Deere & Company (John Deere, NYSE: DE) reported its Q1 FY2026 financial results on February 19, 2026, significantly beating Wall Street expectations. Management indicated that 2026 is expected to represent the cyclical trough for the industry, backed by a strong recovery in order banks.

Here is the summary of the key financial performance and outlook:

Core Financial Performance

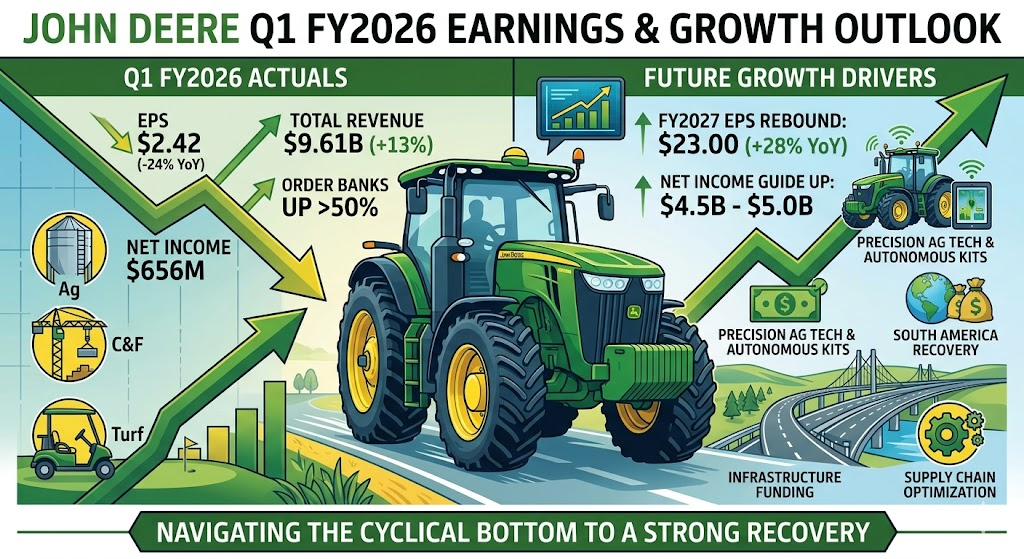

- Total Revenue & Net Sales: Reached 9.61B, up 13% year-over-year (YoY), surpassing the consensus estimate of 7.59B. Net sales for Equipment Operations were 8.001B, representing an 18% increase YoY.

- Net Income: Came in at 656M (or diluted EPS of $2.42), beating analyst estimates of $2.02. However, EPS declined from $3.19 in the same quarter last year, heavily impacted by higher production costs and increased warranty expenses.

- Operating Margin: Equipment Operations reported an operating margin of 5.9% for the quarter.

Segment Performance

Construction & Forestry

- Top Performer: Net sales surged 34% YoY to 2.67B.

- Operating Profit: More than doubled to 137M from 65M in the prior year’s quarter, driven by higher shipment volumes, favorable product mix, and positive foreign exchange effects.

Small Ag & Turf

- Steady Growth: Net sales grew 24% YoY to 2.17B.

- Operating Profit: Increased to 196M from 124M, supported by higher shipment volumes and a 2% price realization.

Production & Precision Ag

- Margin Pressure: Net sales edged up just 3% YoY to 3.16B.

- Operating Profit: Dropped sharply to 139M from 338M. Profitability was eroded by weak commodity prices and high interest rates in South America, requiring higher sales incentives, alongside headwinds from tariffs, unfavorable sales mix, and elevated warranty costs.

Guidance & Management Outlook

- Raised Full-Year Guidance: Upwardly revised FY2026 Net Income guidance to a range of 4.5B to 5B (up from the previous outlook of 4.0B to 4.75B). Equipment Operations full-year cash flow forecast was also lifted by 500M to a range of 4.5B to 5.5B.

- Cyclical Bottom Signaling: Management noted that order banks jumped over 50% during the quarter, hitting their highest level since May 2024. This reinforces the view that 2026 marks the bottom of the current industry downturn.

- Policy Support: The U.S. government’s farm aid programs, such as the roughly 12B farmer bridge assistance initiative, have provided essential liquidity to North American farmers, cushioning the downside for the large agricultural machinery market.

Deere & Company demonstrated several critical structural and market shifts during Q1 FY2026. These changes not only explain the significant earnings beat but also highlight the company’s strategic positioning moving forward:

1. Cyclical Bottoming and Order Surge

After several quarters of decline driven by high interest rates and lower crop prices, the most pivotal shift this quarter was the order bank surging over 50%. This marked the highest level of order backlog since May 2024. This turnaround gave management the confidence to officially declare 2026 as the cyclical trough of the current downturn, signaling an impending recovery.

2. Shift in Growth and Profitability Drivers

While large agricultural machinery historically anchor John Deere’s earnings, this quarter saw a stark divergence and rebalancing among business segments:

- Construction & Forestry as the Main Growth Engine: Driven by sustained infrastructure spending, this segment saw revenue surge 34% YoY, while operating profit more than doubled (up 110%), effectively offsetting weakness in the ag sector.

- Margin Compression in Precision Ag: Although Production & Precision Ag revenue managed a 3% increase, its operating profit plummeted over 58%. This reflects severe headwinds in South America (particularly Brazil), where high interest rates and depressed commodity prices forced Deere to offer aggressive sales incentives and discounts to stimulate demand.

3. Cost-Side Headwinds from Warranties and Tariffs

Despite the top-line beat, net income and EPS declined compared to the same period last year, heavily impacted by shifting internal and external cost pressures:

- Elevated Warranty Expenses: A significant rise in warranty claims and provisions during the quarter directly eroded gross margins, particularly within the ag segments.

- Tariff Pressures: Supply chain adjustments and tariff headwinds emerged as notable drags on profitability across both agricultural and construction equipment lines.

4. Government Aid Stabilizing North America

The implementation of U.S. government farm aid programs, such as the roughly 12B farmer bridge assistance initiative, began providing material support this quarter. This injection of liquidity bolstered North American farmers’ cash flows, serving as a critical buffer that prevented a steeper decline in large ag equipment demand.

5. Executive Transitions and Legal Resolutions

Beyond the financial metrics, Deere finalized two major corporate updates during and shortly after the quarter that shape its forward-looking outlook:

- New CFO Appointment: The company announced that Brent Norwood, a 20-year veteran at Deere who spearheaded landmark acquisitions like Wirtgen and Blue River Technology, will officially take over as Senior VP and CFO on May 1, 2026.

- Right to Repair Settlement: In early April 2026, Deere reached a comprehensive settlement regarding its long-running antitrust class-action lawsuit over repair rights. The company agreed to establish a settlement fund and committed to continued access to diagnostic software, tools, and manuals for independent repair shops, removing a major long-term legal risk.

Deere & Company will report its Q2 FY2026 financial results on May 21, 2026. Based on management’s forward-looking guidance and current industry trends, the company’s growth catalysts and key execution indicators for the upcoming quarters are concentrated in the following areas:

1. Margin Recovery in Production & Precision Ag

Although low crop prices are expected to drive down large agricultural equipment shipments by 15% to 20% for the full year, management noted that the worst of the quarterly margin erosion is now behind them.

- While the segment’s operating margin plummeted to 4.4% in Q1 due to aggressive promotional incentives in South America, full-year margin guidance remains anchored at 11% to 13%.

- This implies a sharp sequential margin rebound starting in Q2, as the core North American market enters the spring planting season and peak delivery window, lifting the sales mix toward higher-margin large tractors (8R/9R series) and X9 combines.

2. Tech Transformation and Automation Kit Commercialization

Deere’s structural growth engine is shifting from traditional hardware manufacturing to chip-and-satellite-driven recurring tech subscriptions and retrofit upgrades:

- See & Spray Acceleration: Adoption take rates on new combines have crossed the 90% threshold, alongside double-digit YoY growth in active usage from existing operators.

- Autonomous Tillage Kits: Autonomous retrofit kits designed for spring 2026 delivery have entered full commercial production. This introduces high-margin software revenues, supporting the company’s target of achieving a standalone 10% operating margin for its precision ag software business by the end of 2026.

3. Sustained Expansion in Construction & Forestry (C&F)

While agriculture works through its cyclical trough, the C&F segment acts as a vital counter-cyclical growth lever.

- Earthmoving and roadbuilding equipment backlog remains robust, driven by the ongoing deployment of federal infrastructure funding and fleet replenishment cycles from major equipment rental companies.

- Management significantly upgraded the full-year net sales guidance for C&F to a 15% increase (up from the previous 5% estimate), with full-year operating margins revised upward to a 9% to 11% range, making it the most reliable near-term earnings engine.

4. Inventory Restocking in Small Ag & Turf

- Following aggressive, deliberate production cuts throughout 2025, dealer channel inventories have been leaned out to healthy, below-average levels.

- Supported by improving profitability in the dairy and livestock sectors, alongside steady commercial landscaping and turf care demand, management lifted the segment’s full-year revenue guidance to a 15% increase (up from previous flat-to-5% guidance), positioning it for an acceleration in shipments starting in Q2.

5. Price Realization Countering Tariff and Cost Headwinds

Deere anticipates up to 1.2B in potential headwinds related to raw material costs and global tariff adjustments for FY2026. Growth over the next few quarters will rely on the successful execution of price hikes to defend profitability:

- The company expects to realize a 1.5% price increase in Production & Precision Ag and a 2.5% increase in Construction & Forestry.

- If supply chain efficiencies hold steady alongside these pricing dynamics, a more pronounced operating leverage effect will materialize in the second half of the fiscal year.

Based on Deere & Company’s updated full-year guidance and the consensus models from Wall Street, the company’s Earnings Per Share (EPS) over the next 12 months is projected to follow a “near-term bottoming with margin repair, leading to a sharp cyclical recovery in FY2027” trajectory.

Here is the core breakdown of the EPS outlook and the key variables driving the numbers:

1. FY2026 EPS Outlook: The Cyclical Trough and Margin Inflection

For the full fiscal year 2026, Wall Street consensus estimates place Deere’s EPS at approximately $18.01, representing a mild 2.7% decline compared to $18.50 in FY2025. This reflects a resilient performance considering 2026 is officially pegged as the absolute bottom of the current agricultural machinery downturn.

- Upward Guidance Revision: Following the strong Q1 beat, management raised its full-year net income guidance from the previous 4.0B–4.75B range up to 4.5B–5.0B.

- Quarterly EPS Cadence:

- Q1 (Actual): Reported at $2.42, soundly beating the consensus estimate of $1.90, though lower than the $3.19 recorded in the prior year’s quarter due to upfront warranty costs.

- Q2 (Upcoming on May 21, 2026): Consensus estimates pin Q2 EPS between $5.70 and $5.81 (down from $6.64 in Q2 FY2025). While this represents a ~12.5% decline YoY, it shows massive sequential (quarter-over-quarter) acceleration as the North American market enters peak spring planting and equipment delivery season.

2. FY2027 EPS Outlook: Rapid Earnings Power Expansion

Looking further into fiscal year 2027, analysts expect Deere to unleash significant operating leverage as farm equipment fleet replacement cycles restart and recurring technology revenue scales.

- Growth Rebound: Consensus estimates forecast FY2027 EPS to surge from around $18.01 up to $23.00, representing an impressive 27.7% YoY growth rate. This underscores the market’s view that current headwinds are purely cyclical rather than structural.

3. Major Headwinds and Tailwinds Shaping the EPS Trajectory

Headwinds Depressing Near-Term EPS Potential

- 1.2B Tariff and Production Drag: Management confirmed that Deere will absorb approximately 1.2B in pretax tariff and geopolitical supply chain costs over FY2026. This is the primary catalyst capping gross margin expansion and EPS upside this year.

- South American Promotional Discounts: High interest rates and low soft commodity prices in Brazil have forced Deere to utilize aggressive dealer incentives and retail financing subsidies, eroding localized average selling prices (ASPs).

Tailwinds Accelerating EPS Performance

- Severe Segment Margin Sequential Recovery: Production & Precision Ag (PPA) operating margins troughed at 4.4% in Q1 due to South American headwinds. However, with full-year PPA margin guidance anchored firmly at 11%–13%, earnings power is set to step up drastically over the next three quarters.

- High-Margin Autonomous Rollout: Starting in spring 2026, See & Spray commercial adoption and autonomous tillage retrofit kits enter full-scale production. These silicon- and software-driven retrofits command significantly higher gross margins than traditional mechanical steel, setting the stage for structural EPS expansion into late 2026 and FY2027.

- Construction & Forestry (C&F) Counter-Cyclical Support: Boosted by federal infrastructure spending and AI data center construction, the full-year net sales guidance for C&F was up-revised to a 15% increase. This provides an excellent defensive earnings cushion during the bottom of the agricultural cycle.

Here is a detailed breakdown of the institutional consensus, implied upside, and core investment thesis:

1. Valuation and Potential Upside

Deere is currently trading around the $574 mark (as of mid-May 2026).

- Wall Street Consensus Target Price: Ranging between $655 and $687 (based on updated April/May institutional reports from Simply Wall St and MarketBeat).

- Implied Upside: Approximately 14% to 19.5%.

- Bull Case Targets: Top-tier firms like DA Davidson, UBS, and Morgan Stanley have set targets between $730 and $775.

- Optimistic Scenario Upside: Reaching 27% to 35%.

- Long-Term Fair Value: Advanced multi-year discounted cash flow models (such as the TIKR Advanced Valuation Model) indicate that once the structural operating leverage of the 2027 agricultural rebound and high-margin autonomous retrofit kits is fully factored in, the stock’s long-term fair value sits closer to $875.

2. Core Investment Thesis (Why Buy?)

Cyclical Bottom is Clearly Defined

Management has officially declared FY2026 as the absolute trough of the current downturn. Historical data demonstrates that buying the dominant market-share leader at the absolute bottom of a cycle delivers a highly asymmetric, winning risk-reward ratio. Wall Street forecasts EPS to bottom at $18.01 this year before surging 27.7% to $23.00 in FY2027.

Balanced Portfolio Hedging Ag Weakness

While large agricultural machinery volume is expected to decline 15% to 20% this fiscal year, the Construction & Forestry (C&F) segment is experiencing explosive growth (full-year revenue guidance upgraded to +15% YoY). This segment is capitalizing on the continuous deployment of U.S. Infrastructure Act funds and massive earthmoving equipment demand driven by AI data center construction.

Software Shift Raising the Valuation Multiple

Deere is no longer just a heavy machinery business. The accelerated commercialization of its “See & Spray” intelligent systems and autonomous tillage kits introduces high-margin, sticky, recurring software subscriptions. This silicon-and-software evolution is structurally reshaping Deere’s earnings profile, laying the groundwork for P/E multiple expansion.

Elite Downside Protection

Deere boasts a stellar track record of paying uninterrupted dividends for over 50 consecutive years (current annualized payout at $6.48). Supported by a robust cash-generating engine and multi-billion-dollar active share buyback programs, the stock has an excellent defensive floor.

3. Key Risks to Monitor (Why Not a Strong Buy?)

- 1.2B Tariff and Warranty Drag: Management confirmed that Deere will absorb up to $1.2B in pretax tariff and supply chain friction costs during FY2026, which caps short-term gross margin expansion.

- Depressed South American Dynamic: Severe macroeconomic pressure and high interest rates in Brazil continue to demand aggressive retail financing subsidies and promotional discounting from Deere, weighing down localized average selling prices (ASPs).

4. Strategic Investment Recommendation

Deere will report its Q2 FY2026 earnings on May 21, 2026. While YoY numbers will show a contraction, the massive sequential acceleration from Q1 will be the real focus.

- The Verdict: If you are a short-term momentum trader hunting for high-flying AI stocks, Deere is not the ideal vehicle. However, if you are a patient, medium-to-long-term value investor, current levels offer a prime window to steadily accumulate shares during an industry bottom. As global agriculture demand normalizes and tech kit deployment scales into FY2027, the projected 15% to 20% upside remains highly achievable.

Source:

- https://www.investing.com/news/transcripts/earnings-call-transcript-deere–company-q1-2026-sees-strong-earnings-beat-93CH-4514410

- https://www.investing.com/news/company-news/deere-q1-2026-slides-strong-revenue-growth-despite-profit-headwinds-93CH-4514444

- https://seekingalpha.com/article/4872244-deere-and-company-de-q1-2026-earnings-call-transcript

- https://seekingalpha.com/news/4554122-deere-soars-to-all-time-high-after-beat-and-raise-q1-report-sees-2026-as-ag-cycle-bottom

- https://farmpolicynews.illinois.edu/2026/04/deere-settles-class-action-right-to-repair-lawsuit/

- https://www.farmprogress.com/farming-equipment/john-deere-settles-right-to-repair-lawsuit-for-99-million

- https://www.streetinsider.com/Management+Changes/Deere+names+Brent+Norwood+as+chief+financial+officer/26411438.html

- https://simplywall.st/stocks/us/capital-goods/nyse-de/deere/news/what-deere-des-cfo-transition-to-t-brent-norwood-means-for-s

Back to Deere page