Foundation and Initial Growth (1965–1970s)

Analog Devices was founded in 1965 by MIT graduates Ray Stata and Matthew Lorber in Massachusetts, initially operating out of a basement to manufacture modular operational amplifiers. The company went public in 1969 and shifted its focus in the 1970s toward high-performance monolithic analog integrated circuits (ICs), establishing its foundational expertise in solid-state signal processing.

Diversification and the Rise of DSP (1980s–1990s)

Recognizing the dawn of the digital era, ADI heavily invested in digital signal processing (DSP) technologies during the 1980s, eventually launching the acclaimed SHARC processor family. This period marked ADI’s successful expansion from purely analog components into the digital realm, securing major design wins in aerospace, defense, and early cellular communications infrastructure.

Market Expansion and Consumer Electronics (2000s–Early 2010s)

With the explosion of mobile phones and consumer technology, ADI diversified its portfolio to capture high-volume markets. The company became a pioneer in Micro-Electro-Mechanical Systems (MEMS) sensors, which were widely adopted in automotive airbag systems and smartphones, fueling rapid revenue growth and cementing its reputation in high-performance signal processing.

Mega Mergers and Building a Technological Moat (2014–2021)

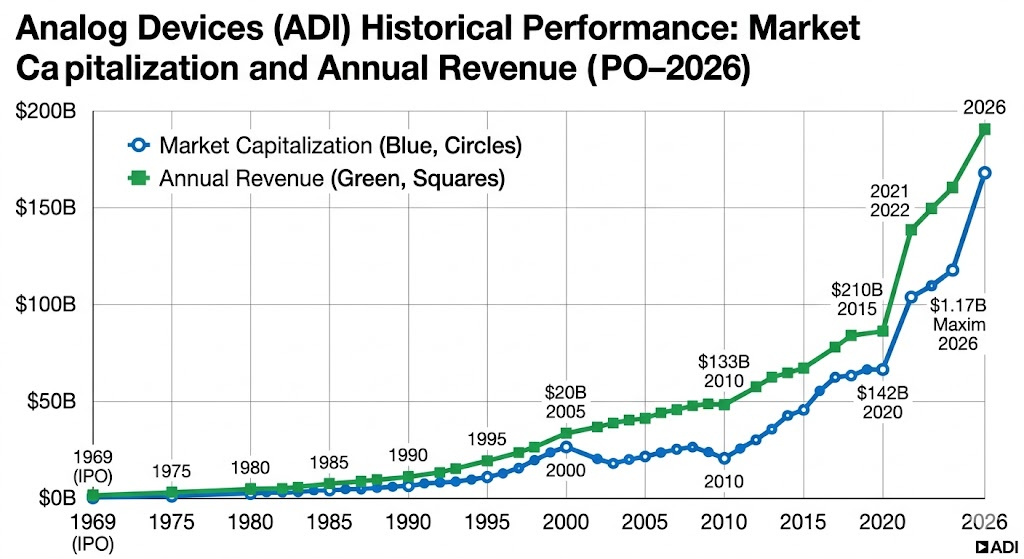

To address the complexity of the Internet of Things (IoT) and advanced automotive systems, ADI executed a series of aggressive strategic acquisitions. It acquired Hittite Microwave in 2014 to boost RF and microwave capabilities, bought power management leader Linear Technology in 2017 for 14.8B, and completed the acquisition of Maxim Integrated in 2021 for 21B. These mergers created an unmatched high-performance analog and power portfolio.

The Intelligent Edge and Digital Transformation (2022–Present)

Today, ADI is focused on advancing the “Intelligent Edge,” integrating sensing, measuring, power management, and edge AI software. Driven by the demands of Industry 4.0, electric vehicles (particularly battery management systems), and next-generation communications, the company continues to bridge the physical and digital worlds to accelerate global digital transformation.

Analog Devices (ADI) operates as a dominant force in the global analog semiconductor market, consistently holding the number two market share position. The analog chip industry is characterized by long product lifecycles, heavy reliance on specialized engineering experience rather than Moore’s Law, and high customer switching costs. Below is the competitive analysis for ADI:

Market Landscape and Core Competitors

The top two giants in the analog semiconductor market, Texas Instruments (TI) and ADI, command a significant portion of the total market share, followed by European and Japanese automotive and industrial specialists.

| Competitor | Core Strengths & Positioning | Competitive Dynamics with ADI |

| Texas Instruments (TI) | The undisputed market leader with over 17% market share. TI relies on its massive internal 300mm (12-inch) wafer fab capacity, focusing on catalog breadth and aggressive cost control. | General Purpose vs. High Performance: TI dominates in volume and cost efficiency through its massive catalog, whereas ADI focuses on higher-margin, high-precision signal chains and customized premium solutions. |

| Infineon Technologies | The European powerhouse leading in power semiconductors and automotive chips, with dominant positions in IGBTs, Silicon Carbide (SiC), and microcontrollers. | Automotive and Power Clash: Both compete fiercely in the electric vehicle (EV) sector. ADI penetrates via its industry-leading Battery Management Systems (BMS), while Infineon leads in power powertrains and discrete components. |

| STMicroelectronics (ST) | Well-positioned in automotive, industrial, and microcontrollers (MCUs), with additional strengths in image sensors and MEMS. | Intelligent Edge Confrontation: ST and ADI cross paths heavily in Industry 4.0 applications, smart sensing, and processing data at the edge. |

ADI’s Core Competitive Advantages (The Moat)

- Absolute Dominance in Data Converters: ADI maintains a commanding global market share in high-performance Analog-to-Digital Converters (ADCs) and Digital-to-Analog Converters (DACs). This technology represents the critical choke point for converting physical-world phenomena into digital data.

- The “Total Solution” Portfolio via Mega Mergers: By absorbing Linear Technology and Maxim Integrated, ADI effectively bridged its historical gap in high-performance power management (PMICs). It can now offer customers a complete, tightly integrated signal chain—from sensing and conversion to processing and power routing.

- Extreme Customer Stickiness: Serving over 125,000 customers worldwide, ADI derives more than 70% of its revenue from the industrial and automotive sectors. These clients prioritize long-term reliability over rock-bottom pricing. Once designed into a system, an ADI chip routinely sees a production lifecycle of over a decade, making switching costs prohibitively high.

Challenges and Structural Risks

- The Fab-lite vs. Fab-owned Conundrum: Competitor TI has invested tens of billions into building out its own internal 300mm manufacturing capacity to drive down per-chip costs and guarantee supply. In contrast, ADI relies on a “Fab-lite” model, outsourcing a significant portion of its leading-edge manufacturing to external foundries like TSMC. This model exposes ADI to higher margin pressures if TI initiates an aggressive industry price war.

- The AI Data Center Power Race: The exponential rise of AI accelerators and hyper-scale data centers has created a fierce battleground for advanced power delivery, specifically Vertical Power Delivery (VPD). While ADI is aggressively expanding its footprint here—boosted by selective acquisitions—niche power specialists like Monolithic Power Systems (MPS) and Vicor have captured strong early traction in high-current AI power stages.

Source:

Back to Analog Devices page