The century-long history of Lowe’s can be divided into several key eras:

Founding and Early Years (1921-1945)

In 1921, Lucius Smith Lowe founded the first Lowe’s North Wilkesboro Hardware store in North Carolina, initially selling hardware, construction materials, groceries, and agricultural supplies. After his son-in-law Carl Buchan took over management in 1940, the company began narrowing its focus toward building materials and hardware retail.

Post-War Transformation and Rapid Expansion (1946-1970s)

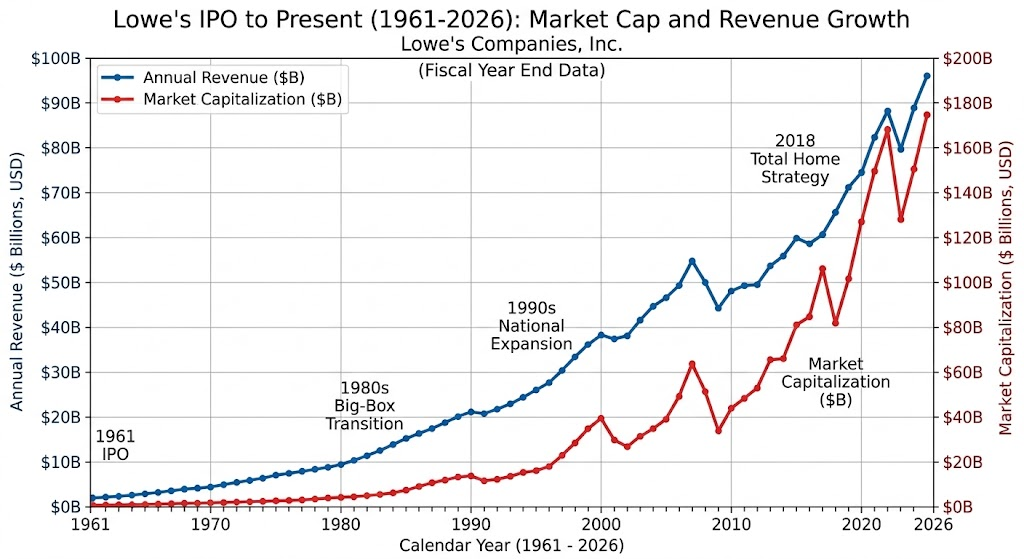

Following World War II, the United States experienced a baby boom and a massive housing development surge. Anticipating a boom in building supply demand, Buchan guided the company to specialize in hardware and construction material wholesaling. Lowe’s went public in 1961 and introduced modern chain-store operating models, rapidly opening locations across the southeastern United States to serve local professional builders.

Shift to Big-Box Format and National Competition (1980s-1990s)

Faced with the rise of Home Depot’s big-box warehouse format in the late 1970s, Lowe’s underwent a major retail transformation. Starting in the 1980s, Lowe’s began converting its smaller traditional stores into massive, one-stop home improvement superstores. Throughout the 1990s, the company accelerated national expansion, successfully growing beyond its southeastern roots.

Modernization, Digitalization, and Total Home Strategy (2000s-Present)

Entering the 21st century, Lowe’s expanded its footprint across North America and invested heavily in e-commerce platforms. Since current CEO Marvin Ellison took the helm in 2018, the company has driven its “Total Home” transformation strategy. This initiative focuses on boosting services for professional contractors (Pro), streamlining the supply chain, and integrating AI technology to enhance store operations and online shopping, securing its position as the world’s second-largest home improvement retailer.

The competitive analysis for Lowe’s primarily focuses on its fierce duopoly with the industry leader, Home Depot, alongside secondary pressures from regional chains, specialty retailers, and e-commerce platforms.

Core Competitive Landscape: Lowe’s vs. Home Depot

Within the North American home improvement market, which exceeds 900B dollars, Home Depot and Lowe’s stand as the two undisputed giants. Both companies maintain distinct positions regarding customer mix, financial scale, and strategic execution:

1. Customer Mix and Revenue Scale

- Home Depot: The market leader (market cap around 380B dollars). Its customer base historically leans toward the Professional Contractor (Pro) segment, which generates nearly half of its revenue. This focus gives Home Depot a higher average ticket size and superior sales per square foot compared to Lowe’s.

- Lowe’s: The global number two (market cap around 158B dollars, with annual revenue around 86B dollars). It traditionally caters to the Do-It-Yourself (DIY) consumer, who accounts for roughly 75% of its total sales. This reliance makes Lowe’s revenue more sensitive to fluctuations in broader consumer spending, inflation, and general housing market trends.

2. Category Strengths and Brand Positioning

- Lowe’s: Holds the number one market share in Major Appliances, home decor, and flooring. It enjoys strong brand affinity among female consumers and suburban households looking for aesthetic upgrades.

- Home Depot: Possesses a commanding lead in core structural categories like lumber, heavy building materials, and professional-grade power tools, making it the default choice for large-scale construction jobs.

3. Recent Strategic Divergence (2025-2026)

- Home Depot Doubling Down on the “Wholesale Pro Ecosystem”: Home Depot has bypassed traditional retail store limitations by acquiring heavyweights like SRS Distribution and GMS to sell directly to large-scale specialty builders. They have also rolled out AI-driven tools, such as the Material List Builder, to lock in commercial accounts.

- Lowe’s “Total Home Strategy and Omnichannel Balance”: Lowe’s is aggressively expanding its own Pro market penetration through loyalty initiatives like MyLowe’s Pro Rewards and its recent acquisitions of FBM (Foundation Building Materials) and ADG. However, Lowe’s prioritizes a balanced ecosystem, actively engaging over 30 million DIY customers through its “MyLowe’s Rewards” program and rolling out specialized rural formats to capture market share from smaller, rural lifestyle retailers.

Key Competitive Metrics Comparison

| Metric | Lowe’s Companies (LOW) | Home Depot (HD) |

| Market Position | 2nd largest in the US, holds ~12% market share | 1st largest in the US, undisputed industry leader |

| Core Customer Mix | Lean DIY (~75%), rapidly scaling up Pro | Lean Pro (~50%), enjoying high loyalty and spending |

| Geographic Footprint | Concentrated in the US (exited Canadian market recently) | Footprint spans the US, Canada, and Mexico |

| Logistics & Delivery | Finalized its “Market-Based Delivery” network, shipping bulky items directly to sites without touching stores | Operates a vast, proprietary distribution network optimized for commercial job sites |

| Digital & AI Focus | Customer experience oriented (e.g., virtual kitchen planning, spatial computing) | Project management oriented (e.g., automatic blueprint estimation and material lists) |

Other Notable Competitors

Beyond Home Depot, Lowe’s faces pressure from three alternative retail channels:

- Regional Home Improvement Chains (e.g., Menards): Possessing an incredibly strong footprint in the US Midwest, Menards uses low-price positioning and a diverse product assortment to apply local pressure on Lowe’s.

- Specialty & Farm Retailers (e.g., Tractor Supply): Dominant in rural and exurban North American markets. Lowe’s has directly countered this threat by adding a dedicated “Rural Living” assortment to over 500 of its stores.

- E-commerce & Mass Merchandisers (e.g., Amazon, Walmart): Online platforms continue to siphon off casual DIY shoppers for commoditized products like small hardware items, basic lighting fixtures, and hand tools due to convenience and competitive pricing.

Conclusion

Lowe’s is leveraging its Total Home strategy to close the operational gap with its primary rival. While fully dismantling Home Depot’s deep commercial Pro moat remains a long-term challenge, Lowe’s is successfully defending its DIY stronghold. By capitalizing on its dominance in appliances, expanding its online ecosystem (which now drives 13% of sales), and rolling out high-performing rural store concepts, Lowe’s continues to secure steady growth among small-to-midsize contractors.

Source:

- https://corporate.lowes.com/

- https://corporate.lowes.com/who-we-are

- https://www.homedepot.com/

- https://www.google.com/finance/beta/quote/HD:NYSE

Back to Lowe page