Thermo Fisher Scientific’s history is a definitive narrative of strategic mergers and aggressive acquisitions, transforming two separate entities into the world’s leader in serving science.

Here is the evolution of the company broken down into key stages:

1. The Foundation: Two Industry Pillars (1900s – 2005)

Before the 2006 merger, Thermo Electron and Fisher Scientific operated as independent leaders in their respective niches.

- Fisher Scientific (Founded 1902): Established by Chester Garfield Fisher in Pittsburgh. It became the first commercial source for laboratory equipment and reagents in the US. By the late 20th century, it was the dominant global distributor for scientific supplies.

- Thermo Electron (Founded 1956): Founded by MIT professor George Hatsopoulos. The company focused on analytical instrumentation and environmental monitoring. It was famous for its “spin-out” model, creating several specialized publicly traded subsidiaries based on internal R&D.

2. The Landmark Merger: Birth of a Giant (2006)

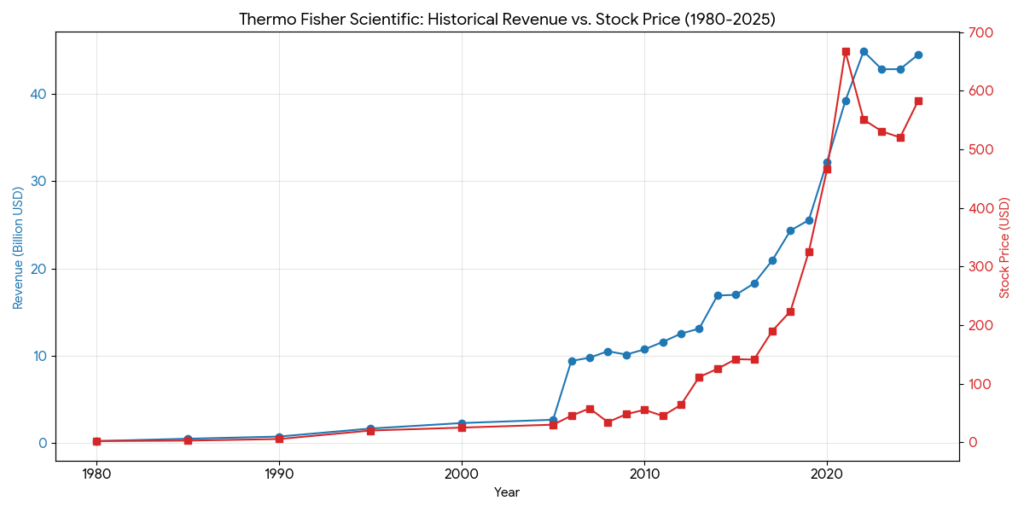

In November 2006, Thermo Electron and Fisher Scientific completed a 10.6 billion USD merger of equals.

- Strategic Rationale: This was a “hardware meets distribution” play. Thermo brought high-end manufacturing (mass specs, spectrometers), while Fisher brought a massive global logistics network and a portfolio of consumables.

- The Result: The combined company became a “one-stop shop” for laboratories, capable of providing everything from a simple pipette to the most complex analytical instruments.

3. Expansion into Life Sciences & Genomics (2013 – 2016)

Following the merger, the company pivoted toward high-growth sectors like biotechnology and precision medicine.

- Acquisition of Life Technologies (2013): A transformative 13.6 billion USD deal. This brought the legendary Applied Biosystems and Invitrogen brands under one roof, giving Thermo Fisher a dominant position in DNA sequencing (NGS) and molecular biology.

- Acquisition of FEI Company (2016): For 4.2 billion USD, Thermo Fisher acquired the leader in electron microscopy. This strengthened their presence in structural biology, particularly in the rising field of Cryo-Electron Microscopy (Cryo-EM).

4. Vertical Integration: CDMO and Clinical Services (2017 – 2021)

Thermo Fisher moved beyond the lab bench and into the drug production and clinical trial phases.

- Acquisition of Patheon (2017): A 7.2 billion USD entry into the Contract Development and Manufacturing Organization (CDMO) space, allowing them to manufacture drugs for pharmaceutical clients.

- Acquisition of PPD (2021): One of its largest deals at 17.4 billion USD. By acquiring a top-tier Clinical Research Organization (CRO), Thermo Fisher completed the “end-to-end” circle: supporting customers from initial discovery to clinical trials and eventual mass production.

5. Present Day: Specialized Diagnostics & Multi-omics (2022 – 2026)

The company continues to fine-tune its portfolio toward high-margin specialty diagnostics and advanced “omics” technologies.

- Key Moves: Acquisitions of The Binding Site (specialty diagnostics) and Olink (proteomics) highlight a focus on the next frontier of medical research: understanding proteins and complex diseases.

In 2026, the competitive landscape for Thermo Fisher Scientific (TMO) is defined by its massive “One-Stop-Shop” scale versus specialized, agile competitors. While TMO leads in total revenue, rivals like Danaher and Agilent challenge it on operational efficiency and technical precision.

1. Key Competitors & Strategic Positioning (2026)

- Danaher (DHR): The Primary Rival.

- Focus: Recently transitioned into a focused life sciences and diagnostics innovator.

- Edge: Known for the Danaher Business System (DBS), which drives higher operating efficiency and capital discipline compared to TMO’s broader approach.

- Market Dynamic: DHR’s Cytiva and Pall brands are dominant in bioprocessing, directly competing with TMO’s bioproduction offerings.

- Agilent Technologies (A): The Instrumentation Leader.

- Focus: Specializes in high-end analytical tools (HPLC, Mass Spectrometry) and genomics.

- Edge: Boasts higher Net Margins (18.75%) and Return on Equity (25.20%) compared to TMO, reflecting a more profitable, focused hardware business.

- Merck KGaA (MilliporeSigma):

- Focus: A powerhouse in laboratory chemicals and biopharma consumables.

- Edge: Deeply embedded in the European and Asian research supply chains, challenging TMO’s Fisher Scientific distribution network.

- CRO/CDMO Challengers:

- Lonza & WuXi Biologics: Major competitors in the CDMO space where TMO’s Patheon operates.

- IQVIA & Medpace: Compete with TMO’s PPD in clinical research services.

2. Comparative Financial Metrics (2025-2026)

| Metric (FY 2025/26) | Thermo Fisher (TMO) | Danaher (DHR) | Agilent (A) |

| Gross Revenue | $44.56B | ~$24.6B | ~$6.8B |

| P/E Ratio | 28.98 | 43.2x | 32.6x |

| Net Margins | 15.05% | ~14.7% | 18.75% |

| Return on Assets | 8.36% | 7.05% | 12.99% |

3. TMO’s Strategic Advantages & Risks (2026)

- Unmatched Scale: TMO’s Fisher Scientific platform remains the “Amazon of the lab,” giving it a distribution moat that smaller rivals cannot match.

- End-to-End Capabilities: Through the integration of PPD (CRO) and Patheon (CDMO), TMO is the only player that can support a drug from discovery through to mass production within one ecosystem.

- The GLP-1 Tailwinds: As a leader in fill-finish services, TMO is a key beneficiary of the massive demand for weight-loss drugs (GLP-1s) in 2026.

- Debt and Complexity: Massive acquisitions (like the $34B PPD deal) have left TMO with higher leverage, potentially limiting its flexibility for new mega-mergers in the short term.

- China Exposure: TMO remains sensitive to “In China, For China” localization policies, where local competitors like MGI Tech are gaining ground in entry-level segments.

4. Market Sentiment (Q1 2026)

- Growth Outlook: TMO’s CEO Marc Casper projects 3-6% organic revenue growth for 2026-2027, with a return to 7%+ growth in 2028.

- Stock Performance: TMO has seen some recent pressure (down ~12% from recent highs), while Danaher is viewed as “richly valued” with a higher P/E, suggesting investors currently pay a premium for DHR’s focused growth over TMO’s broad scale.

Sources:

- Thermo Fisher Strategy Analysis (2026)

- TMO vs DHR Financial Comparison

- J.P. Morgan Healthcare Conference 2026 Highlights

Back to Thermo Fisher page