Key Changes and Strategic Highlights: JPMC Q4 2025

Based on the 2025 fourth quarter earnings report, the most significant shifts and performance highlights for JPMorgan Chase are as follows:

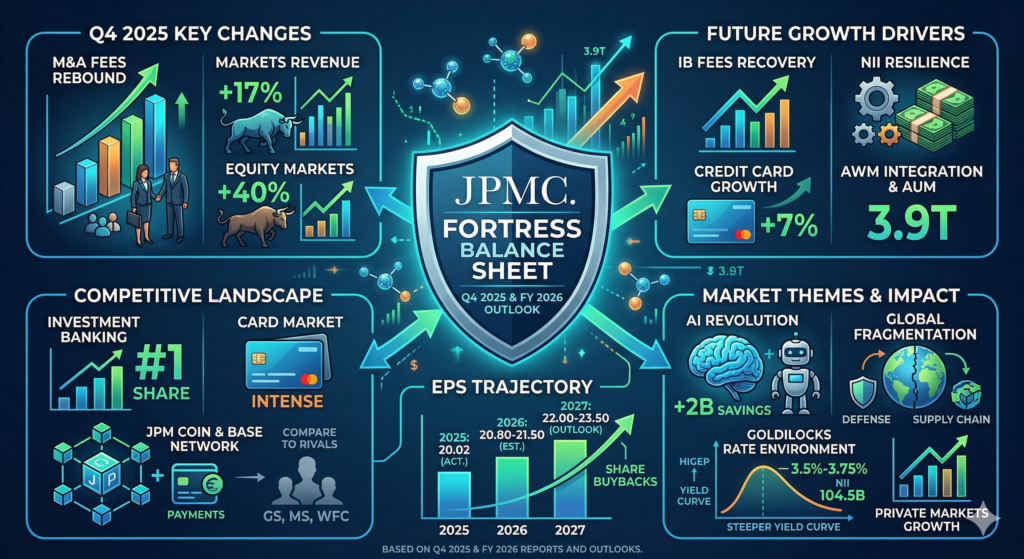

Revenue Driven by Surging Market Activity

The most prominent growth driver this quarter came from Markets revenue within the Investment Bank, which saw a 17% year-over-year increase. Notably, Equity Markets revenue soared by 40%, reflecting the bank’s strong trading performance amid heightened market volatility and increased client activity.

Strengthening of the Balance Sheet

The bank’s capital adequacy continued to improve, with the CET1 capital ratio reaching 15.3%, up from 15.0% in the prior year. This fortress balance sheet allows JPMorgan Chase to maintain operational resilience while returning significant value to shareholders. Book value per share rose 9% year-over-year to 116.32.

Shifting Credit Costs and Asset Quality

The provision for credit losses stood at 3.1B, indicating that while current credit conditions remain healthy, the bank maintains a cautious stance toward macroeconomic uncertainty. This figure reflects adjustments based on loan growth and the evolving economic outlook.

Robust Core Profitability

Excluding specific items (such as those related to Visa transactions or FDIC special assessments), the bank demonstrated exceptional operating efficiency. The adjusted Return on Tangible Common Equity (ROTCE) reached 24%, showcasing the strength of its core earning power even as the interest rate environment shifts.

Returns on Payments and Technology Investments

In the Consumer & Community Banking (CCB) segment, card services sales volume grew by 7% year-over-year, highlighting the continued resilience of consumer spending. Simultaneously, ongoing investments in payment technology and data platforms have contributed to steady gains in market share.

Future Growth Drivers

Based on the outlook and management commentary in the financial documents, the growth momentum for JPMorgan Chase in the coming quarters is primarily centered on the following areas:

Recovery in Investment Banking and Market Activity

While investment banking fees saw a slight decline for the full year 2025, the fourth quarter showed clear signs of a rebound. As the market environment stabilizes, the backlog of mergers and acquisitions (M&A) and IPO activity is expected to be further unleashed. Additionally, the strong momentum in Equity Markets during the fourth quarter (up 40%) is anticipated to carry over into the first quarter of 2026.

Resilience of Net Interest Income (NII)

Despite the challenges posed by a changing interest rate environment, JPMorgan Chase expects full-year 2026 Net Interest Income to be approximately 91B. This is supported by continued growth in loan balances and flexible balance sheet management. Management specifically noted that while deposit costs may rise, asset repricing will provide a significant buffer.

Consumer Spending and Credit Growth

The Consumer & Community Banking (CCB) segment continues to see growth in card services sales volume (up 7% year-over-year). With consumer confidence remaining steady, the growth in credit card revolving balances and the expansion of the payments business will serve as core growth engines for the retail banking division.

Scalability of Payment Technology and Data Platforms

The bank continues to invest billions of dollars in technological innovation, particularly in modernizing payment platforms and AI applications. These investments are designed to enhance operating efficiency and capture more market share. As these platforms scale, they are expected to translate into more significant non-interest income.

Integration and Asset Management Expansion

Through ongoing business integration and client acquisition strategies, particularly in Asset & Wealth Management (AWM), the bank’s Assets Under Management (AUM) have reached 3.9T. The continued inflow of client assets and the increasing demand for advisory services will drive steady fee-based revenue.

Shifts in the Competitive Landscape

According to market data from Q4 2025 and early 2026, JPMorgan Chase (JPMC) maintains a “dominant lead with intensifying competition in niche segments.” The key competitive shifts are as follows:

1. Fluctuations in Investment Banking Market Share

Although JPMC retained its position as the world’s #1 in investment banking fees for 2025 (with an 8.4% market share), its growth performance in the fourth quarter showed a gap compared to its primary rivals:

- Competitive Shift: JPMC’s investment banking fees decreased by 5% in Q4, while Morgan Stanley saw a massive 47% increase and Goldman Sachs grew by 25%.

- Analysis: This indicates that during the early stages of the market recovery, Goldman and Morgan Stanley benefited more rapidly from the surge in M&A and underwriting activity, whereas JPMC showed a steadier but slightly lagged growth curve.

2. Strategic Pivot in Payments and Blockchain

JPMC is shifting its competitive focus toward “platformization” to solidify its dominance in wholesale payments:

- New Momentum: This quarter saw the official launch of JPM Coin (a USD deposit token) on the Base network, with substantive transaction partnerships established with Mastercard and Coinbase.

- Strategic Goal: This demonstrates that JPMC’s competitors are no longer limited to traditional banks; it is now vying for dominance in 24/7 real-time settlement against emerging fintech players.

3. “Red Ocean” Competition in the Card Market

Management emphasized during the earnings call that the credit card ecosystem has become “extraordinarily intense”:

- Market Share Battle: While JPMC’s card sales volume grew 7%, rivals including Wells Fargo also reported 7% growth in retail revenue, driven by strong card business performance.

- Resource Allocation: To counter this, JPMC plans to invest approximately 19.8B in technology and AI in 2026. The focus will be on “hyper-personalization” in consumer banking to widen the gap between JPMC and mid-tier banks.

4. The “Arms Race” in Wealth Management

As global capital markets rose, all major banks intensified their pursuit of wealth management clients:

- Scale Comparison: JPMC’s Assets Under Management (AUM) reached 3.9T, but Morgan Stanley demonstrated exceptional gathering power, adding 122B in net new assets in Q4 alone.

- Focus of Competition: Market competition has shifted from simple commission-based models to a race for “asset inflow velocity” and the breadth of alternative investment products (such as private equity).

Competitive Summary Table

| Competitive Field | JPMC Current Status | Competitor Dynamics |

| Investment Banking | Global #1 share, but quarterly growth slowed | Goldman and Morgan Stanley showed higher elasticity in M&A recovery |

| Retail & Cards | Robust sales growth of 7% | Wells Fargo and others increasing promotions; competition is white-hot |

| Tech Innovation | 19.8B investment; leading in blockchain settlement | Fintechs and big banks are all entering real-time payments |

| Wealth Management | AUM reached 3.9T | Morgan Stanley’s asset inflows are extremely rapid, with margins nearing 30% |

Market Themes and Investment Narratives

According to the latest 2026 market reports and investment outlooks from JPMorgan Chase, the market is currently laser-focused on these four core themes:

1. The “Micro to Macro” Transition of Artificial Intelligence (AI)

The market has shifted focus from AI technology itself to its structural impact on the real economy.

- Key Direction: Investors are searching for companies that can convert AI into actual “productivity” and “revenue.”

- JPMC Insight: AI is the most significant transformative force in 2026, yet caution is advised regarding “excessive enthusiasm.” Attention should be paid to industries providing infrastructure (power, digital construction), as the energy sector has become a critical bottleneck in the AI revolution.

2. Global Fragmentation and Resilient Investing

The era of “seamless globalization” has ended. Markets are restructuring assets in response to geopolitical shifts.

- Key Direction: The global order is splitting into competing blocs, making supply chain security, defense, and energy self-sufficiency paramount.

- Investment Narratives:

- Defense Spending: Specifically, European defense spending is shifting from “peace dividends” to “conflict-related capital expenditure.”

- Resource Security: Investing in regions like South America that possess critical minerals and resources.

- Resilience over Efficiency: Corporate strategies are no longer just about the lowest cost, but about the stress-resistance of supply chains.

3. Structural Inflation and the “Goldilocks” Rate Environment

While inflation has retreated from its peaks, the old “low inflation, low interest rate” norm has not returned.

- Key Direction: Markets are adapting to a more volatile inflation environment with a higher baseline.

- Upside for Banking: 2026 is viewed as a “Goldilocks” period for the banking sector. As the Federal Reserve stabilizes rates between 3.50% and 3.75%, the yield curve is steepening (long-term rates higher than short-term), which significantly expands Net Interest Margins (NIM) for banks.

- Refinancing Wave: Markets expect that as rates stabilize, corporations will initiate large-scale debt refinancing, generating substantial fee income for banks.

4. Capital Market Polarization and Private Market Potential

Markets are moving away from highly concentrated growth (such as mega-cap tech) toward broader opportunities.

- Key Direction: Significant attention is being paid to the potential of “private assets” including private equity, credit, and infrastructure.

- Investment Pivot: Due to increased volatility in public markets, asset managers are directing capital toward alternative investments that offer stable cash flows. Additionally, with the expected rebound in M&A activity in 2026, related themes have returned to the spotlight.

Summary of Market Themes

| Core Theme | Key Focus | Significance for Investors |

| AI Revolution | Productivity conversion, power, and energy infrastructure | Shift from “concept stocks” to “application and infrastructure stocks” |

| Global Fragmentation | Supply chain reshoring, defense, and energy security | Prioritize asset safety and resilience over pure efficiency |

| Rate Environment | Steepening yield curve, 3.5%+ “new normal” rates | Positive for the profitability of major banks like JPM |

| Inflation Shift | Structurally higher inflation, tangible asset value | Need for diversification (e.g., commodities, real estate) to hedge inflation |

Impact of Market Themes on JPMC

The four major market themes act not just as external shifts but as critical catalysts for JPMorgan Chase (JPMC) to further solidify its “fortress” status in 2026. Here is the specific impact analysis:

1. AI Revolution: Transitioning from CapEx to Profit Returns

JPMC’s leadership in AI is converting into tangible financial advantages.

- Direct Financial Impact: CEO Jamie Dimon has noted that the bank’s annual 2B investment in AI research and development has already generated approximately 2B in direct cost savings (through error reduction, automation, etc.), achieving a 1:1 return on investment.

- Long-term Operational Impact: With a 2026 technology budget of 19.8B, JPMC is enhancing productivity and risk control. Markets believe this scale provides a long-term margin advantage over mid-tier banks that cannot afford such massive R&D outlays.

2. Global Fragmentation: Driving Advisory and Alternative Investment Demand

As the geopolitical focus shifts toward “supply chain resilience” and “resource security,” JPMC serves as a central facilitator for global corporations.

- Business Growth Points: Multinational corporations facing supply chain restructuring are driving demand for M&A advisory and balance sheet management.

- Asset Allocation Shift: With energy security taking center stage, JPMC’s financing and advisory services in LNG, renewables, and grid modernization have increased significantly. This attracts more clients to JPMC’s “Private Markets” portfolio as they seek hedges against global volatility.

3. “Goldilocks” Rate Environment: Expanding Net Interest Margin (NIM)

A stable Federal Funds Rate between 3.5%-3.75% and a steepening yield curve represent a major tailwind for JPMC.

- Optimized Profit Structure: Compared to the uncertainty of 2025, a stable high-rate environment allows JPMC to better manage deposit costs and loan pricing.

- Clear Guidance: JPMC forecasts 2026 Net Interest Income (NII) to reach approximately 104.5B (with approximately 95B excluding the Markets business), reflecting confidence that the current rate environment will translate into stable earnings.

4. Private Markets and M&A Recovery: Surge in Fee Income

Market focus on private equity and credit directly benefits JPMC’s Investment Banking and Asset Management divisions.

- Fee Rebound: As M&A activity and the IPO pipeline strengthen in 2026, JPMC—ranking first in global investment banking market share—is poised to capture high-margin fee revenue.

- AUM Growth: As capital flows toward “alternative investments,” JPMC’s diverse private market product line helps maintain the growth of its Assets Under Management, which has already reached 3.9T.

Summary of Core Impact on JPMC

The combined effect of these themes is that JPMC is reducing costs through AI, expanding margins through high rates, increasing fees through an M&A rebound, and capturing restructuring opportunities through its global footprint. Consequently, JPMC is viewed in 2026 as a premier investment vehicle that offers both “fortress-like defensiveness” and “growth-oriented offensiveness.”

Future EPS Projections

Based on current market analysis and the guidance issued by JPMorgan Chase (JPMC) in early 2026, the expected trajectory for Earnings Per Share (EPS) is as follows:

1. 2026 EPS Forecast: Steady Growth

According to analyst consensus, JPMC’s 2026 EPS is expected to continue its upward climb from the 20.02 recorded in 2025.

- Growth Expectations: Markets anticipate an EPS growth rate of approximately 7.29%, with a target range falling between 19.42 and 21.50.

- Key Drivers: While Net Interest Income (NII) faces challenges from rising deposit costs, a robust recovery in investment banking fees (particularly M&A and IPO activity) and operational efficiencies gained from AI are seen as the core pillars supporting EPS growth.

2. Impact of the Interest Rate Environment: A Hawkish Outlook

JPMC’s internal economic forecasts currently rank among the most “hawkish” on Wall Street.

- Critical Shift: JPMC economists predict that the Federal Reserve will not cut rates in 2026 and even anticipate a 25-basis-point hike in the third quarter of 2027.

- EPS Effect: If this forecast materializes, the prolonged high-interest-rate environment will favor JPMC by expanding Net Interest Margins (NIM), contributing positively to EPS. However, it is important to note that sustained high rates could eventually dampen loan demand and increase provisions for credit losses.

3. Long-term Trend Over the Next Three Years

The market expects JPMC to achieve a compound annual growth rate (CAGR) for EPS of approximately 7.5% over the next three years.

- Scalability Advantage: Analysts believe that JPMC’s nearly 20B annual technology investment allows it to absorb cost pressures more effectively than its competitors.

- Capital Returns: With the CET1 capital ratio maintaining a high level of 15.3%, the bank has significant room for share buybacks, which will further drive up EPS by reducing the total number of shares outstanding.

EPS Trajectory Reference Table

| Year | Estimated EPS (USD) | Key Observations |

| 2025 (Actual) | 20.02 | Driven by a 40% surge in Equity Markets revenue |

| 2026 (Est.) | 20.80 – 21.50 | Recovery in IB fees; AI-driven cost savings |

| 2027 (Outlook) | 22.00 – 23.50 | M&A market maturation; full realization of digital transformation |

Source:

- J.P. Morgan Payments Q4 2025 Highlights

- GS and MS Q4 Earnings Surge Analysis

- JPMorgan Chase 2026 Outlook – Stock Titan

Back to JP Morgan page