highly Focused R&D Pipeline and Obesity Timelines

Pfizer consolidated its R&D budget to aggressively back areas with established commercial infrastructure: Oncology, Metabolic Diseases (Obesity), and Vaccines.

- Obesity Strategy: Management emphasized its conviction in the next-generation pipeline assets acquired via the Metsera transaction (including the ultra-long-acting GLP-1 receptor agonist berobenatide). Pfizer expects to initiate up to 10 pivotal obesity trials in 2026, targeting an initial commercial approval by 2028.

- Oncology Momentum: The company cleared 3 positive Phase 3 data readouts this quarter (including impressive data for Padcev in muscle-invasive bladder cancer). Pfizer’s broader 2026 oncology catalysts include 20 pivotal study initiations, 8 major data readouts, and 4 regulatory decisions slated for the remainder of the year.

According to Pfizer’s latest Q1 2026 earnings release and executive commentary, the sequential and year-over-year growth trajectory for the upcoming quarter (Q2 2026) and the remainder of the fiscal year will be propelled by commercial scaling of new launches, clinical trial readouts, and oncology milestones as the pandemic-era comparisons finish bottoming out.

The primary near-term growth catalysts include:

1. Commercial Scaling of the Core Non-COVID Portfolio

Several non-COVID blockbusters that demonstrated strong momentum in Q1 are expected to accelerate market penetration next quarter:

- Padcev (Urothelial Cancer): Growth will continue to be driven by robust uptake in the first-line locally advanced or metastatic urothelial cancer (la/mUC) setting, alongside continued commercial expansion into cisplatin-ineligible muscle-invasive bladder cancer (MIBC).

- Nurtec ODT (Migraine): Pfizer expects to sustain high double-digit prescription growth by leveraging its massive primary care field force to capture additional market share across both acute and preventive migraine indications.

- Vyndaqel/Vyndamax Franchise (Rare Disease): With the US patent litigation settlement effectively removing medium-term generic headwinds, management expects steady revenue expansion driven by higher diagnosis rates and expanding international access.

2. Oncology Catalysts: ASCO Presentations and Regulatory Progress

Pfizer is positioned to showcase pivotal clinical data at the upcoming American Society of Clinical Oncology (ASCO) Annual Meeting (late May to early June), which will serve as a significant catalyst for institutional sentiment and pipeline valuation:

- Talzenna in Combination with Xtandi: Following positive Phase 3 top-line results for the first-line treatment of HRRm metastatic castration-sensitive prostate cancer (mCSPC), Pfizer will present detailed data next quarter and accelerate regulatory filings.

- Braftovi Combination Therapies: Additional survival data from the Phase 3 BREAKWATER trial evaluating Braftovi regimens in first-line BRAF-mutant colorectal cancer are expected to mature mid-year.

- Next-Gen Bispecifics and ADCs: Pfizer plans to initiate multiple pivotal Phase 3 trials next quarter for its promising PD-1xVEGF bispecific antibody (PF-08634404), targeting first-line non-small cell lung cancer (NSCLC) and first-line colorectal cancer.

3. Moving Elrexfio Into Earlier Lines of Therapy

- At the end of Q1, Elrexfio met its primary endpoint in the Phase 3 MagnetisMM-5 trial, demonstrating a statistically significant improvement in progression-free survival (PFS) for patients with relapsed or refractory multiple myeloma. Pfizer plans to submit these data to regulatory authorities next quarter to move this asset into earlier lines of treatment, substantially expanding its addressable patient population.

4. Mid-Year Obesity Pipeline Milestones (Metsera Assets)

- The commercial focus on Pfizer’s metabolic pipeline will intensify mid-year with the highly anticipated Phase 2b (VESPER-3) data readout for berobenatide (PF-08633944), the ultra-long-acting, once-monthly GLP-1 receptor agonist acquired via Metsera.

- Strong tolerability and competitive efficacy data will position Pfizer to challenge current weekly injectables. Management is on track to initiate up to 10 pivotal clinical studies across the broader obesity pipeline before the end of 2026.

5. Acceleration of Reorganization Cost Efficiencies

- As the newly implemented global commercial operating model fully stabilizes, the cost-saving benefits are expected to manifest more prominently next quarter. Continued reductions in Selling, Informational, and Administrative (SI&A) expenses will help expand operating margins, providing stronger bottom-line leverage to offset the lower gross margins from shifting product mixes.

Pfizer functions as a textbook high-yield, defensive value stock. It is highly attractive for income-oriented portfolios seeking stable cash flows, but less compelling for growth-driven investors looking for rapid capital appreciation over the next 6 to 12 months.

Here is the professional breakdown of Pfizer’s investment thesis and potential upside:

Potential Stock Price Upside Analysis

With Pfizer trading at approximately $25.33 per share (as of mid-May 2026):

- Consensus Target Price: Wall Street analyst estimates average between $29.24 and $29.57.

- Implied Upside Potential: Approximately 13.5% to 16.7% from current levels.

- Bull Case Scenario ($36.00 / ~42% Upside): Triggered if mid-year clinical readouts for the obesity pipeline show best-in-class efficacy and safety, prompting significant valuation multiple expansion.

- Bear Case Scenario ($24.00 / ~5.2% Downside): Driven by unexpected regulatory delays or steeper-than-expected commercial erosion from legacy drug losses of exclusivity (LOE).

Investment Thesis: Why to Hold / Accumulate (Tailwinds)

- High Dividend Yield Offers Strong Downside Protection: Pfizer currently sports a forward dividend yield of 6.7% to 6.8%, one of the highest in the large-cap pharma sector. This high payout acts as a strong valuation floor and provides superb cash flow insulation during market volatility.

- Historically Depressed Valuation: Trading at a forward P/E of roughly 9.3x, Pfizer is priced at a steep discount compared to the broader healthcare sector average of 18.7x and its own 5-year historical average (10.21x). Most of the post-COVID earnings contraction risks are already fully priced in.

- Oncology Integration is Executing Successfully: The Seagen acquisition is beginning to pay off. The non-COVID portfolio grew 7% this quarter, led by Padcev, proving that Pfizer has a viable commercial bridge to sustain long-term growth past 2028.

- De-risking of Key Patent Cliff: The recent patent litigation settlement extending Vyndamax’s US exclusivity to 2031 removes a major cloud of uncertainty that had previously depressed the stock’s long-term terminal value.

Risks and Bottlenecks: Why to Avoid Chasing Aggressively (Headwinds)

- Near-Term Earnings Lack Growth Catalysts: Full-year 2026 guidance (EPS of $2.80–$3.00) indicates flat-to-slightly-negative growth compared to 2025. This explains why the stock price hasn’t reacted explosively to the Q1 earnings beat—institutional investors are waiting for sustainable, top-line organic growth.

- Absence of Share Repurchases: Because management is prioritizing debt payoff and dividend preservation over buybacks in 2026, EPS will receive no artificial boost from a shrinking share count. Growth must come entirely from operational performance.

- High R&D Spending Consumes Short-Term Margins: Allocating $10.5B to $11.5B to R&D this year to aggressively advance the metabolic (Metsera) and oncology portfolios will keep a tight lid on net income and operational margins for the next few quarters.

Strategic Conclusion & Actionable Advice

- Suitable For: Income investors, retirement funds, and conservative value portfolios that prioritize a near-7% annualized dividend yield while waiting for a long-term valuation rerating. The $25 level represents a fundamentally sound entry point for defensive capital.

- Unsuitable For: Growth and momentum traders who expect a stock price doubling or sharp near-term gains.

Pfizer is in a multi-quarter “bottoming out” transition phase. The primary near-term catalyst to watch is the mid-year Phase 2b clinical readout for berobenatide. If this once-monthly obesity drug delivers data superior to currently marketed weekly options, it will be the defining trigger needed to break the stock out toward the $30+ range.

Source:

- https://s206.q4cdn.com/795948973/files/doc_financials/2026/q1/Q1-2026-PFE-Earnings-Release-FINAL.pdf

- https://s206.q4cdn.com/795948973/files/doc_financials/2026/q1/Q1-2026-Earnings-Conference-Call-Prepared-Remarks-FINAL.pdf

- https://seekingalpha.com/news/4585990-pfizer-expects-59_5b-62_5b-2026-revenue-cites-postminus-2028-high-single-digit-cagr

- https://hk.investing.com/news/transcripts/article-93CH-1443081

- https://www.cmoney.tw/notes/note-detail.aspx?nid=1186988

Back to Pfizer page