The history of Lockheed Martin can be divided into four distinct phases:

Foundation and Early Pioneering (1910s–1930s)

Lockheed and Martin began as separate entities. Glenn L. Martin founded the Martin Company in 1912, producing early military trainers. That same year, the Loughead (later changed to Lockheed) brothers built their first aircraft, establishing their manufacturing company in 1926. During this era, both companies pushed early aviation boundaries, laying the groundwork for advanced aerospace engineering.

WWII and Cold War Expansion (1940s–1980s)

World War II catalyzed massive growth for both companies. Lockheed produced the iconic P-38 Lightning and later established its famed “Skunk Works” division, which developed legendary reconnaissance aircraft like the U-2 and SR-71 Blackbird. Meanwhile, the Martin Company expanded into missiles and space exploration, developing the Titan rocket series. Both became pillars of U.S. defense technology during the Cold War.

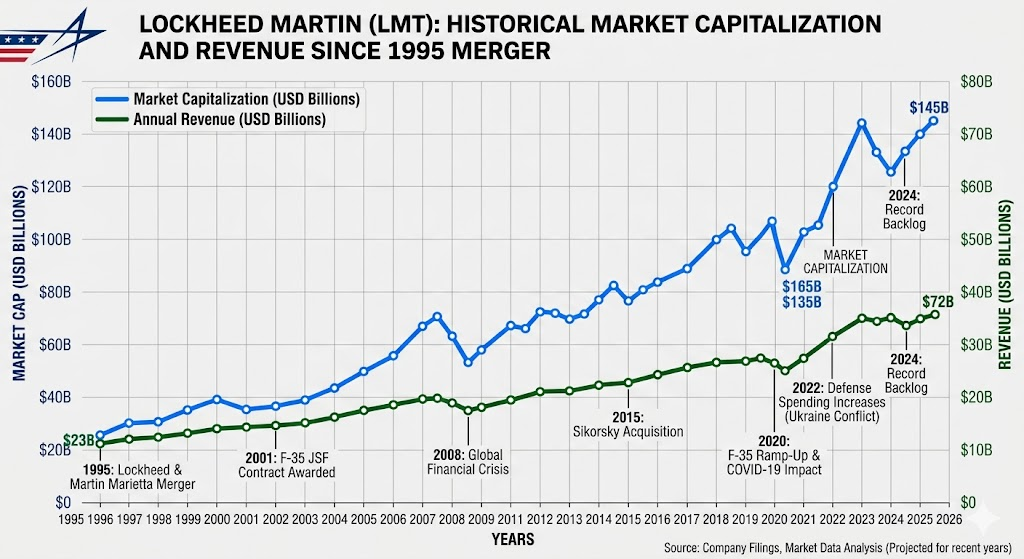

The Mega-Merger and Consolidation (1990s)

The end of the Cold War led to sharp declines in U.S. defense spending, triggering industry consolidation. In 1995, Lockheed Corporation and Martin Marietta merged to form Lockheed Martin. This historic merger combined their massive portfolios, positioned the new entity as the world’s largest defense contractor, and ultimately secured the Joint Strike Fighter contract, which produced the F-35 Lightning II.

21st Century Tech and Joint-Domain Defense (2000s–Present)

In the modern era, Lockheed Martin solidified its air superiority with the F-22 Raptor and F-35 programs, and expanded its rotary capabilities by acquiring Sikorsky Aircraft in 2015. To address evolving security threats, the corporation has evolved beyond traditional hardware manufacturing into an integrated technology powerhouse, heavily investing in hypersonics, artificial intelligence, cybersecurity, and autonomous systems.

Lockheed Martin’s competitive landscape is defined by its position as the world’s largest defense contractor. Its market dynamics are analyzed across its four primary business segments, where it competes against fellow defense primes, European conglomerates, and agile commercial tech disruptors.

Aeronautics

Aeronautics is the flagship segment, generating nearly forty percent of the company’s revenue, driven primarily by dominance in fifth-generation fighter technology.

- Strategic Position: Lockheed Martin holds a near-monopoly on Western fifth-generation stealth fighters with the F-35 Lightning II and F-22 Raptor, backed by a massive international order backlog.

- Key Competitors:

- Boeing: Competes with the F/A-18 Super Hornet and F-15EX Eagle II. While Boeing faces commercial headwinds, it remains a robust competitor in military transport, refueling tankers (KC-46), and trainer jets.

- Northrop Grumman: Dominates the strategic bomber market with the B-21 Raider and serves as a major subcontractor on the F-35 program, specializing in stealth fuselage components and airborne radar.

- Dassault Aviation (France): A potent European rival capturing market share in non-US aligned nations with its Rafale fighter jet.

Missiles and Fire Control (MFC)

This segment focuses on precision-guided weapons, air defense hardware, and tactical missiles.

- Strategic Position: The company is a premier provider of high-demand platforms like the HIMARS, GMLRS, and Patriot PAC-3 missiles.

- Key Competitors:

- RTX (formerly Raytheon Technologies): The most direct rival in this space. The two companies share a complex relationship of co-opetition; for instance, RTX manufactures the radar and systems integration for the Patriot air defense system, while Lockheed Martin supplies the PAC-3 interceptor missiles. RTX also leads in missile seekers, electronic warfare, and counter-UAS technology.

- Boeing: Competes with precision ammunition configurations, such as the Small Diameter Bomb (SDB) and Joint Direct Attack Munition (JDAM) kits.

Rotary and Mission Systems (RMS)

Centered around Sikorsky Aircraft (acquired in 2015), this segment produces legendary military helicopters and naval combat systems like the Aegis Combat System.

- Strategic Position: Sikorsky’s UH-60 Black Hawk remains the global standard for utility helicopters, though the segment faces long-term headwinds in future vertical lift modernization.

- Key Competitors:

- Textron (Bell): A major threat to Sikorsky’s long-term dominance, having secured the U.S. Army’s Future Long-Range Assault Aircraft (FLRAA) contract with its V-280 Valor tiltrotor platform.

- Boeing: Produces heavy-lift and attack portfolios, specifically the CH-47 Chinook and AH-64 Apache helicopters.

- Airbus Helicopters (Europe): Competes aggressively in the global military and paramilitary utility helicopter markets outside the United States.

Space

This segment covers military satellites, space launch services, and strategic missile defense interceptors.

- Strategic Position: Lockheed Martin is the prime contractor for the Fleet Ballistic Missile program and NASA’s Orion spacecraft, while co-owning the United Launch Alliance (ULA) with Boeing.

- Key Competitors:

- Northrop Grumman: Holds a dominant position in solid rocket boosters, strategic deterrence architecture, and military space payload manufacturing.

- SpaceX: Actively disrupting the segment. With reusable launch capabilities and its military-focused Starshield network, SpaceX is capturing high-priority low-Earth orbit (LEO) satellite constellations and national security launch contracts that historically went to legacy primes.

Competitive Advantages and Vulnerabilities

- Moat: Irreplaceable system integration capabilities, deep institutional trust with the Pentagons of allied nations, and the unmatched revenue generation of the F-35 program.

- Risks: Supply chain bottlenecks affecting aircraft delivery cadences, labor constraints, and emerging defense-tech unicorns (like Anduril Industries or SpaceX) attempting to displace traditional hardware primes through rapid, software-first development cycles.

Source:

Back to Lockheed Martin page