According to the latest public information, BYD released its financial report for the first quarter of 2026 at the end of April, with performance falling short of market expectations. Below is a summary of the quarterly financial report:

Q1 2026 Financial Report Key Data Summary

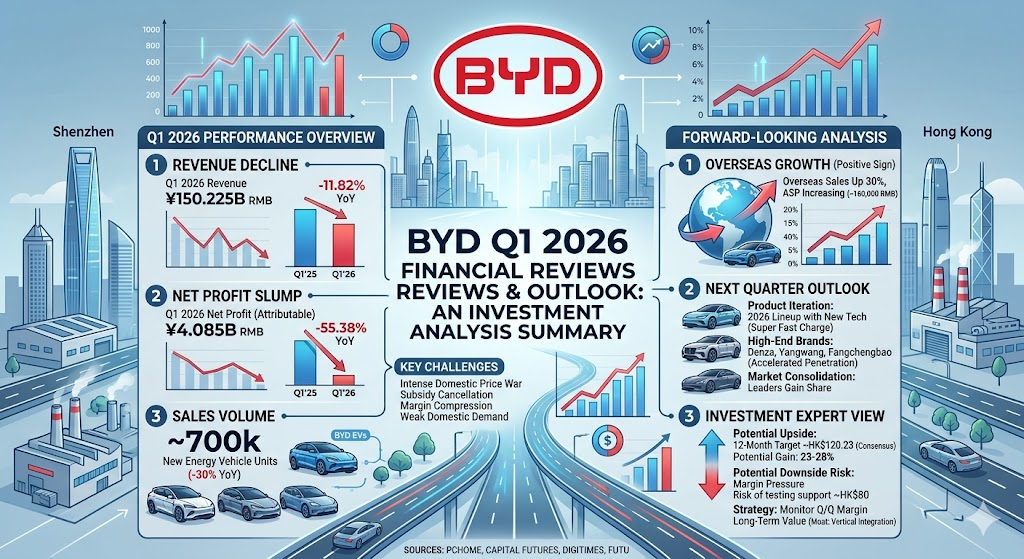

- Revenue and Sales Volume: Facing intense price competition in the Chinese market and the cancellation of government subsidy policies, BYD’s new energy vehicle sales in the first quarter were approximately 700,000 units, a decline of about 30% compared to the same period last year.

- Profit Performance: Overall net profit was weak, with a decline of over 55% compared to the previous year.

- Market Background: Although BYD surpassed Tesla as the global electric vehicle sales champion in 2025, the company has faced significant pressure on both revenue and profitability in early 2026 due to changes in the market environment and intensifying competition.

The financial status of BYD for the first quarter of 2026, future outlook, and EPS analysis are summarized below:

Key Changes and Operational Highlights for Q1

- Significant Profit Decline: Net profit attributable to shareholders was 4.085B RMB, a year-over-year decrease of 55.38%. The primary reason was the intense price war in the Chinese electric vehicle market, which compressed per-unit margins, coupled with reduced economies of scale.

- Revenue Decline: Q1 revenue was 150.225B RMB, down 11.82% year-over-year.

- Strong Overseas Market: Despite pressure on domestic demand, overseas sales performance was robust. The share of overseas sales increased significantly, driving the overall average selling price (ASP) up (to approximately 160,000 RMB) compared to both the previous quarter and the same period last year.

- Cost and Expense Pressure: Affected by exchange rate fluctuations and declining scale, the period expense ratio rose; however, driven by the optimization of the overseas sales mix, the gross margin for the automotive business improved compared to the previous quarter.

Next Quarter Outlook

- Product Iteration: BYD is gradually rolling out its 2026 vehicle lineup. The introduction of new technologies (such as super-fast charging) is expected to enhance product competitiveness and help boost domestic sales momentum.

- High-End Strategy: The company continues to promote its sub-brands such as Denza, Yangwang, and Fangchengbao to accelerate penetration into the high-end market.

- Market Landscape: The Chinese electric vehicle industry has entered a consolidation phase, and weaker brands may exit the market sequentially. Market share is expected to concentrate among top-tier enterprises. Analysts generally expect that as the sales mix improves and the scale of the overseas market expands, profitability will gradually recover in subsequent quarters.

One-Year EPS Forecast

Since consensus EPS forecasts for individual stocks in the public market are dynamic and easily influenced by market sentiment, investors should note the following trends:

- Market Consensus: Despite the weak profit performance in the first quarter, some brokerage research reports still maintain a buy rating on BYD’s long-term competitiveness.

- Risk Factors: Continuous monitoring is required regarding whether domestic market demand will rebound as expected and whether the decline in battery costs meets projections.

- Note: Please be aware that EPS forecasts for BYD on the market are subject to frequent changes. It is recommended to refer to real-time consensus forecasts provided by major investment banks (such as Citi) or professional financial information platforms (such as Bloomberg, Investing.com) to obtain values most reflective of the current market assessment.

1. Potential Stock Price Upside and Downside

Market sentiment toward BYD currently reflects a divergence of “bearish in the short term, bullish in the long term”:

- Potential Upside:

- Analyst Price Targets: Based on data as of the end of May 2026, the average 12-month target price for BYD (01211.HK / 002594.SZ) among institutional analysts is approximately 120.23 HKD. Compared to the recent trading range of 93-97 HKD, this represents an upside potential of approximately 23% to 28%.

- Market Consensus: Most brokerage firms (such as Macquarie and CLSA) maintain a “buy” rating, holding the view that as an industry leader, BYD will capture a larger market share following the current industry consolidation phase.

- Potential Downside Risk:

- Short-term Financial Pressure: Since Q1 2026 net profit attributable to shareholders dropped by over 55% year-over-year, it is evident that intense price competition has significantly eroded profit margins. If gross margins fail to stabilize in subsequent quarters, the stock price may face downward pressure, potentially testing support levels around 80 HKD.

2. Key Influencing Factors (Metrics Investors Should Monitor)

2026 is a critical year for BYD as it shifts from a “sales volume race” to a “quality competition”:

- Gross Margin Stability: Whether BYD can recover profit margins squeezed by the price war through its high-end brand strategy (Denza, Yangwang, Fangchengbao) and an optimized overseas sales mix is the key to determining whether the stock price will reverse upward.

- Overseas Expansion Efficacy: While global expansion (e.g., factories in Southeast Asia, Europe, and Latin America) is a long-term positive, the high initial capital expenditures and execution complexity could become a burden on the stock price in the short term if they fail to generate cash flow as expected.

- Industry Consolidation: The Chinese EV market is undergoing structural adjustments. If weaker competitors exit the market, market share is expected to concentrate among top-tier players like BYD, which is a long-term positive for the company’s valuation.

3. Investment Expert Recommendations

- Short-term Strategy: The stock is currently in a medium-term consolidation phase. Investors are advised to closely monitor quarterly gross margin changes rather than focusing solely on sales figures. If gross margins show signs of improvement for two consecutive quarters, market confidence may recover accordingly.

- Long-term Strategy: For long-term value investors, BYD’s vertical integration capabilities (batteries, electric motors, and electronic controls) remain its core competitive moat. If the stock retraces to key technical support levels (such as the 85-90 HKD range), it may present a value opportunity for layered entry, provided the valuation remains reasonable.

Disclaimer: Stock market investment involves risks. The target prices and analytical data above are based on market reports and consensus from May 2026 and are for reference only; they do not constitute direct trading advice. It is recommended that you evaluate your risk tolerance and assess the company’s progress in overseas production expansion before entering the market.

Source:

- https://car.pchome.com.tw/news_content.html?nid=229408

- https://www.capitalfutures.com.tw/zh-tw/Financial/BreakingNewsArticle?ContentId=C26042800894

- https://www.digitimes.com.tw/tech/dt/n/shwnws.asp?id=0000753760_HDK6XU1N7NY8WOLRBCRKT

- https://news.futunn.com/en/post/73392847/byd-002594-q1-2026-commentary-results-in-line-with-expectations

Back to BYD page