The following is the summary of Danaher’s (DHR) Q1 2026 earnings report:

Financial Highlights

- Revenue: $6.0B, an increase of 3.5% year-over-year.

- Earnings Per Share (EPS): GAAP EPS was $1.45; adjusted EPS was $2.06, reflecting a 9.5% year-over-year growth.

- Cash Flow: Operating cash flow was $1.3B, with free cash flow reaching $1.1B.

Key Business and Market Developments

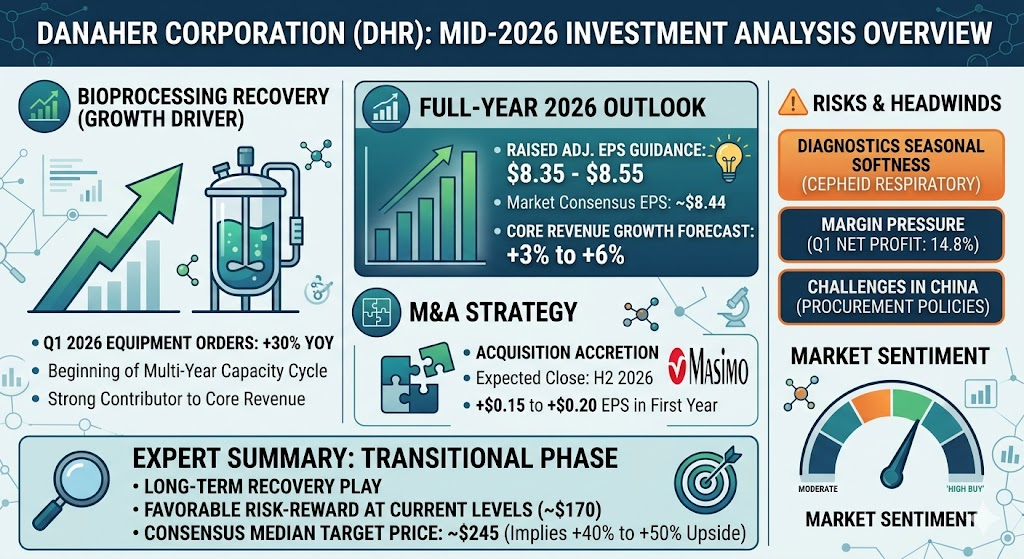

- Bioprocessing Recovery: The Biotechnology segment saw core sales growth of approximately 7%, which management identified as the beginning of a multi-year capacity investment cycle.

- Respiratory Headwinds: Due to seasonal respiratory trends, Cepheid’s respiratory-related revenue declined by approximately 25%, negatively impacting core revenue by about 2.5%.

- Strategic Acquisitions: The company announced its intent to acquire Masimo Corporation, aiming to leverage the Danaher Business System (DBS) and its global scale to improve the profitability of the asset.

- China Market Performance: Strong performance in Biotechnology and Life Sciences outperformed expectations, offsetting a low-single-digit decline in the Diagnostics segment caused by centralized procurement and changes in reimbursement policies.

Financial Outlook

- Raised Guidance: The company increased its full-year adjusted EPS guidance to a range of $8.35 to $8.55.

- Full-Year Outlook: Danaher maintained its forecast for full-year core revenue growth of 3% to 6%.

For the upcoming quarter (Q2 2026), Danaher’s growth momentum is primarily driven by the recovery in bioprocessing and stable improvements in end markets across its business segments. Here is a summary of the key drivers:

Core Growth Drivers

- Continued Bioprocessing Recovery: This remains Danaher’s strongest growth engine. In Q1, equipment orders recorded their first year-over-year increase in nearly two years (growing over 30%). This indicates that the industry’s capacity investment cycle has begun, which is expected to continue supporting core revenue in subsequent quarters.

- Improved Life Sciences End Markets: Beyond robust monoclonal antibody production demand from biopharmaceutical customers, R&D spending is showing signs of gradual improvement. Management noted that order activity from small biotech companies and academic research departments has stabilized and is showing signs of recovery.

- Diagnostics Business Resilience: Although Q1 was negatively impacted by seasonal respiratory factors (Cepheid), the broader diagnostics business demonstrated solid foundations when excluding these items. As seasonal headwinds related to respiratory products fade throughout the year, momentum in this segment is expected to pick up.

Financial Outlook and Guidance

- Q2 Forecast: The company expects core revenue for the second quarter to show low-single-digit growth year-over-year, with an expected adjusted operating profit margin of approximately 26.5%.

- Full-Year Growth: Danaher has maintained its forecast for full-year core revenue growth of 3% to 6% and slightly raised its full-year adjusted EPS guidance to a range of $8.35 to $8.55.

Strategic Perspective

Management emphasized that Danaher is utilizing the Danaher Business System (DBS) to strengthen operational profitability. Furthermore, as the acquisition of Masimo Corporation progresses, the company plans to leverage its global scale to capture operational synergies. While global macroeconomic environments (such as geopolitical tensions) remain a dynamic challenge, the company is maintaining profit stability through rigorous supply chain management and volatility monitoring.

The trajectory of Danaher’s (DHR) earnings per share (EPS) over the coming year is supported by internal growth strategies, the recovery in bioprocessing markets, and the anticipated impact of strategic acquisitions. Here is a key analysis:

EPS Outlook Summary

- 2026 Full-Year Guidance: Following the Q1 earnings report, the company raised its full-year adjusted EPS guidance to a range of $8.35 to $8.55.

- Market Consensus: Analyst estimates for full-year 2026 EPS currently hover around a median of $8.44.

- 2027 Growth Expectation: Market projections suggest that Danaher’s EPS could further increase to approximately $9.11 in 2027, representing a year-over-year growth rate of roughly 8%.

Key Factors Influencing EPS Trajectory

- Bioprocessing Recovery: This is the core driver of profit improvement. With equipment orders showing strong growth in Q1, these are expected to translate into more significant revenue and profit contributions over the coming quarters.

- Acquisition Impact (Masimo): Danaher has announced its intent to acquire Masimo Corporation. This acquisition is expected to close in the second half of 2026 and is projected to be accretive to EPS by $0.15 to $0.20 in the first full year. Long-term (after the fifth year), it is expected to contribute approximately $0.70 in EPS accretion.

- Execution of the Danaher Business System (DBS): The company continues to leverage DBS to improve operating margins. Even in a volatile market, Danaher has maintained better-than-expected earnings, credited to its robust cost control and productivity enhancement initiatives.

- Market Headwinds: While the biotechnology segment is recovering, the diagnostics segment—particularly Cepheid’s respiratory business—remains subject to seasonal volatility, which is a factor that may limit explosive profit growth in the short term.

Financial Health Indicators

- Strong Cash Flow: The company maintains robust free cash flow generation (1.1B in Q1), providing high flexibility for capital allocation, including consistent dividend payouts and strategic acquisitions.

- Valuation: Market sentiment remains generally positive, with a consensus “Buy” rating. Current share prices reflect growth expectations, and the median analyst price target is approximately $245, reflecting market confidence in the company’s long-term earning power.

In summary, Danaher’s EPS trajectory is on a steady upward trend, driven in the short term by business recovery and in the medium-to-long term by the accretion from strategic acquisitions.

Upside Potential

Market sentiment among analysts remains largely bullish, characterizing DHR as a high-quality asset currently trading at a discount.

- Target Price Range: Analyst consensus indicates a median price target of approximately $245, which, relative to the recent price level near $165–$170, implies an upside potential of roughly 40% to 50%.

- Valuation Gap: Discounted Cash Flow (DCF) models frequently place the intrinsic value of DHR in the $215–$230 range, suggesting the stock is currently undervalued by nearly 20% to 30% compared to its projected long-term cash flow generation.

- Core Catalysts:

- Bioprocessing Recovery: Q1 2026 equipment orders saw their first year-over-year increase in nearly two years (up over 30%), signaling the start of a multi-year capacity investment cycle.

- Strategic M&A: The pending acquisition of Masimo Corporation is expected to close in the second half of 2026, serving as a long-term lever for margin expansion and portfolio diversification beyond seasonal respiratory diagnostics.

Downside Risks

Despite the attractive valuation, the stock faces significant short-term pressure:

- Operational Headwinds: The diagnostics segment, specifically Cepheid’s respiratory business, has struggled with seasonal softness and pricing pressure in China.

- Valuation Sensitivity: While its P/E ratio is lower than many historical peaks, the market is cautious about the recent decline in net profit margins (easing from 15.8% to 14.8%), which creates tension between current stock price and future growth expectations.

- Macro and Execution Risk: Broader market volatility and the integration risks associated with the $9.9 billion Masimo acquisition may act as near-term “noise” that could limit rapid price appreciation.

Expert Summary

Danaher is currently in a transitional phase. It is arguably a “buy” for long-term investors attracted to its recurring revenue model and the leverage provided by the Danaher Business System (DBS).

- The Bull Case: The company is a fundamental “life sciences & diagnostics” play. If the 30% growth in bioprocessing orders continues, it will validate the recovery thesis and likely drive the stock toward its intrinsic value.

- The Bear Case: Skeptics point to the gap between revenue growth (forecast at 3–6%) and the higher earnings growth targets, arguing that Danaher must demonstrate significant efficiency gains to justify its current premium.

Recommendation: Monitor the conversion of bioprocessing orders into revenue over the next two quarters. This is the primary indicator of whether the company’s turnaround is firmly on track. If the recovery holds, the current price point represents a favorable risk-reward entry for a long-term holding.

Disclaimer: This analysis is for informational purposes only and does not constitute formal investment advice. Investment decisions should be based on your individual risk tolerance and overall portfolio strategy.

Source:

- https://statementdog.com/analysis/DHR

- https://www.tradingview.com/news/tradingview:d69898b059a00:0-danaher-posts-q1-2026-revenue-6-0b-net-income-1-03b-adj-diluted-eps-2-06/

- https://investors.danaher.com/press-releases

- https://investors.danaher.com/2026-04-21-Danaher-Reports-First-Quarter-2026-Results

- https://seekingalpha.com/news/4577241-danaher-signals-2026-adjusted-eps-of-8_35-8_55-while-keeping-3-percentminus-6-percent-core

- https://simplywall.st/stocks/us/pharmaceuticals-biotech/nyse-dhr/danaher/future

- https://www.marketbeat.com/stocks/NYSE/DHR/earnings/

Back to Danaher page