Here is the history of T-Mobile US broken down into its key evolutionary stages:

Phase 1: The VoiceStream Era (1994–2001)

Before it was T-Mobile, the company operated as VoiceStream Wireless, a subsidiary of Western Wireless.

- 1994: Founded as a regional carrier in Bellevue, Washington.

- 1996: Launched its first digital GSM network in Honolulu and Salt Lake City.

- 1999: Spun off from Western Wireless as a standalone public company.

Core Technology: GSM (Global System for Mobile). While most U.S. carriers (Verizon/Sprint) chose CDMA, VoiceStream adopted the European GSM standard. This later became the technical bridge that attracted Deutsche Telekom.

Core Strategy: Regional Aggregation. The focus was on acquiring smaller regional carriers (Omnipoint, Aerial) to build a patchwork national footprint and listing on the NASDAQ to fund infrastructure.

Revenue Level: Under $2B annually. The company was in a high-growth, high-loss phase typical of early-stage infrastructure deployment.

Phase 2: Acquisition by Deutsche Telekom (2001–2012)

This period marked the official birth of the T-Mobile brand in the United States and a failed attempt at a massive exit.

- 2001: Deutsche Telekom (the German telecommunications giant) acquired VoiceStream for approximately 35 billion dollars.

- 2002: The company was officially rebranded as T-Mobile USA, Inc.

- 2011: AT&T attempted to acquire T-Mobile for 39 billion dollars. However, the deal was blocked by the Department of Justice on antitrust grounds.

- The Silver Lining: T-Mobile received a 3 billion dollars “breakup fee” and valuable spectrum from AT&T, which provided the capital and resources for its future comeback.

Core Technology: 3G (HSPA+). T-Mobile struggled during this phase due to a lack of compatible spectrum for 3G, causing them to fall behind Verizon and AT&T in the early smartphone era. They eventually used “HSPA+” as a marketing “4G” to bridge the gap.

Core Strategy: Global Integration and Survival. Following the $35B acquisition by Deutsche Telekom, the focus was on establishing a unified brand. After the 2011 AT&T merger failed, the strategy shifted to using the $3B breakup fee to modernize the network.

Revenue Level: $18B – $20B annually. Revenue growth was stagnant during the later years of this phase due to high churn rates and the lack of the iPhone (which they didn’t get until 2013).

Phase 3: The “Un-carrier” Movement (2013–2019)

Under the leadership of CEO John Legere, T-Mobile launched the Un-carrier campaign, which disrupted the entire U.S. wireless industry.

- 2013: Merged with MetroPCS and began trading on the NYSE as TMUS.

- Market Disruption: T-Mobile eliminated two-year contracts, introduced free international data roaming, and offered “Simple Choice” plans.

- Rapid Growth: By 2015, T-Mobile overtook Sprint to become the third-largest wireless carrier in the U.S.

Core Technology: 4G LTE Modernization. T-Mobile aggressively deployed LTE using AWS and 700MHz/600MHz spectrum to fix its indoor coverage issues, rapidly closing the quality gap with “The Big Two.”

Core Strategy: Market Disruption (Un-carrier). Led by CEO John Legere, the company eliminated contracts, subsidized device costs, and offered free international roaming. The goal was to be the “customer-centric” alternative to “greedy” incumbents.

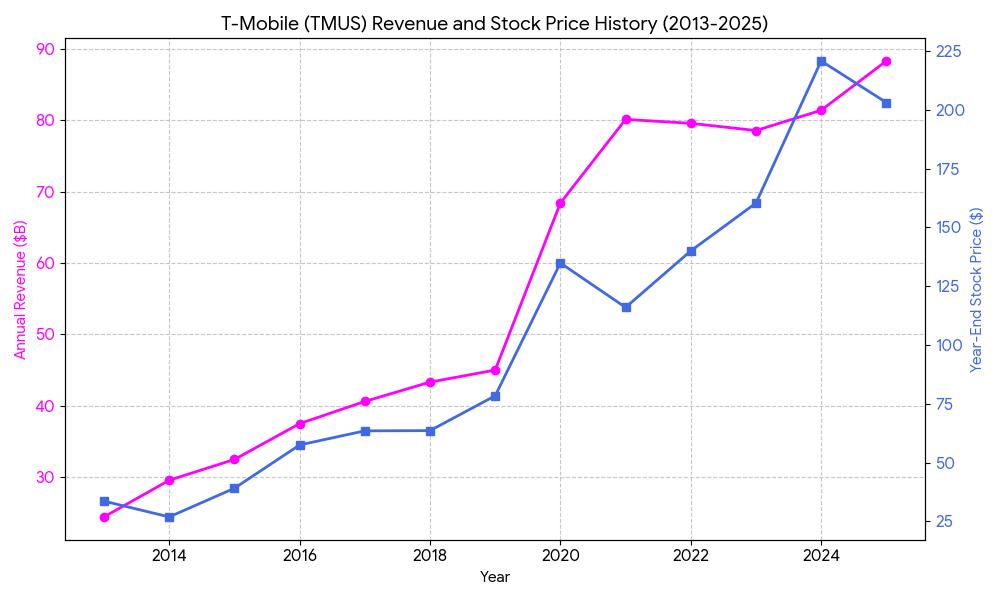

Revenue Level: $24B – $45B annually. This period saw explosive growth. By 2019, revenue had nearly doubled from the start of the Un-carrier era as they became the fastest-growing carrier in the U.S.

Phase 4: 5G Dominance and Sprint Merger (2020–Present)

T-Mobile shifted from a “scrappy underdog” to a dominant market leader by focusing on 5G infrastructure.

- April 2020: Formally completed its 26.5 billion dollars merger with Sprint. This gave T-Mobile a massive hoard of mid-band spectrum (2.5GHz), which became the backbone of its 5G lead.

- 2023–2025: Expanded its reach through strategic acquisitions, including Mint Mobile‘s parent company (KA’ena Corp) and US Cellular‘s wireless operations.

- 2026: As of early 2026, T-Mobile has consistently outperformed Verizon and AT&T in 5G coverage and speed tests, solidifying its position as the top choice for high-speed mobile data in America.

Core Technology: 5G (Mid-band 2.5GHz). Through the Sprint merger, T-Mobile secured a massive lead in mid-band spectrum. This allowed them to offer 5G speeds significantly faster than Verizon’s nationwide 5G and more reliable than mmWave.

Core Strategy: Scale and Fixed Wireless Access (FWA). T-Mobile leveraged its 5G capacity to enter the home broadband market (5G Home Internet), directly attacking cable companies. They also focused on expanding into rural markets and the enterprise sector.

Revenue Level: $70B – $88B+ annually. Post-merger revenue jumped significantly.

- 2020: ~$68.4B

- 2024: ~$81.4B

- 2025: Reached $88.31B, with a focus on maximizing Free Cash Flow (FCF) and shareholder returns through massive buybacks.

Below is a comprehensive competitive analysis of T-Mobile US as of early 2026, comparing its market position, technical edge, and strategic outlook against its primary rivals, Verizon and AT&T.

1. Market Share and Subscriber Dynamics

T-Mobile has successfully transitioned from a “scrappy underdog” to a dominant market force. While Verizon remains the largest by total connections, T-Mobile leads in growth velocity.

- Market Position: As of early 2026, Verizon holds approximately 36% market share, AT&T 32%, and T-Mobile 30%. However, T-Mobile has captured nearly 50% of all industry net additions over the past two years.

- Broadband Invasion: T-Mobile is no longer just a “phone company.” Its 5G Fixed Wireless Access (FWA) service reached 8.5 million customers by the end of 2025, directly stealing market share from traditional cable giants like Comcast and Charter.

- Churn Rate Management: While T-Mobile’s post-paid churn saw a slight uptick to 1.02% in Q4 2025 (partially due to legacy plan adjustments), it remains competitive with Verizon’s premium user base.

2. The 5G Technical Lead

T-Mobile’s “Layer Cake” spectrum strategy has proven superior in the 5G era.

- Speed Advantage: According to 2026 Ookla and J.D. Power reports, T-Mobile’s median download speed is 223 Mbps, more than double that of Verizon (113 Mbps) and AT&T (111 Mbps).

- Mid-Band King: By utilizing the 2.5GHz spectrum acquired from Sprint, T-Mobile offers “Ultra Capacity” 5G to over 300 million people, a reach that Verizon and AT&T are still struggling to match with their C-Band deployments.

- Next-Gen AI Integration: In February 2026, T-Mobile launched an Agentic AI Platform, integrating AI directly into the network layer to optimize traffic and provide real-time translation services for roaming users.

3. Competitor Strategic Comparison (2026)

| Competitor | Core Strategy | Primary Strength | Main Vulnerability |

| T-Mobile | Best Network + Best Value | 5G Speed/Capacity lead; Aggressive FWA growth | Saturation in urban markets; rising customer acquisition costs |

| Verizon | Premium Bundling | High-value enterprise base; Disney+/Netflix/Max bundles | Massive debt from C-Band auctions; slower 5G rollout |

| AT&T | Convergence (Fiber + 5G) | Ownership of fiber infrastructure; FirstNet (Emergency services) | Lower marketing “buzz”; slower subscriber growth |

4. Key Risks and Emerging Threats

- Price Creep: To support its massive $18B+ Free Cash Flow (FCF) goals and shareholder buybacks, T-Mobile has begun raising prices on older “lifetime” plans. This risks damaging the “Un-carrier” brand loyalty.

- The Rise of MVNOs: Cable companies (Xfinity Mobile, Spectrum Mobile) are using Verizon’s network to offer low-cost bundles, putting pressure on T-Mobile’s “value” proposition.

- Capital Intensity: Integrating the US Cellular assets and the Mint Mobile acquisition requires significant Capex, which may temporarily impact margins in mid-2026.

Sources:

- T-Mobile USA Inc. History – BCC Research

- T-Mobile: A Journey Through Mergers, Milestones – Oreate AI

- T-Mobile Hits Historic Milestone – TmoNews

- T-Mobile Overtakes Peers in Subscriber Growth – Wells Fargo (2025)

- T-Mobile Q4 2025 Financial Performance – 24/7 Wall St. (2026)

- Verizon vs T-Mobile vs AT&T: Best 5G Comparison (2026 Guide)

Back to T-Mobile page