The financial report for Contemporary Amperex Technology Co., Limited (CATL, 300750.SZ) for the first quarter of 2026 demonstrates significant resilience amidst market volatility. Key changes are concentrated in product mix adjustments, overseas expansion progress, and the impact of non-recurring items:

1. Product Structure and Gross Margin Shifts

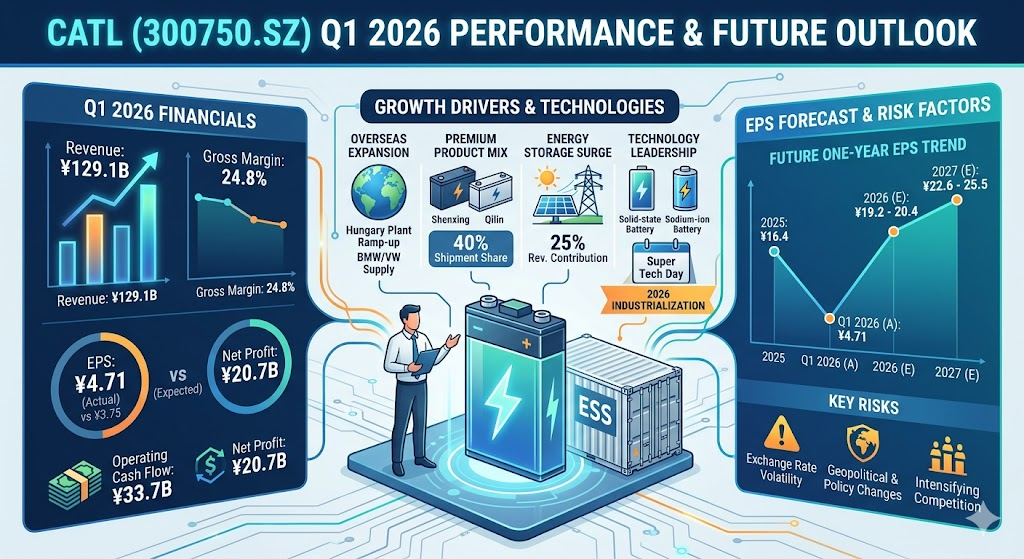

- Significant Growth in Energy Storage: Total battery sales exceeded 200GWh this quarter, with energy storage batteries increasing to approximately 25% (over 50GWh). Since energy storage batteries generally command higher gross margins (approx. 26.71%) compared to power batteries (approx. 23.84%), the surge in this segment has become a major profit engine.

- Slight Quarter-on-Quarter Margin Decline: The consolidated gross margin was 24.82%, a slight decrease from Q4 2025. This was primarily due to the lagged pass-through of rising raw material costs (such as commodities and lithium carbonate) and shifts in Average Selling Price (ASP) driven by higher domestic energy storage shipments.

2. Overseas Capacity and New Design Wins

- Deepening European Presence: The Hungary plant has entered the equipment commissioning phase and begun supplying BMW. Costs at this facility are expected to be roughly 20% lower than the German base, which will significantly optimize the profitability of overseas operations as production scales up.

- Global Market Position: CATL’s global market share in power batteries remains near 40%, securing the top spot for nine consecutive years. The company has revised its 2026 full-year production plan upward to between 1.1 and 1.2TWh.

3. Financial Metrics and Non-recurring Factors

- Impact of Exchange Losses: Driven by the appreciation of the RMB, the company recorded exchange losses exceeding 1.7B, which weighed on net profit performance.

- Robust Cash Flow: Net cash flow from operating activities reached 33.7B, indicating strong bargaining power with downstream customers and supply chain partners, as well as efficient capital recovery during capacity expansion.

- Doubling of Investment Income: Investment income for Q1 was approximately 2.7B, a 101% year-on-year increase, mainly benefiting from changes in the fair value or dividends of invested companies across the industry chain.

4. Strategy and Policy Response

- Export Tax Rebates: Regarding the reduction in export tax rebate rates effective April 1, the company stated the overall impact on profit is limited, as it offsets cost pressures through localized production at overseas plants and optimized production line efficiency.

- Future Technology Roadmap: The company designated the Super Tech Day on April 21 as a turning point to accelerate the mass production of solid-state and sodium-ion batteries, addressing low-price competition from second-tier manufacturers.

Based on the performance in Q1 2026 and the latest market developments, the growth momentum for CATL in the upcoming quarter (Q2 2026) is primarily driven by the following four core engines:

1. Ramp-up of Overseas Capacity (Hungary Plant)

- Mass Production in Hungary: The Debrecen plant (Phase I with a 40GWh capacity) commenced production in early 2026 and is expected to enter a critical capacity ramp-up phase in Q2. This facility directly serves core European clients such as BMW, Stellantis, and VW. Localized production will significantly reduce logistics costs and mitigate potential risks related to trade tariffs.

2. Increased Penetration of Shenxing and Qilin Batteries

- Premium Product Mix: The shipment share of Shenxing Superfast Charging batteries (LFP) and Qilin batteries (NCM) is projected to reach over 40% in 2026. As more vehicle models equipped with 4C fast-charging technology launch in the second quarter, the volume growth of these high-margin products will effectively offset price war pressures in the entry-level market.

- Shenxing Plus Series: The newly released Shenxing Plus series further improves energy density and range (up to 1000km), and is expected to become a mainstream configuration for luxury and long-range models in Q2.

3. Sustained Surge in Energy Storage Business

- Expansion of Zero-Carbon Business: Benefiting from global demand for grid-scale and industrial/commercial energy storage, the revenue contribution from this segment is expected to break past 25%. Since energy storage projects often follow seasonal delivery patterns and offer better margins than power batteries, order settlements in Q2 will be a key support for profit growth.

4. Industrialization Turning Point for Frontier Technologies

- Solid-State and Sodium-Ion Batteries: CATL has designated 2026 as the inaugural year for the industrialization of solid-state batteries. Following the production updates shared during the Super Tech Day in late April, Q2 is expected to see more data regarding the installation of second-generation sodium-ion batteries in commercial and compact vehicles.

- R&D Capital Infusion: The company recently completed a major H-share placement in Hong Kong, raising approximately 39.11B HKD. These funds will be deployed rapidly in Q2 toward zero-carbon business initiatives and the R&D of frontier battery technologies to strengthen its technological lead.

Comprehensive Outlook

Analysts generally believe that despite raw material price fluctuations, CATL’s revenue is poised for steady quarter-on-quarter growth in Q2, driven by its domestic market share of over 50% and accelerating overseas expansion. Furthermore, as capacity utilization rates recover, unit production costs are expected to decline further.

According to the latest research reports and market consensus from institutions such as Sinolink Securities, East Money, and Simply Wall St, the earnings per share (EPS) for CATL (300750.SZ) is expected to maintain a steady growth trend over the coming year. Here is the detailed analysis of the trend and forecast data:

1. EPS Forecast Trends

Based on consensus expectations, the actual EPS for 2025 was 16.41, representing a year-on-year growth of 42.28%.

Entering 2026, the market projects the full-year EPS to fall between 19.16 and 20.39, an increase of approximately 16.7% to 24.3%. Notably, the actual EPS for the first quarter of 2026 reached 4.71, outperforming the initial market expectations of 3.69 to 3.80, providing a strong foundation for the annual target.

Looking ahead to 2027, analysts predict that EPS will further grow to between 22.59 and 25.49, reflecting a continuous expansion of long-term profitability.

2. Core Drivers for EPS Strength

Recovery in Capacity Utilization and Economies of Scale: As the global electric vehicle demand enters a new growth cycle in 2026, CATL’s capacity utilization is expected to rise from around 70% in 2025 to over 80%. This will significantly dilute fixed costs, thereby improving unit margins and overall earnings efficiency.

Release of High-Margin Overseas Orders: The capacity ramp-up of the Hungary plant (Phase I) in 2026 will contribute more to international revenue. Since the Average Selling Price (ASP) and profit margins for European orders are generally higher than those in the domestic market, this will directly drive structural growth in EPS.

Premium from New Technologies: The increasing shipment share of high-value products such as Shenxing and Qilin batteries (expected to exceed 40% in 2026) helps the company maintain gross margins above 20%, even amidst intense domestic price wars.

Cash Flow and Interest Income: The company maintains extremely abundant cash flow, with operating cash flow reaching 33.7B in Q1 2026. Additionally, the recent H-share placement in Hong Kong raised approximately 39.11B HKD. A robust balance sheet not only supports R&D but also generates stable financial returns and interest income.

3. Potential Risk Factors

Exchange Rate Volatility: As the proportion of overseas revenue continues to increase, fluctuations in the RMB exchange rate have a growing impact on net profit and EPS. For instance, exchange losses of approximately 1.7B were recorded in Q1 2026.

Geopolitical and Policy Changes: Dynamics regarding the U.S. Inflation Reduction Act (IRA) and EU tariff policies on Chinese EVs remain uncertainties that could affect the pace of expansion and profitability in overseas markets.

Intensifying Industry Competition: If second-tier battery manufacturers launch more aggressive price wars, CATL might be forced to adjust its pricing strategy to maintain market share, which could impact short-term EPS performance.

In summary, most analysts believe CATL is transitioning from a period of high-speed growth to a phase of stable growth and technological leadership. The market currently assigns a forward P/E ratio for 2026 between 20x and 22x, which is at a historically low level. Sustained EPS growth will be the core driver supporting the upward movement of the stock price.

Source:

- https://finance.eastmoney.com/a/202604153706284270.html

- https://wap.eastmoney.com/report/AP202604261821592998.html

- https://pdf.dfcfw.com/pdf/H3_AP202604161821255081_1.pdf

- https://www.moomoo.com/news/post/68349811/catl-s-q1-revenue-hit-a-record-high-with-a

- https://www.investing.com/news/stock-market-news/catl-shares-hit-record-high-after-strong-q1-earnings-4617032

- https://www.catl.com/news/7945.html

- https://www.tradingview.com/symbols/SZSE-300750/forecast/

- https://stock.stockstar.com/notice/SN2026041500042193.shtml

Back to CATL page