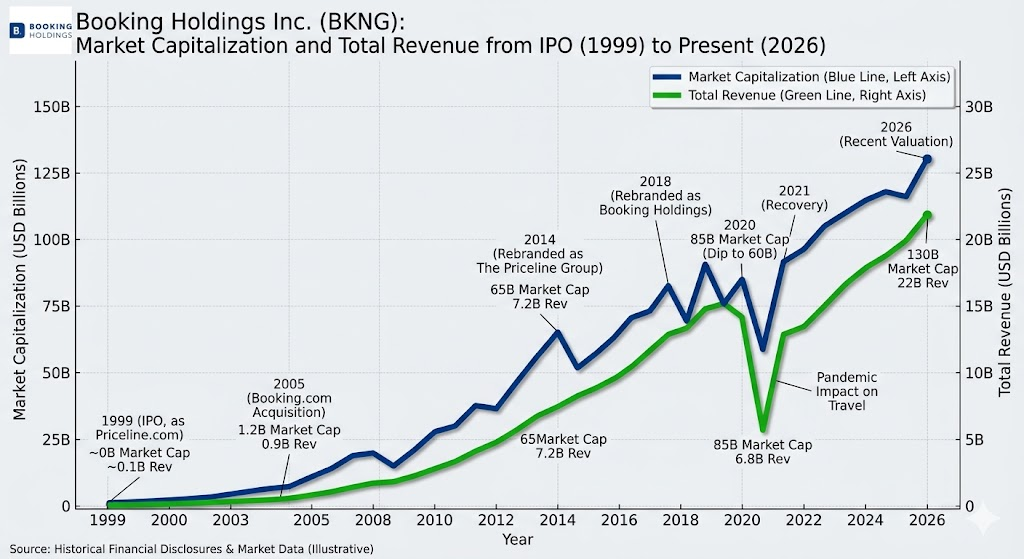

The evolution of Booking Holdings can be divided into four distinct phases, tracking its journey from a niche startup to a global travel technology titan:

1. Inception and Early Growth (1996–2004)

The company was founded in 1996 as Priceline.com by Jay Walker. It gained fame for its unique “Name Your Own Price” business model, which allowed consumers to bid on flights and hotels. The company went public on the Nasdaq in 1999 and navigated the volatile market shifts during the dot-com bubble era.

2. Strategic Acquisitions and Transformation (2005–2012)

This period was critical in establishing the group’s dominance. In 2005, the company acquired the Dutch startup Booking.com for approximately 135M USD, which would eventually become the primary engine for the group’s revenue and profitability. Through further strategic acquisitions, such as Agoda in 2007 and Rentalcars.com in 2010, the group built a massive competitive moat in global accommodation bookings.

3. Globalization and Brand Consolidation (2013–2017)

The company rebranded as The Priceline Group in 2014 to reflect its diversified portfolio. During this phase, the focus shifted toward integrating brand resources and expanding the service ecosystem. Key acquisitions included the travel metasearch engine Kayak in 2013 and the restaurant reservation platform OpenTable in 2014, marking a transition from a hotel-centric model to a comprehensive travel experience provider.

4. Platform Ecosystem and Deep Integration (2018–Present)

In 2018, the company officially rebranded as Booking Holdings, highlighting the dominance of the Booking.com brand. The core strategy in this phase is the “Connected Trip,” which aims to offer seamless travel experiences by integrating flights, accommodations, ground transportation, and activities into a single application. In the post-pandemic era, the focus has expanded to leveraging AI to optimize personalized recommendations and service workflows.

Booking Holdings currently holds the dominant position in the global online travel agency (OTA) industry, yet it faces significant tests from market structure shifts, geopolitical instability, and technological disruption. Here is the competitive analysis:

1. Core Competitive Advantages

- Operational Efficiency and Scale: With a diverse portfolio including Booking.com, Agoda, and Kayak, the company leverages massive data and economies of scale to maintain industry-leading profit margins and cash flow (free cash flow reached 9.1B USD in 2025).

- Genius Loyalty Program: The tiered loyalty system drives high stickiness and repeat booking rates. Genius Level 2 and Level 3 members contribute over 50% of total room nights.

- Global Infrastructure: The ability to handle 100+ payment methods and 50+ currencies while maintaining regulatory compliance across 200+ countries serves as a massive moat that is difficult for smaller platforms to replicate.

- Connected Trip Strategy: By integrating flights, car rentals, accommodations, and local experiences, the group reduces friction for travelers and successfully increases cross-selling transaction volumes.

2. Key Competitors

- Airbnb: The primary competitor, focused on alternative accommodations and experiences. Airbnb possesses stronger brand design and community engagement, and its asset-light business model results in superior FCF conversion compared to Booking.

- Google (Google Travel): As the search gatekeeper, Google exerts significant pressure by offering direct comparison and booking tools within search results, effectively siphoning traffic and driving up Booking’s Customer Acquisition Costs (CAC).

- Expedia: A traditional OTA rival. Despite recent headwinds from geopolitical issues—such as soft demand in the Middle East and Mexico—it remains a major global player in the travel channel.

3. Challenges and Risks

- AI Paradigm Shift: The market is concerned that generative AI might fundamentally change how consumers book travel, potentially leading to “disintermediation” where Large Language Models (LLMs) replace the need for OTA search interfaces. Booking is countering this with its AI Trip Planner, leveraging its proprietary data for more accurate, personalized recommendations.

- Regulatory Pressure: Particularly in the EU, the Digital Markets Act (DMA) has designated Booking.com as a “gatekeeper,” limiting its use of data and self-preferencing tactics, which may increase compliance costs and limit ranking strategies.

- Geopolitical Risk: Since early 2026, conflict in the Middle East has significantly dampened regional travel demand, forcing Booking to lower its annual revenue outlook and highlighting the company’s vulnerability to macroeconomic instability.

4. Competitive Summary

| Factor | Booking Holdings | Airbnb | Google Travel |

| Primary Focus | Comprehensive Travel Ecosystem | Homestays & Unique Experiences | Search & Traffic Gateway |

| Key Strengths | Scale, Data, Payment Infra | Brand Design, Community | Traffic Monopoly, AI Integration |

| 2026 Outlook | Adapting to Regs & Regional Risks | Expanding share, flexible leverage | Squeezing OTA via tech evolution |

In conclusion, Booking Holdings’ strategy centers on increasing user frequency through the Connected Trip and maintaining its barrier to entry via AI-driven data optimization. While facing growth normalization, its robust profitability and structural dominance in the accommodation market make it difficult to replace in the near term.

Source:

- https://www.etoro.com/au/news-and-analysis/stocks/booking-holdings-is-ai-killing-this-travel-giant-bkng-2026/

- https://www.tikr.com/blog/booking-holdings-stock-is-down-27-in-2026-is-bkng-stock-now-undervalued

- https://www.tikr.com/blog/airbnb-vs-booking-holdings-which-travel-stock-is-the-smarter-pick

- https://s201.q4cdn.com/865305287/files/doc_financials/2026/q1/Q1-26-Prepared-Remarks-for-Website.pdf

Back to Booking page