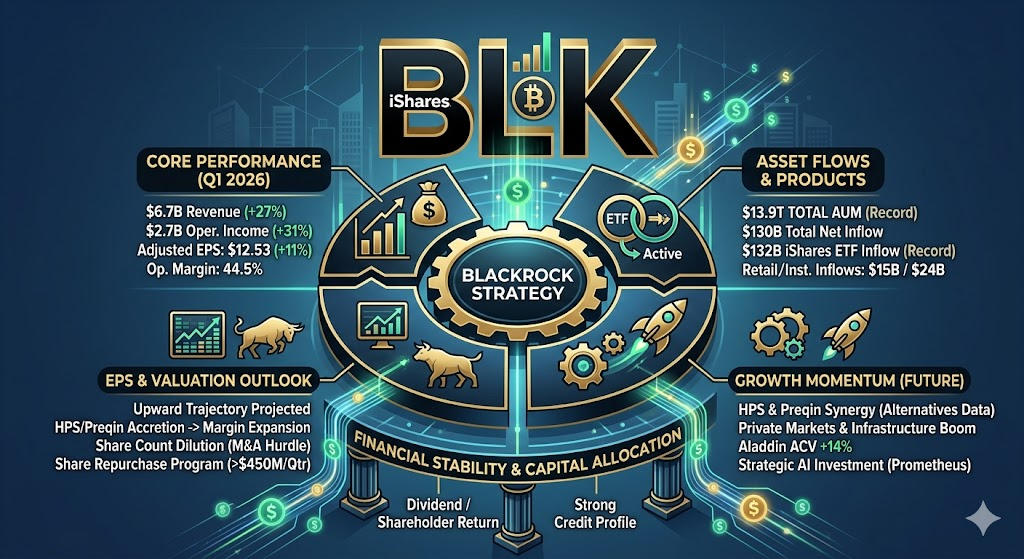

Core Financial Performance

- Revenue: $6.7B, up 27% year-over-year

- Operating Income: $2.7B, up 31% year-over-year

- Diluted Earnings Per Share (EPS): $12.53, up 11% year-over-year

- Operating Margin: Expanded by 130 basis points to 44.5%

Capital Return and Outlook

- Share Repurchase Program: Maintained at a minimum of $450M per quarter for the full year

- Estimated Tax Rate: Projected at 25%

BlackRock demonstrated strong growth momentum in the first quarter of 2026, driven by several key developments and operational milestones across core business segments:

Assets Under Management (AUM) and Fund Flows

- Total Assets Under Management reached a record high of approximately $13.9 trillion, representing a robust 20% year-over-year increase.

- Total net inflows for the quarter reached $130B. Growth was primary anchored by the iShares ETF platform, which captured a record $132B in quarterly net inflows (boosted by strong momentum in the iShares Bitcoin Trust IBIT, as well as international and precision instruments).

- Retail long-term products secured $15B in net inflows, while active institutional strategies added another $24B, offsetting minor outflows within institutional index mandates.

Strategic M&A and Business Diversification

- The double-digit expansion in top-line revenue was propelled by favorable market tailwinds and organic base-fee growth, alongside the full-quarter revenue consolidation of the previously completed HPS (private credit and markets) and Preqin (private markets data) acquisitions.

- Performance fees surged past 350% year-over-year to $272M, up from $60M in the same quarter last year. Notably, $121M of this performance revenue originated directly from the acquired HPS business, validating BlackRock’s expansion into high-margin alternative investment strategies.

Technology Services and Subscription Revenue

- Technology revenue climbed 22% year-over-year to $530M. This growth was driven by sustained institutional demand for the Aladdin risk-management platform, coupled with the first full-quarter consolidation of Preqin, which added roughly $65M. Annual Contract Value (ACV) posted a 14% year-over-year growth rate.

Financial and Capital Structural Shifts

- Although operating margins expanded via scale efficiencies, the 11% increase in Adjusted EPS slightly lagged behind the 27% and 31% expansion seen in revenue and operating income, respectively. This variance reflects a lower non-operating income print, a higher effective tax rate, and an increased diluted share count resulting from equity issued for recent acquisitions.

BlackRock highlighted three core drivers expected to power its continuous growth momentum in the upcoming quarters, as detailed in its recent Q1 earnings call and Q2 investment outlook:

Private Markets & Alternatives Synergy Deepening

- Full Integration of HPS and Preqin: The previously acquired HPS (private credit) and Preqin (private markets data services) only recently began consolidated financial reporting in Q1. In the quarters ahead, BlackRock plans to aggressively cross-sell these platforms across its massive institutional client network to drive revenue upside.

- Infrastructure and Private Credit Demand: As the global rollout of AI data centers and energy infrastructure scales rapidly, institutional capital is leaning heavily into private equity and private credit solutions. BlackRock’s strong fundraising and deployment momentum in these segments is anticipated to translate directly into high-margin base fees and performance fees.

Technology Services and AI Ecosystem Expansion

- Aladdin Platform ACV Growth: The Aladdin risk-management platform continues to see robust institutional adoption, maintaining a 14% year-over-year expansion in Annual Contract Value (ACV). With the rolling out of new feature suites and deeper data integration with Preqin, technology subscription revenue is projected to sustain its double-digit growth trajectory.

- Frontier Tech Strategic Investments: BlackRock recently announced its role as a core strategic investor in Jeff Bezos’s $10B “Project Prometheus,” which targets frontier AI technologies. This strategic positioning in AI workflows and automation tools is anticipated to structurally lower non-compensation operating expenses and enhance margin efficiency over the medium to long term.

Asset Rotation from Cash to Long-Term Products

- ETF and Active Equity Capital Inflows: Following the record-breaking asset gathering by the iShares ETF platform (including digital assets like IBIT) in Q1, management indicated that clients are continuing to reallocate cash. As global macroeconomic and geopolitical environments recalibrate, money market fund holdings are expected to cycle continuously into international equities, precision exposure products, and systematic active strategies.

- With its total AUM base sitting at $13.9 trillion, BlackRock’s highly diversified positioning across passive indexing, active mandates, technology services, and alternative assets allows it to continuously compound competitive advantages throughout changing market asset rotation cycles.

Following BlackRock’s Q1 2026 earnings release—where adjusted quarterly EPS reached $12.53, outperforming the consensus estimate of $11.48—Wall Street analysts project a resilient, upward trajectory for BlackRock’s EPS over the next twelve months. The key catalysts and structural dynamics shaping this EPS path include:

1. High-Margin Core Growth Accelerating Fundamental EPS

- Scaling the $13.9 Trillion AUM Base: With total Assets Under Management wrapping up the first quarter at a record high, the steady compounding of organic base fees from fixed income, systemics, and digital asset ETFs (such as IBIT) will serve as a foundational tailwind for bottom-line earnings over the coming four quarters.

- M&A Financial Synergies Entering Peak Contribution: The acquisitions of HPS (private credit) and Preqin (private markets data) are undergoing full financial consolidation this year. Having already contributed $121M in performance fees during Q1 alone, the aggressive rollout of cross-selling strategies over the next twelve months is positioned to structurally enhance BlackRock’s operating margin profile and lift overall EPS potential.

- Double-Digit Aladdin Subscription Growth: The Aladdin platform continues to sustain a 14% year-over-year increase in Annual Contract Value (ACV). This high-margin, sticky recurring revenue stream offers excellent downside protection and cash flow predictability for EPS forecasts.

2. Near-Term Share Dilution and Financial Drags

- Share Count Dilution From Recent Closings: Management noted during the earnings call that the equity issued to finalize large-scale acquisitions has expanded the diluted share count. This share expansion explains why the 31% year-over-year growth in operating income translated into a more modest 11% increase in adjusted EPS for Q1. This dilution hurdle will continue to temper the year-over-year EPS growth rate on a per-share basis over the next two to three quarters.

- Tax Rate and Non-Operating Normalization: BlackRock has projected its full-year 2026 effective tax rate at a normalized 25%, which tracks slightly higher than several historical quarters. Combined with a lower run-rate in non-operating investment income, net income growth faces mild near-term friction.

3. Wall Street Consensus and Forward Outlook

- Forward Twelve-Month Trend: The broader market consensus expects BlackRock’s EPS path to accelerate in the latter half of 2026 and early 2027. As the revenue and operational synergies from HPS and Preqin unlock at scale, the accretion from high-margin alternative products is projected to comfortably outpace the initial share dilution.

- Capital Return Support: BlackRock’s commitment to executing at least $450M in quarterly share repurchases remains a core pillar of its capital allocation strategy. Steady share retirements will gradually neutralize the dilutive effects of recent M&A activity, reinforcing a solid floor for EPS performance over the coming year.

From an investment standpoint, BlackRock (NYSE: BLK) is highly regarded as a premier growth-oriented blue-chip stock. Below is an institutional perspective on the stock rating and its potential upside based on current market dynamics.

For medium-to-long-term investors seeking resilient capital appreciation, steady dividend compounders, and exposure to private credit and infrastructure booms, BlackRock remains a core portfolio candidate.

- The Bull Case (Core Catalysts)

- Impenetrable Economic Moat: Commanding a massive $13.9 trillion asset base, its iShares ETF ecosystem and digital asset instruments (such as IBIT) capture dominant market share, turning base management fees into a reliable compounding engine.

- High-Margin Secular Drivers: The integration of HPS (private credit) and Preqin (private markets data) elevates BlackRock’s pricing power in alternative assets. Revenue synergies and cross-selling capabilities are poised to expand operating margins over the coming year.

- Sticky Technology SaaS Platform: The Aladdin risk-management platform maintains a robust 14% year-over-year expansion in Annual Contract Value (ACV), guaranteeing highly predictable, recurring software revenues that insulate the business during broader market downturns.

- Shareholder-Friendly Capital Allocation: Backed by a pristine credit profile, the management’s commitment to returning capital through at least $450M in quarterly share repurchases provides consistent downside support.

- The Bear Case (Key Risks)

- Near-Term Per-Share Dilution: The share issuances utilized to fund its major private market acquisitions have expanded the diluted share count. This capital structural shift will temper year-over-year EPS expansion metrics over the next few quarters.

- Premium Valuation Multiple: Trading at a forward P/E multiple hovering around 19.5x to 19.7x, the stock is fairly valued rather than cheap, making it susceptible to temporary broad-market or macroeconomic corrections.

- Macro Credential Tail Risks: As alternative asset strategies grow to encompass a $210B private credit footprint, asset quality and underwriting performance must be monitored closely in the event of severe economic downturns.

Potential Upside Analysis

With the stock stabilizing around the $1,050 to $1,080 range following its strong Q1 earnings release:

- Wall Street Consensus Target: Approximately $1,254 to $1,265.

- Top-Tier Optimistic Target (Bull Case): Peak analyst estimates range between $1,328 and $1,393.

- Conservative Floor Valuation (Bear Case): Downside protection targets hold firm near $1,140, with Morningstar placing its Fair Value Estimate at $1,150.

Upside Projections

- Consensus Upside Potential: Measuring from the current baseline toward the Wall Street consensus average (~$1,260), the stock offers an attractive 16% to 20% fundamental upside potential.

- Accelerated Growth Scenario: If execution of the HPS/Preqin synergy outpaces expectations in the latter half of the year and alternative performance fees experience a sharper uptick, the target expands toward the ~$1,350 mark, translating to a 25%+ potential upside.

Investment Strategy Suggestion

If your financial objective targets rapid, short-term speculative gains, a mega-cap financial heavyweight like BLK is ill-suited for your approach. However, if you are looking for an institutional-grade anchor that simultaneously capitalizes on secular megatrends—specifically the digitizing of private markets and AI-driven infrastructure funding—buying the dips amidst short-term share dilution noise represents a high-probability entry strategy for long-term capital compounding.

Source:

- https://s24.q4cdn.com/856567660/files/doc_financials/2026/Q1/BLK-1Q26-Earnings-Release.pdf

- https://www.investing.com/news/transcripts/earnings-call-transcript-blackrocks-q1-2026-earnings-beat-expectations-93CH-4612827

- https://www.investing.com/news/company-news/blackrock-q1-2026-slides-eps-beats-on-record-flows-13-organic-growth-93CH-4612994

- https://www.blackrock.com/corporate/newsroom/press-releases/article/corporate-one/press-releases/blackrock-reports-first-quarter-2026

- https://www.stocktitan.net/sec-filings/BLK/8-k-black-rock-inc-reports-material-event-6cb2a32ffcb4.html

Back to BlackRock page