Here is detailed breakdown of Philip Morris International’s history, categorized by its most defining eras:

1. The London Roots and Early Expansion (1847–1919)

This period marks the transition from a single shop to a recognized international brand.

- 1847: Mr. Philip Morris opens a single shop on London’s Bond Street, selling loose tobacco and hand-rolled cigarettes.

- 1881: After Philip Morris’s death, the business is taken over by his wife, Margaret, and his brother, Leopold. It eventually goes public.

- 1902: A New York corporation is established to sell British brands (including Marlboro) in the U.S. market.

Core Products: Hand-rolled cigarettes, loose tobacco, and Turkish blends (e.g., Cambridge, Oxford Blues).

Core Strategy: Niche Premium Positioning. Focused on the London elite and later the New York urban market through high-end retail and quality craftsmanship.

Revenue Level: Boutique scale. Revenue was modest but highly profitable per unit, providing the capital for initial transatlantic expansion and incorporation in the U.S.

2. The Rise of Marlboro and Altria Formation (1920s–1980s)

During this stage, the company transformed into a global powerhouse through iconic marketing and corporate restructuring.

- 1924: Marlboro is introduced as a “woman’s cigarette” with the slogan “Mild as May.”

- 1954: In one of the most famous brand pivots in history, Marlboro is repositioned with the “Marlboro Man” to appeal to men, featuring a filter for the first time.

- 1968: Philip Morris International (PMI) is formed as an operating division of Philip Morris Companies Inc. to manage the brand’s rapid growth outside the U.S.

- 1985: Philip Morris Companies Inc. is formed as a holding company, later diversifying into food and beverage (acquiring General Foods and Kraft Foods).

Core Products: Marlboro (Red/Gold), L&M, Parliament, and Virginia Slims.

Core Strategy: Mass-Market Lifestyle Branding. The 1954 “Marlboro Man” pivot redefined cigarettes from a functional habit to a masculine identity. Strategically, PMI expanded through global licensing and localized manufacturing to dominate international markets outside the U.S.

Revenue Level: Exponential growth. By the 1970s, Marlboro became the world’s best-selling cigarette, generating multi-billion dollar cash flows that funded the parent company’s diversification into the food industry.

3. The Great Spin-off (2000s)

This era was defined by legal pressures and the strategic separation of domestic and international interests.

- 2003: Philip Morris Companies Inc. renames itself Altria Group.

- 2008: Philip Morris International (PMI) is spun off from Altria. This was a pivotal moment: Altria kept the U.S. tobacco business (Philip Morris USA), while PMI became a separate, independent company headquartered in Switzerland to focus on international growth and distance itself from U.S. litigation.

Core Products: Cigarettes (Marlboro dominated) and Food/Beverage (Kraft, Miller Brewing).

Core Strategy: Risk Mitigation and De-merger. Under the Altria holding company, the strategy was to shield international earnings from U.S. tobacco litigation. This culminated in the 2008 Spin-off, where PMI became an independent Swiss-based entity focused solely on international growth.

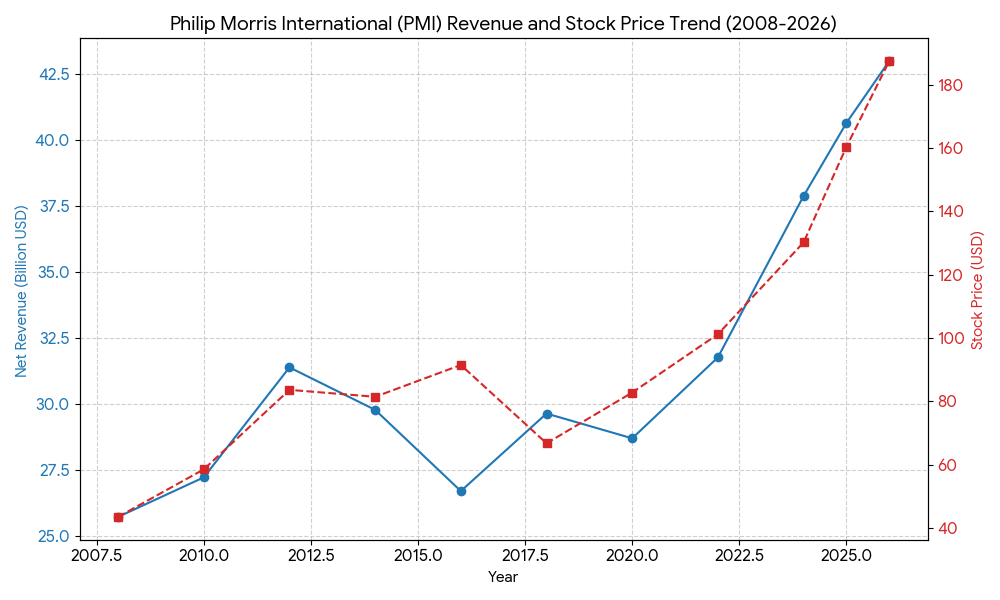

Revenue Level: Stable and high. At the time of the 2008 spin-off, PMI’s net revenues were approximately $25.7 billion, with an operating company income of roughly $10.2 billion.

4. The “Smoke-Free” Transformation (2014–Present)

PMI is currently in its most radical phase, attempting to pivot away from traditional cigarettes entirely.

- 2014: The company launches IQOS (Heat-not-Burn technology) in Nagoya, Japan, and Milan, Italy.

- 2016: PMI officially announces its “Smoke-Free Future” vision, committing to replace cigarettes with smoke-free alternatives as soon as possible.

- 2021-2022: PMI expands beyond tobacco into “Beyond Nicotine” areas, acquiring Vectura (an inhaler drug delivery company) and Swedish Match (the leader in oral nicotine pouches like ZYN).

Core Products: IQOS (Heat-not-Burn), ZYN (Nicotine Pouches), VEEV (E-vapor), and legacy Combustible Cigarettes.

Core Strategy: Business Transformation (RRPs). Shifting R&D and marketing capital away from cigarettes toward Reduced-Risk Products (RRPs). The acquisition of Swedish Match in 2022 was a masterstroke to dominate the oral nicotine category (ZYN).

Revenue Level: * 2024: Net revenues reached $37.9 billion, with smoke-free products accounting for 39% of total revenue.

- 2025: Net revenues surpassed $40 billion, with smoke-free revenue hitting $16.8 billion (41.5%).

- Goal: PMI aims for smoke-free products to exceed 2/3 of total net revenue by 2030.

In 2026, the global tobacco and nicotine landscape is no longer just a battle for cigarette market share; it has evolved into a high-stakes race to own the “Reduced-Risk” future.

Philip Morris International (PMI) is currently the frontrunner in this transition, but its rivals are aggressively attempting to disrupt its dominance in specific categories.

1. Financial & Valuation Comparison (2025/2026)

Market sentiment has clearly diverged. Investors are rewarding PMI with a “Growth Multiplier” while treating its peers more like traditional “Value” stocks.

| Metric (Est. 2025/26) | Philip Morris (PMI) | British Am. Tobacco (BAT) | Altria (MO) |

| Market Cap | ~$280B | ~$111B | ~$110B |

| Forward P/E Ratio | ~19x – 20x | ~11x | ~12x |

| Smoke-Free Revenue % | 41.5% | ~15% – 18% | ~12% – 15% |

| Dividend Yield | ~3.3% | ~8.5% | ~7.8% |

| R&D Intensity | Very High (Tech-led) | Moderate (Multi-category) | Moderate (U.S. Focused) |

2. Strategic “Category” Battlegrounds

A. Heated Tobacco (HTP): IQOS vs. glo & Ploom

PMI holds a near-monopoly in the heated tobacco category with roughly 70% global volume share.

- The Challenger (BAT): Their glo device is priced lower to attract value-conscious smokers, but it lacks the premium “lifestyle” status of IQOS.

- The Challenger (JTI): Their Ploom device is a strong #2 in Japan, using aggressive local marketing to chip away at PMI’s earliest stronghold.

- PMI’s Defense: Continuous innovation (e.g., IQOS ILUMA) and a 72% conversion rate (smokers who switch to IQOS and stop smoking cigarettes) which is significantly higher than competitors.

B. Oral Nicotine: ZYN vs. Velo & on!

This is the fastest-growing segment in the U.S., where PMI is now the dominant force following its acquisition of Swedish Match.

- PMI (ZYN): Holds approximately 66% – 70% value share in the U.S. and is expanding rapidly into Europe.

- Altria (on!): Aggressively competing on price in the U.S. to slow ZYN’s momentum.

- BAT (Velo): The leader in several European markets, providing a strong counter-weight to ZYN’s international expansion.

3. SWOT Analysis of Competitors

- BAT (British American Tobacco):

- Strengths: Most diversified “New Category” portfolio (Vaping, Heating, Oral).

- Weaknesses: Higher debt levels and significant write-downs on traditional U.S. cigarette brands in late 2023.

- Altria (U.S. Rival):

- Strengths: Massive cash flow from the U.S. Marlboro franchise; high dividends.

- Weaknesses: Limited to the U.S. market; struggled with M&A (Juul) before acquiring NJOY.

- Imperial Brands:

- Strengths: “Follower” strategy—focusing on being a highly efficient #3 or #4 with lower R&D risk.

- Weaknesses: Smallest footprint in high-growth smoke-free technologies.

4. The “2030” Race

The ultimate competition is the race to reach 50% smoke-free revenue.

- PMI is on track to hit this by 2026-2027.

- BAT and Altria are lagging behind, likely not reaching that milestone until after 2030.

This gap is why PMI’s stock is trading at a significant premium (19x P/E) compared to its peers (11x-12x P/E). The market no longer views PMI as a “Sin Stock” but as a “Consumer Tech/Wellness” hybrid.

Source:

- https://www.pmi.com/content/dam/pmicom/global/docs/pmi-sustainability/pmi-integrated-report-2024.pdf

- https://www.pmi.com/investor-relations/overview

- https://www.pmi.com/progress/

- https://www.pmi.com/investor-relations/pm-stock-and-bond-information/

- https://companiesmarketcap.com/philip-morris/stock-price-history/

- https://www.pmi.com/our-transformation/delivering-a-smoke-free-future

Back to Philip Morris page