Foundation and Core Focus (1988–1994)

BlackRock was founded in 1988 by Larry Fink and seven partners, initially operating under the umbrella of the private equity firm Blackstone. The founding team focused heavily on risk management and fixed-income investing. Driven by their bond market expertise and proprietary risk analysis tools, the firm achieved rapid profitability. In 1992, the company officially adopted the name BlackRock, and by 1994, it separated from Blackstone due to equity distribution disputes.

Independence and Technological Evolution (1995–2004)

Following its split from Blackstone, BlackRock was acquired by PNC Financial Services Group. A defining milestone of this era was the introduction of the Aladdin investment management platform. Originally developed for internal risk management, Aladdin became the analytical backbone of the company and was later commercialized for major global financial institutions, securing BlackRock a dominant position in investment technology. In 1999, BlackRock went public on the New York Stock Exchange.

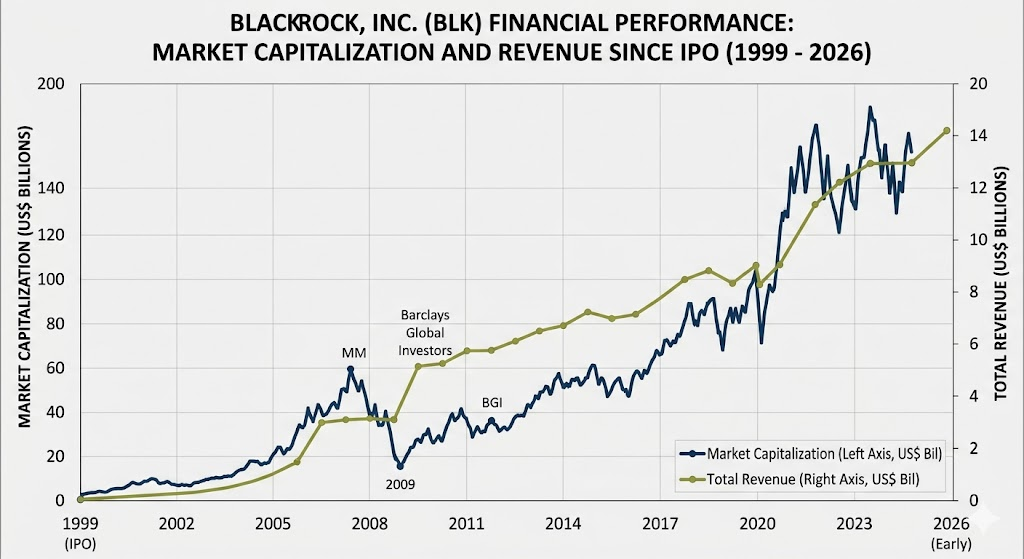

Strategic Mergers and Market Expansion (2005–2009)

BlackRock achieved exponential growth in assets under management through a series of transformative global acquisitions. In 2006, the firm acquired Merrill Lynch Investment Managers (MLIM), significantly expanding its international distribution channels and product lineup. The ultimate turning point arrived in 2009 during the global financial crisis, when BlackRock acquired Barclays Global Investors (BGI). This transaction brought the industry-leading iShares ETF business into its portfolio, propelling BlackRock to its position as the world’s largest asset manager and pioneering the passive investing movement.

Digital Transformation and Alternative Infrastructure (2010–Present)

As the undisputed leader in global asset management, BlackRock continues to expand its Aladdin technology ecosystem and integrate sustainability into its long-term investment frameworks. In recent years, the firm has actively scaled its presence in digital assets and alternative investments. This strategic pivot was highlighted by the acquisition of Global Infrastructure Partners (GIP), positioning BlackRock at the forefront of financing next-generation infrastructure, including artificial intelligence data centers and energy transition projects.

BlackRock is the undisputed titan of the global asset management industry, with its assets under management (AUM) hovering between 10.5M and 11M. The firm’s competitive edge lies in its multi-engine business model, spanning passive, active, and private markets, all tied together by financial technology. However, it faces intense competition across three distinct financial sectors.

1. Passive Investing and the ETF Market: The Duopoly Clash

In index funds and ETFs, BlackRock’s iShares and Vanguard form a global duopoly. While both control the market, their strategic execution and customer segments differ:

- Vanguard: Controlling roughly 9M to 10M in AUM, Vanguard is BlackRock’s closest rival. Organized under a unique mutually owned structure, Vanguard excels in high-volume, low-cost retail funds, enjoying immense loyalty in 401k plans and target-date fund channels.

- BlackRock’s Counter: iShares holds the upper hand among institutional clients, cross-border distribution networks, and core market liquidity. BlackRock consistently counters Vanguard by pioneering active ETFs, fixed-income ETF ladders, and thematic crypto products like its bitcoin spot ETF (IBIT), capturing fast-moving market segments before its rival.

- State Street Global Advisors (SSGA) & Invesco: SSGA (managing around 4M in AUM) relies on its massive asset-servicing parent company to lock in mega-institutional mandates, driven by the highly liquid SPDR S&P 500 ETF (SPY). Meanwhile, Invesco uses its flagship QQQ series to dominate large-cap growth segments, directly peeling market share away from iShares.

2. Private Markets and Alternative Investments: The Scale Expansion

As fee compression dampens margins in public markets, BlackRock is aggressively expanding into high-margin private markets. This strategic shift places it in direct competition with elite, pure-play private equity firms:

- Blackstone: As the world’s largest alternative asset manager (with over 1B in AUM), Blackstone commands unmatched brand prestige in real estate, private equity, and opaque private credit markets.

- BlackRock’s Counter: BlackRock is executing a scale-driven roll-up strategy. By acquiring Global Infrastructure Partners (GIP), private debt platforms, and data providers like Preqin, BlackRock is aggressively pitching a “whole-portfolio” solution. This allows institutional clients to seamlessly manage public and private assets in one place, positioning BlackRock at the forefront of financing next-generation AI data centers and energy infrastructure projects.

- Apollo, KKR, and Carlyle: These traditional private equity heavyweights hold deep domain relationships and structures tailored for complex asset configurations. While BlackRock brings massive scale and corporate distribution networks, it must still prove that its organic returns can consistently match the track records of these specialist alternative houses.

3. Investment Technology: The Unassailable Aladdin Moat

Unlike standard asset management peers, BlackRock’s most resilient competitive barrier is its proprietary investment operating system, Aladdin.

- The Competitive Threat: Competitors include State Street Alpha, Bloomberg PORT, and internal software frameworks built by financial conglomerates like Fidelity.

- BlackRock’s Absolute Monopolization: Aladdin serves over 1,000 global institutional clients, from sovereign wealth funds to insurance companies, providing complete end-to-end portfolio management and risk analytics. This software-as-a-service (SaaS) model yields high-margin, recurring revenues and erects steep switching costs. Because a substantial double-digit percentage of all global financial assets are processed through Aladdin, no other asset manager possesses a digital footprint of this magnitude.

Summary of Competitive Outlook

- Core Strengths: BlackRock stands alone as a financial conglomerate capable of combining institutional ETF liquidity (iShares), mission-critical fintech (Aladdin), and multi-billion infrastructure capabilities (GIP). This diverse architecture drives robust cross-selling and high client retention.

- Vulnerabilities and Risks: The firm remains exposed to structural fee compression in standard public mutual funds. Additionally, its prominent stance on ESG (Environmental, Social, and Governance) principles has drawn political crossfire in the U.S. from both conservative and progressive factions, creating ongoing regulatory and public relations friction alongside macroeconomic geopolitical shifts.

Source:

- https://www.blackrock.com

- https://www.ishares.com

- https://www.vanguard.com

- https://www.blackstone.com

- https://www.ssga.com

Back to BlackRock page