The development history of Cambricon can be divided into the following three key phases:

1. Academic Incubation and Technical Foundation (2016-2017)

Founded by a team from the Institute of Computing Technology (ICT) of the Chinese Academy of Sciences, Cambricon’s core team has long specialized in neural processing unit (NPU) architecture research. During this phase, the company focused on underlying architectural innovation and launched the Cambricon 1A, the world’s first commercial deep learning processor. This successfully integrated AI acceleration capabilities into end-user devices, establishing its position as a technical pioneer in the field of neural processing.

2. Product Line Expansion and Ecosystem Building (2018-2020)

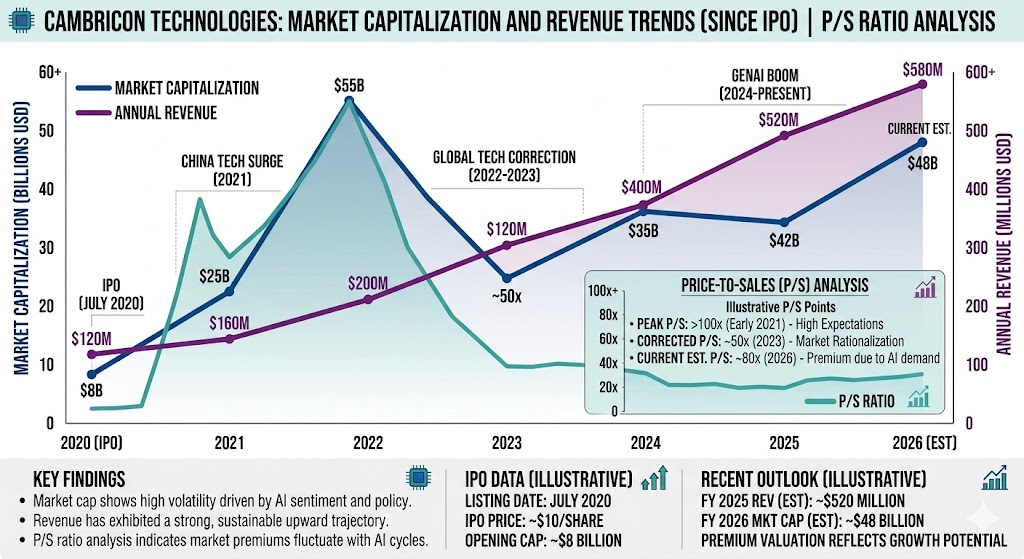

The company moved toward product diversification, expanding its business from edge devices to the cloud. It successively released the MLU series of cloud-based AI chips and the associated software development platform, Cambricon NeuWare. During this period, the company committed to building an integrated software-hardware development environment to serve high-performance computing needs such as data centers. In 2020, Cambricon successfully went public on the STAR Market of the Shanghai Stock Exchange, significantly strengthening its capital position.

3. Global Strategy and Deepening Computing Power (2021-Present)

With the advent of the era of large models, Cambricon has focused on the research and development of high-performance computing power. By iteratively launching the MLU370, MLU590, and subsequent series, it has significantly enhanced support for the training and inference of Large Language Models (LLMs). During this phase, the company has emphasized the continuous optimization of its software-hardware ecosystem and has actively strengthened its competitiveness in the general-purpose AI processor market, striving to become a core supplier of computing power for global AI infrastructure.

In 2026, the competitive landscape for Cambricon is divided between international and domestic Chinese markets, with its core competitiveness lying in its role as a key driver of domestic, localized AI hardware alternatives.

1. International Competitive Landscape

- Technical Gap: Despite rapid growth in the domestic market, Cambricon still faces the overwhelming technical monopoly of NVIDIA in the global AI chip sector. Leveraging its CUDA ecosystem and advanced Blackwell architecture, NVIDIA currently holds over 80% of the global AI accelerator market.

- Market Squeeze: Due to US export restrictions on high-end AI chips, NVIDIA’s market share in China continues to decline (expected to drop below 60%), leaving a massive market vacuum for domestic manufacturers like Cambricon.

2. Domestic Chinese Competition (The Core Battlefield)

Cambricon currently sits in the first tier of Chinese AI chipmakers, but it still faces intense competition within the domestic market:

- Huawei (Ascend): Huawei is Cambricon’s largest competitor in China. Through its Ascend 910/920 series, Huawei has built a powerful cloud ecosystem and possesses superior system integration capabilities. Huawei is projected to reach an output of 600K units in 2026, continuing to lead among domestic suppliers.

- Other Domestic Competitors: Companies such as Hygon Information (focusing on its DCU series), Moore Threads, Iluvatar CoreX, and Enflame are competing for market share by leveraging Chiplet technology, High Bandwidth Memory (HBM), and software development platforms (e.g., Hygon’s DCU-paired computing ecosystem).

3. Cambricon’s Competitive Strategy and Advantages

- Computing Power and Ecosystem Integration: With its MLU product series, Cambricon has secured key deployments among large-scale clients such as ByteDance. Its advantage lies in its deeply integrated software-hardware development platform (NeuWare), which helps reduce switching costs for customers.

- Policy Dividends: Cambricon is among the very few companies selected for Chinese government AI hardware procurement lists, providing it with an exclusionary advantage in national-level data center and smart city projects.

- Expansion Targets: In 2026, Cambricon plans to increase production to 500K units, with the goal of capturing market share from Huawei and filling the void left by NVIDIA due to trade restrictions.

4. Key Risks and Challenges

- Capacity Dependency: Cambricon is highly dependent on the advanced process capacity of Semiconductor Manufacturing International Corporation (SMIC). While the two have a strategic partnership, the yields (approx. 20%) and capacity constraints of advanced processes (e.g., 7nm-class nodes) remain the primary factors limiting the achievement of its shipment targets.

- Customer Concentration: Cambricon’s revenue is heavily reliant on its top few clients (such as ByteDance). A change in the procurement strategy of any single major client would have a significant impact on the company’s revenue.

Source:

- https://www.tomshardware.com/tech-industry/cambricon-q1-2026-earnings-as-chinas-domestic-ai-chip-market-accelerates

- https://simplywall.st/stocks/tw/tech/twse-2360/chroma-ate-shares/news/asian-growth-companies-with-insider-ownership-in-may-2026

- https://en.unibetter-ic.com/16-top-ai-chip-makers-in-2026/

Back to Cambricon page