1932–1960s: Founding and Military Foundation

Amphenol was founded in Chicago in 1932 by Arthur J. Schmitt, initially manufacturing tube sockets for radio equipment. The company experienced explosive growth during World War II, becoming a critical supplier of connectors for military aircraft, radar, and communications, establishing its lifelong foundation in high-reliability aerospace and defense sectors.

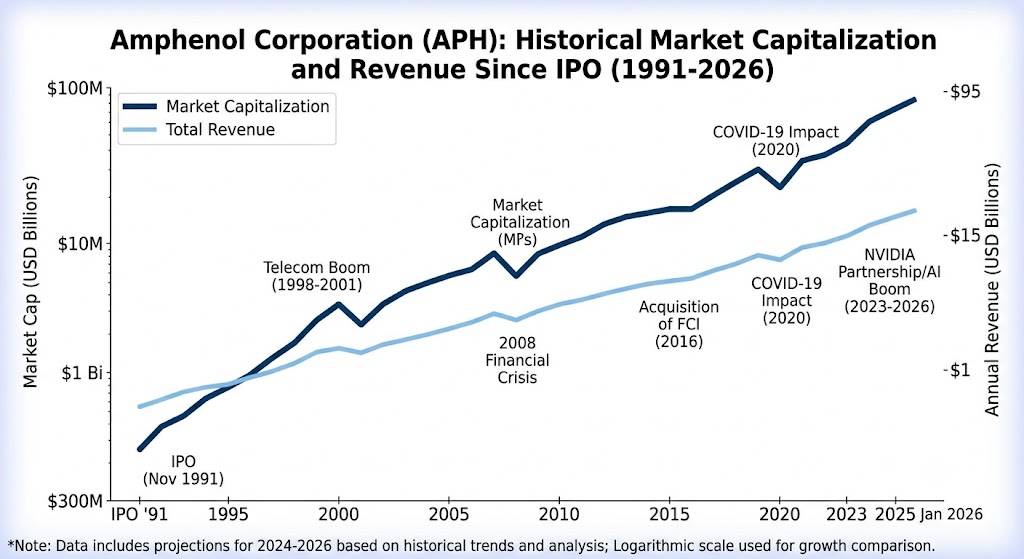

1970–1990s: Expansion and the Acquisition Strategy

In the 1970s, Amphenol expanded into the emerging telecommunications and computing markets. A pivotal moment came in 1987 when the company was acquired by LPL Investment Group, which established the decentralized management and aggressive M&A playbook that defines the company today. Amphenol went public on the NYSE in 1991, accelerating its growth by buying specialized connector manufacturers.

2000–2010s: Global Footprint and the Tech Boom

Entering the 21st century, Amphenol expanded its global manufacturing footprint, particularly in Asia, to capture the booming mobile communications and internet infrastructure markets. The company diversified heavily into automotive electronics—such as airbag and infotainment systems—and strategically acquired sensor companies, moving beyond pure interconnect solutions into advanced sensing technology.

2020s–Present: AI Data Centers and the EV Era

Today, Amphenol is riding the wave of the AI revolution and next-generation mobility. As advanced computing demands unprecedented bandwidth, Amphenol’s high-speed copper and fiber solutions have become essential components for modern AI server architecture and data centers. Concurrently, the company has deeply penetrated the electric vehicle sector, providing high-voltage interconnects for power management systems.

In the global interconnect industry—a market valued near $100 billion—Amphenol consistently ranks as the world’s second-largest player, standing alongside its chief rival TE Connectivity as one of the two industry titans.

The competitive landscape for Amphenol can be analyzed across three major dimensions: the rival landscape, core competitive advantages, and critical market battlegrounds.

1. The Rival Landscape

- TE Connectivity (The Scale Leader): As the market leader, TE possesses a slightly larger revenue scale and immense economies of scale in high-volume, standardized production for the automotive and industrial sectors. While Amphenol focuses on agility and high-margin niches, TE typically secures rigid, long-term alignments with high-volume Tier 1 supply chains.

- Molex (The Technology Heavyweight): Owned by Koch Industries and ranking third globally, Molex is highly verticalized and commands strong market share in consumer electronics, automotive infotainment, and data centers. It acts as one of Amphenol’s most formidable direct competitors in high-speed hyperscale data center architectures.

- Samtec & Specialized Niche Players: Samtec excels in board-level high-speed connectivity and silicon-to-silicon packaging (such as PCIe and SerDes architectures). In cutting-edge computing where extreme Signal Integrity (SI) is paramount, Samtec exerts significant pressure on Amphenol. Meanwhile, players like Rosenberger and Hirose present high-frequency RF and telecommunication barriers.

- Asian Scale and Cost Challengers (Foxconn/FIT, Luxshare Precision): Utilizing their massive consumer electronics manufacturing footprints, these companies have rapidly moved up the value chain into server, data center, and EV wire harness markets, competing fiercely on price for mid-to-low tier or commoditized interconnect products.

2. Amphenol’s Core Competitive Advantages (The Moat)

- Decentralized Operating Model: Unlike most large conglomerates that rely on centralized corporate management, Amphenol operates over 130 highly independent, entrepreneurial business units. This decentralized architecture allows localized general managers to respond to custom design modifications or engineering requests from major tech clients like NVIDIA or Tesla within days, offering unmatched agility.

- Aggressive M&A Execution: Amphenol functions as an institutionalized “acquisition machine,” consistently buying 5 to 10 specialized technology firms annually. This playbook allows the company to instantly bridge technological gaps in emerging sectors (such as specialized sensing or advanced optics) while preemptively absorbing potential market disruptors.

- High-Margin, Defensive Portfolio Mix: Amphenol holds a dominant global market share in harsh-environment connectors utilized in military, aerospace, and heavy industrial applications. These segments feature long qualification cycles and extreme engineering friction, making supplier switching highly prohibitive. This provides a stable bedrock of high-margin cash flow, keeping Amphenol’s operating margins consistently above 21%—outperforming the industry average.

3. Critical Market Battlegrounds & Current Dynamics

- AI Data Centers & Hyper-Computing: In the race for AI infrastructure, Amphenol partnered closely with major chipmakers like NVIDIA to design advanced 800G and 1.6T high-speed copper and fiber solutions, granting it a dominant early footprint in GPU clustering. However, as tech giants adopt multi-sourcing strategies to mitigate supply chain risks, Molex and Samtec are rolling out rival architectures, escalating competitive pressure.

- Electric Vehicles & Smart Mobility: In traditional automotive wire harnesses, Japanese suppliers like Yazaki and Sumitomo, alongside Aptiv, maintain entrenched Tier 1 status. Amphenol deliberately avoids these low-margin, high-volume commodities, focusing instead on high-margin niches: high-frequency RF connectors for ADAS and autonomous driving systems, sensor modules, and high-voltage interconnects for EV battery management systems (BMS).

- The Physics of Transmission (Copper vs. Optical): As transmission speeds push the physical limits of copper wiring, Co-Packaged Optics (CPO) and optical interconnects are gaining traction within next-generation AI topologies. While safeguarding its intellectual property in high-speed copper, Amphenol has accelerated its optics capabilities through targeted acquisitions (such as acquiring CommScope’s mobile networks and wireless assets) to hedge against pure-play optical giants like Corning.

Source:

Back to Amphenol page