Here is the summary of Gilead Sciences’ (NASDAQ: GILD) Q1 2026 financial results announced on May 7, 2026.

Core Financial Performance

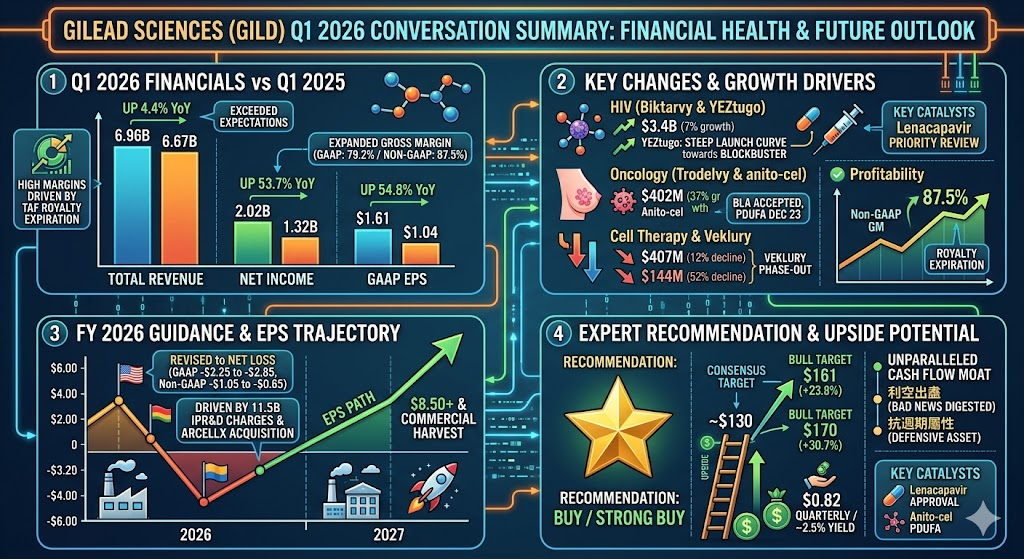

| Metric | Q1 2026 | Q1 2025 | YoY Change |

| Total Revenue | 6.96B | 6.67B | 4.4% |

| Net Income | 2.02B | 1.32B | 53.7% |

| GAAP Diluted EPS | $1.61 | $1.04 | 54.8% |

| Non-GAAP Diluted EPS | $2.03 | $1.81 | 12.2% |

- Both revenue and earnings exceeded Wall Street expectations (consensus estimates were 6.91B for revenue and $1.91 for Non-GAAP EPS).

- Gross margin expansion: GAAP product gross margin increased to 79.2% (up from 76.7% in Q1 2025), and Non-GAAP product gross margin rose to 87.5% (up from 85.5%), primarily driven by a richer product mix and the expiration of certain royalty obligations.

- Cash position: As of March 31, 2026, cash, cash equivalents, and marketable debt securities totaled 8.6B, down from 10.6B at the end of 2025. Operating cash flow grew by approximately 45% year-over-year.

Product & Segment Breakdown

- HIV Franchise (Up 10% YoY to 5.03B)

- Biktarvy sales grew 7% to 3.4B, maintaining a dominant market share of over 52% in the U.S. HIV treatment market.

- Descovy sales surged 38% to 807M, propelled by higher demand and increased average realized price.

- Oncology & Liver Disease

- Trodelvy (breast cancer treatment) sales jumped 37% to 402M, supported by strong baseline demand, favorable inventory dynamics, and higher average realized prices.

- Liver Disease portfolio sales edged up 1% to 767M, buoyed by the launch and scaling of Livdelzi, which offset declines in chronic hepatitis C virus (HCV) sales and inventory adjustments.

- Cell Therapy faced increased in-class and out-of-class competition, falling 12% to 407M (Yescarta down 14% to 332M; Tecartus down 4% to 75M).

- Veklury (remdesivir)

- Sales dropped 52% to 144M, reflecting lower global hospitalization rates for COVID-19.

Full-Year 2026 Guidance Update

While Gilead raised its total product sales targets for the year, it sharply adjusted its EPS guidance down into negative territory due to massive acquisition and collaboration charges.

- Product Sales Guidance: Increased to 30.0B – 30.4B (previously 29.6B – 30.0B).

- Diluted EPS Guidance:

- GAAP EPS: Revised to a loss of $3.25 to $2.85 (previously positive $6.75 to $7.15).

- Non-GAAP EPS: Revised to a loss of $1.05 to $0.65 (previously positive $8.45 to $8.85).

【Key Drivers for the Revision】

The net impact of approximately negative $9.50 per share is a direct result of 11.5B in In-Process Research and Development (IPR&D) impairments, alongside upfront funding and financing costs related to closing the Arcellx acquisition ($7.8B implied equity value) and new strategic transactions with Tubulis and Ouro Medicines.

Dividend Policy

The Board of Directors declared a quarterly cash dividend of $0.82 per share of common stock for the second quarter of 2026. The dividend is payable on June 29, 2026, to stockholders of record at the close of business on June 15, 2026.

Gilead Sciences demonstrated several milestone structural and strategic changes in its Q1 2026 financial results. These shifts not only reshaped the company’s current financial framework but also solidified its future growth engines.

The primary significant changes can be summarized into three core pillars:

1. Dramatic Revision in Financial Guidance: Higher Revenues, Earnings Shift into Negative Territory

This was the most scrutinized revision by the market this quarter. Gilead made divergent adjustments to its full-year 2026 outlook:

- Upward Revision of Revenue Outlook: The full-year product sales guidance was raised to 30.0B – 30.4B (up from the previous estimate of 29.6B – 30.0B). This reflects robust baseline demand for core franchises—particularly HIV and Trodelvy—alongside successful new product introductions.

- EPS Guidance Cut into the Negative:

- GAAP EPS guidance was slashed from the previous positive $6.75 to $7.15 down to a loss of $3.25 to $2.85.

- Non-GAAP EPS guidance was similarly lowered from the previous positive $8.45 to $8.85 down to a loss of $1.05 to $0.65.

【Underlying Drivers for the Revision】

This massive financial impact of approximately negative $9.50 per share does not stem from operational deterioration. Instead, it is due to the concentrated recognition of 11.5B in In-Process Research and Development (IPR&D) impairments, upfront transaction fees, and financing costs during the quarter. These expenses were primarily incurred to complete the full acquisition of Arcellx and advance strategic collaborations with Tubulis and Ouro Medicines.

2. Structural Evolution in Core Portfolio and Pipeline

The product and revenue mix showed a distinct transition this quarter, highlighting the company’s accelerated shift away from “COVID-19 windfalls” toward “long-term, stable antibody and oncology therapeutics”:

- HIV Franchise Dual-Engines and a Rising Star: The core drug Biktarvy sustained a 7% growth rate (reaching 3.4B), while Descovy surged 38% (reaching 807M) driven by pricing dynamics and demand. Furthermore, the newly launched HIV drug YES2GO displayed exceptional momentum. Management noted during the earnings call that the therapeutic is on track to become a 1B blockbuster within its first year of launch, projected to drive full-year HIV franchise growth up to 8%.

- Next-Generation Oncology and Immunology Layout (M&A and Alliances):

- Completion of the Arcellx Acquisition: Closed at $115 per share (implying a 7.8B equity value), giving Gilead full ownership of the core asset anito-cel (for relapsed/refractory multiple myeloma). The FDA has accepted the Biologics License Application (BLA), with a PDUFA target action date set for December 23, 2026.

- Tubulis Acquisition Agreement: Acquired this clinical-stage biotech firm to secure its next-generation Antibody-Drug Conjugate (ADC) technology platforms and lead asset TUB-040 (a Phase 1b/2 candidate for ovarian cancer), strengthening the oncology pipeline.

- Ouro Medicines Collaboration: Licensed gamgertamig (a BCMAxCD3 T-cell engager), marking an expansion into B-cell-driven autoimmune diseases.

- Headwinds in Legacy and Cell Therapy Segments:

- Veklury (COVID-19) Phase-Out: Sales plunged 52% to 144M, effectively marginalizing its impact on total revenues.

- Cell Therapy Contraction: Yescarta and Tecartus faced intense in-class and out-of-class competition, resulting in a 12% year-over-year decline in total Cell Therapy revenue to 407M.

3. Optimization of Underlying Profitability (Margins)

Even though net income was suppressed by the accounting treatments of the M&A transactions, Gilead’s underlying operational quality demonstrated noticeable improvement:

- Substantial Expansion in Product Gross Margin: Non-GAAP product gross margin advanced to 87.5%, up 2 percentage points from 85.5% in the same period last year.

- Driving Factors: This margin expansion was primarily propelled by the expiration of certain royalty-related obligations (preventing profit dilution to external parties) and an increased revenue contribution from higher-margin products like the flagship HIV portfolio and Trodelvy.

Summary:

This quarter represents a pivotal inflection point where Gilead sacrificed short-term paper profitability to secure long-term control over its pipeline. By absorbing 11.5B in acquisition and R&D expenses upfront, the company cleared its financial slate while capturing critical assets in oncology (ADCs), multiple myeloma (anito-cel), and immunology. Meanwhile, the robust performance and strong margins of the underlying HIV business provided the necessary cash flow foundation to support this transition.

In its latest earnings call and financial reports, Gilead Sciences highlighted several core growth drivers for the upcoming quarters, particularly looking into the second half of 2026 and beyond. While short-term paper profitability has turned negative due to the 11.5B acquisition and R&D expenditures, the company’s upward revision of its full-year revenue guidance is firmly backed by the following catalysts:

1. The “Dual-Milestone” Catalyst in the HIV Prevention and Treatment Pipeline

Gilead’s dominance in the HIV sector is poised for another technological upgrade, which will serve as the most critical growth driver over the coming quarters:

- Clinical and Regulatory Progress for Lenacapavir (Every-Six-Month Injection):

- Accelerated Regulatory Review: In late April 2026, the U.S. FDA officially accepted Gilead’s New Drug Application (NDA) for a once-daily Bictegravir / Lenacapavir regimen, granting it Priority Review status. This significantly shortens the review timeline. Regulatory milestones and potential approvals over the next few quarters are expected to be major focal points for investors.

- Expanding Market Moat: As the backbone of long-acting therapeutics, Lenacapavir drastically reduces dosing frequency. Backed by exceptional data from clinical trials (such as the PURPOSE study series), its upcoming market penetration is anticipated to further solidify Gilead’s monopoly in the HIV Pre-Exposure Prophylaxis (PrEP) market, where revenue has already grown 87% year-over-year.

- Commercialization Scaling of YEztugo:

- As a newly launched flagship for long-acting HIV prevention, YEztugo delivered 166M in sales for Q1, representing a stellar quarter-over-quarter growth of 72% and beating consensus estimates. Management expects the drug to maintain a steep launch trajectory in the coming quarters, tracking toward blockbuster status (exceeding 1B in revenue) within its first year on the market to serve as a direct revenue driver for the second half of the year.

2. Unlocking Merged Assets: Arcellx’s Core Asset anito-cel Enters the Commercialization Countdown

Gilead officially finalized its full acquisition of Arcellx on April 28, 2026. The commercial value of this substantial investment is expected to unlock rapidly in the near term:

- PDUFA Target Date Secured: The FDA has accepted the Biologics License Application (BLA) for the core acquired asset, anito-cel (a CAR-T therapy for relapsed/refractory multiple myeloma). The PDUFA target action date has been set for December 23, 2026.

- Second-Half Momentum: As the PDUFA date approaches, Gilead will fully initiate pre-commercialization preparation and channel deployment over the next quarter. This highly disruptive cell therapy is viewed as the key to reversing the current decline in Yescarta sales and reigniting growth across the Cell Therapy segment.

3. Sustained Expansion of Oncology and Liver Disease Rising Stars (Trodelvy & Livdelzi)

- Trodelvy (ADC for Breast and Urothelial Cancer):

- Q1 sales surged 37% to 402M, driven by robust baseline demand in the U.S. market.

- In the upcoming quarters, Trodelvy is projected to capture more market share in second-line Triple-Negative Breast Cancer (TNBC) and HR+/HER2- metastatic breast cancer. As international access and reimbursement materialize in parts of Europe and Asia, overseas expansion will take the baton as a major growth driver.

- Livdelzi (seladelpar, formerly a CymaBay asset):

- Q1 revenue reached 133M, surging more than three-fold year-over-year. This therapeutic for Primary Biliary Cholangitis (PBC) shows high clinical adherence. As market awareness increases, management forecasts a more pronounced surge in patient enrollment over Q2 and the second half of the year.

4. Continuation of Underlying Gross Margin Optimization (Cash Flow Foundation)

- The Non-GAAP product gross margin expanded to 87.5% in Q1, benefited by the expiration of certain external royalty-related obligations.

- This structural improvement is not a short-term anomaly and will continue to bear fruit over the coming quarters. Consequently, every dollar of revenue generated by core operations will yield higher operating cash flow. The financial flexibility provided by these high margins will effectively bankroll the clinical progression and pipeline expansion of newly acquired assets, including Tubulis’s next-generation ADC platform and Ouro Medicines’ immunology assets, in the upcoming quarter.

Summary:

Gilead’s near-term growth will be sustained by immediate revenue contributions from the double-digit commercial scaling of YEztugo and Livdelzi, while the Priority Review progress of Lenacapavir and the pre-launch catalysts for anito-cel ahead of its year-end target provide the upside narrative for valuation expansion.

The EPS trajectory for Gilead Sciences over the next year presents a highly unique V-shaped pattern, best characterized as a “short-term accounting hit, underlying financial windfall, and a powerful rebound the following year.”

To accurately interpret the EPS movement over the next twelve months, one must decouple the reported full-year fiscal 2026 figures from the company’s robust, quarter-by-quarter operational earnings power:

1. Full-Year 2026 Guidance: Shifting into Negative Territory on One-Time Accounting Charges

In its latest Q1 earnings release, management implemented an extraordinarily rare and massive downward revision to its full-year 2026 EPS outlook:

- GAAP EPS: Revised to a loss of $3.25 to $2.85 (down from the initial projection of positive $6.75 to $7.15).

- Non-GAAP EPS: Revised to a loss of $1.05 to $0.65 (down from the initial projection of positive $8.45 to $8.85).

【Crucial Context】 This is an upfront “one-time charge,” not an operational collapse

This revision wiped approximately $9.50 off the projected EPS. The adjustment stems entirely from Gilead’s aggressive expansion in external M&A and collaborations during 2026—including the finalization of the 7.8B Arcellx acquisition, the Tubulis transaction, and the Ouro Medicines alliance. Under current accounting standards, a staggering 11.5B in In-Process Research and Development (IPR&D) upfront fees and related financing costs must be expensed entirely in 2026. This massive, forward-looking R&D investment completely masks the year’s underlying operational net income on paper.

2. Quarterly EPS Trend over the Next Four Quarters: Exceptionally Strong Core Profitability

When striping away the 11.5B one-time acquisition drag to look at the company’s true “core earnings power,” Gilead’s quarterly EPS is actually tracking near historical highs:

- Q1 Sets a High Bar: True Non-GAAP EPS for Q1 2026 landed at $2.03 (up 12.2% year-over-year), substantially beating Wall Street consensus estimates of $1.91.

- Baseline Margin Expansion: Thanks to the formal expiration of a long-standing TAF royalty payment obligation in Q1, coupled with an increased mix of higher-margin HIV revenue and Trodelvy, Gilead’s Non-GAAP product gross margin has undergone a structural transformation, climbing to a premium 87.5% (up 2 percentage points year-over-year).

- Trajectory for the Next Three Quarters: Over the remaining quarters of 2026 (Q2, Q3, and Q4), driven by the full-year scaling of YEztugo toward its 1B blockbuster target and continuous enrollment for Livdelzi, the illustrative base business is positioned to reliably generate roughly $2.00 to $2.20 in Non-GAAP EPS per quarter.

3. Fiscal Year 2027 Outlook: Primed for an Explosive EPS Breakout

Once the one-time accounting headwinds of 2026 are fully cleared from the balance sheet, the market and analysts anticipate a dramatic surge in Gilead’s reported financials moving into the following year:

- Full Financial Normalization: Absent the heavy IPR&D impairment charges, Non-GAAP EPS for fiscal year 2027 is projected to instantly gap up and return to a highly lucrative bracket of $8.50 to $9.00+.

- Seamless Transition to New Growth Engines: December 23, 2026, marks the critical FDA PDUFA action date for anito-cel, the highly anticipated CAR-T therapy for multiple myeloma. By 2027, this high-margin asset will officially transition into its commercial harvest phase. Alongside the continuous rollout of the every-six-month Lenacapavir injection for prevention, it will inject strong, fundamental earnings momentum directly into 2027 EPS.

Summary of the Next Year’s EPS Trajectory

Gilead’s EPS over the coming year will display a peculiar dichotomy of “reported net losses alongside cash-generating core operations.” In the short term (through fiscal year 2026), the annualized bottom line will read negative, but this is strictly the accounting price paid to secure full proprietary ownership of the company’s future blockbuster pipeline.

As the 87.5% high-margin baseline business continues to expand, the moment the company enters fiscal year 2027, EPS is set to stage a violent V-shaped reversal, snapping straight back onto a powerful trajectory of generating over $8 per share.

Wall Street consensus (including major firms like Wolfe Research and Barclays) generally maintains a “Strong Buy” or “Outperform” rating on Gilead. The core reasons to back this stock include:

- The Core HIV Franchise Provides an Unparalleled Cash Flow Moat: Biktarvy and the newly launched YES2GO (which is on track to cross the 1B sales threshold in its first year) demonstrate incredible commercial resilience. Crucially, Gilead’s HIV patent estate extends safely out to 2036, eliminating the near-term Loss of Exclusivity (LOE) or “patent cliff” risks that typically plague large-cap pharma peers.

- Structural Leap in Underlying Profitability: Propelled by the formal expiration of legacy TAF royalty obligations, Non-GAAP product gross margin soared to a premium 87.5% in Q1 (up 2 percentage points year-over-year). High gross margins mean that even as the company scales up R&D, its underlying capacity to generate Free Cash Flow (FCF) remains among the top tier in the industry.

- The Bad News is Out; Balance Sheet Cleared Upfront: The dramatic adjustment to full-year 2026 guidance, shifting EPS into a projected loss of $1.05 to $0.65, is strictly an accounting byproduct of taking a concentrated 11.5B upfront charge for massive strategic M&A (such as the Arcellx acquisition). Since this paper loss has already been completely digested by the market following the Q1 earnings call, the downside is fully priced in.

Potential Upside and Target Price Analysis

As of mid-May 2026, Gilead’s stock is consolidating in the $129 to $132 range.

- Wall Street Average Consensus Target Price: Approximately $158.00 to $161.46.

- Bull-Case Street Targets: Top-tier analysts are significantly more constructive, with firms like Wolfe Research setting a target at $170.00, and Scotiabank pushing their target to $177.00.

- Potential Upside Calculations (Based on a current stock price of roughly $130):

- To Consensus Target ($161): Implies a potential upside of approximately +23.8%.

- To Bull-Case Target ($170): Implies a potential upside of approximately +30.7%.

Furthermore, the company yields a stable ~2.5% dividend (paying out $0.82 quarterly) and boasts an 11-year track record of consecutive dividend increases, offering premium downside protection for income and value investors alike.

Key Catalysts Over the Next 12 Months (The Upside Drivers)

To bridge the gap to that 20%+ upside, the market is waiting on the execution of two pivotal inflection points:

- Regulatory Approvals for Lenacapavir (Every-Six-Month Injection): Having secured FDA Priority Review status in late April 2026, any positive regulatory updates or outright approvals later this year will act as a massive catalyst, radically resetting market expectations for Gilead’s long-term top-line expansion.

- The BLA Decision for anito-cel (December 23, 2026 PDUFA Date): Now that the Arcellx acquisition is closed, securing a year-end FDA green light for this highly disruptive CAR-T therapy in multiple myeloma will formally unlock Gilead’s second major growth curve in oncology.

Strategic Investment Advice

Gilead is currently sitting in deeply undervalued territory. For long-term investors looking for stable, anti-cyclical exposure that offers a combination of capital gains (as fiscal year 2027 EPS snaps back to a normalized $8.50+) and reliable dividend yields, the current price represents a highly compelling entry point to accumulate shares.

Source:

- https://investors.gilead.com/news-releases/news-release-details/gilead-sciences-announces-first-quarter-2026-financial-results

- https://www.nasdaq.com/market-activity/stocks/gild/earnings

- https://seekingalpha.com/symbol/GILD/earnings

Back to Gilead page