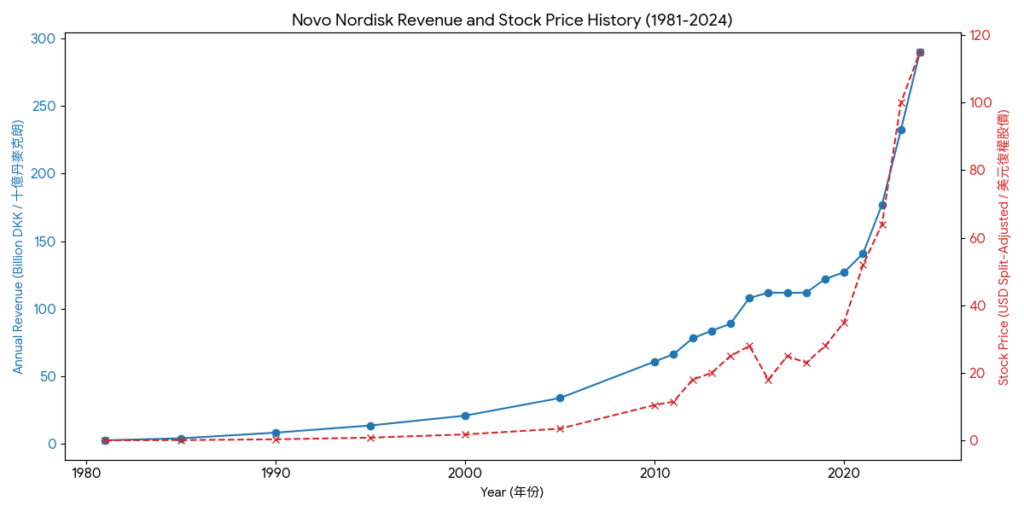

Novo Nordisk has evolved through four major stages, transforming from two rival Danish laboratories into a global leader in metabolic health.

1. The Rivalry Era (1923–1988)

The company’s roots lie in the discovery of insulin and a long-standing competition between two entities.

- The Foundation (1923): Nobel laureate August Krogh and Dr. Hans Christian Hagedorn founded Nordisk Insulinlaboratorium after Krogh brought insulin production technology back from Canada.

- The Split (1925): Former employees of Nordisk, the Pedersen brothers (Harald and Thorvald), founded their own rival company, Novo Terapeutisk Laboratorium.

- Decades of Innovation: Both companies competed to improve insulin. Key breakthroughs included:

- 1946: Nordisk launched NPH insulin, a long-acting formula that reduced the number of daily injections.

- 1985: Novo introduced NovoPen, the world’s first insulin pen, revolutionizing drug delivery.

2. The Merger and Consolidation (1989–1999)

To compete on a global scale, the two fierce rivals decided to unite.

- 1989 Merger: Novo Industri A/S and Nordisk Gentofte A/S merged to form Novo Nordisk A/S, creating the world’s largest insulin producer.

- Operational Focus: The company began streamlining its operations, spinning off IT and engineering units (NNIT and NNE) to focus strictly on healthcare.

3. Biological Breakthroughs & Specialization (2000–2010s)

The turn of the century marked a shift toward high-tech biological engineering and a narrower focus on chronic diseases.

- 2000 De-merger: The industrial enzyme business was spun off as Novozymes, allowing Novo Nordisk to focus 100% on medical treatment.

- GLP-1 Discovery: While continuing to lead in insulin (launching long-acting Levemir in 2004), the company intensified research into the GLP-1 hormone.

- 2010: Launched Victoza (liraglutide), its first GLP-1 for Type 2 diabetes, which laid the groundwork for its future in weight management.

4. The Obesity & Cardiometabolic Era (2017–Present)

Novo Nordisk shifted from being a “diabetes company” to a “metabolic powerhouse.”

- The Ozempic Breakthrough (2017): The FDA approved Ozempic (semaglutide), a once-weekly GLP-1 treatment that proved highly effective for both blood sugar and weight loss.

- Obesity Leadership (2021): The launch of Wegovy (specifically for weight management) propelled the company to record-breaking market valuations.

- Expansion: The company is now expanding into treatments for cardiovascular disease, kidney disease, and liver health (MASH), aiming to treat the broader spectrum of chronic metabolic conditions.

As of 2026, the GLP-1 market is shifting from a duopoly to an intense multi-player race. While Novo Nordisk and Eli Lilly still dominate, new entrants are challenging them on efficacy, dosing frequency, and administration (oral vs. injection).

1. The Heavyweights: Eli Lilly vs. Novo Nordisk

The competition has moved beyond standard GLP-1 (single-target) to multi-receptor agonists and oral formulations.

- Eli Lilly (Current Leader in Efficacy):

- Zepbound/Mounjaro (Tirzepatide): A GLP-1/GIP dual agonist. It currently holds the “gold standard” for weight loss efficacy (approx. 21–22% weight loss).

- Orforglipron (Oral): Lilly’s highly anticipated daily pill. It is expected to launch in Spring 2026 with a target price of around $399/month, significantly lower than current injectable list prices.

- Retatrutide (Triple Agonist): Targeting GLP-1, GIP, and Glucagon. Clinical data suggests weight loss exceeding 24%, potentially setting a new ceiling for the industry.

- Novo Nordisk (Defending Market Share):

- Wegovy/Ozempic (Semaglutide): Still the most recognized brand. To counter Lilly, Novo is launching its own Wegovy Pill in 2026.

- CagriSema: A combination of semaglutide and cagrilintide (an amylin analogue). It aims to match or exceed Lilly’s tirzepatide in efficacy while maintaining a strong safety profile.

- Amycretin (Oral): A co-agonist of GLP-1 and amylin. Early Phase 1 data showed 13% weight loss in just 12 weeks, which is faster than semaglutide.

2. The Disruptors: Amgen and Viking

These companies are targeting the “convenience gap” left by the weekly injections of the leaders.

- Amgen (MariTide):

- Differentiating Factor: Monthly dosing. While Wegovy and Zepbound are weekly, MariTide (AMG 133) is a bispecific GLP-1/GIPR antibody that may only require one injection per month.

- Status 2026: Mid-stage data shows ~20% weight loss. Amgen is positioning this as the premium “convenience” option for patients with “needle fatigue.”

- Viking Therapeutics (VK2735):

- The “Best-in-Class” Challenger: A dual GLP-1/GIP agonist similar to Lilly’s tirzepatide but with potentially better tolerability.

- Performance: In its Phase 2 VENTURE trial, it achieved 14.7% weight loss in just 13 weeks with no plateau observed. Viking is also fast-tracking an oral version of the same compound.

3. Comparison of Key GLP-1 Competitors (2026 Outlook)

| Drug (Company) | Target Receptors | Administration | Key Advantage | Efficacy (Weight Loss) |

| Zepbound (Lilly) | GLP-1 / GIP | Weekly SQ | Highest approved efficacy | ~21% |

| Wegovy (Novo) | GLP-1 | Weekly SQ | Longest safety track record | ~15% |

| Orforglipron (Lilly) | GLP-1 | Daily Oral | No needles, lower cost ($399) | ~15% (36 weeks) |

| MariTide (Amgen) | GLP-1 / GIPR | Monthly SQ | Less frequent dosing | ~20% (estimated) |

| VK2735 (Viking) | GLP-1 / GIP | Weekly SQ/Oral | Fast onset, good tolerability | ~15% (13 weeks) |

| Retatrutide (Lilly) | GLP-1/GIP/GCG | Weekly SQ | Potential “triple threat” | >24% |

4. 2026 Market Dynamics

- Patent Cliff & Generics: 2026 is a critical year as semaglutide (Ozempic/Wegovy) starts to lose exclusivity in markets like China, Canada, and India, which could lead to a flood of cheaper generic versions.

- Supply vs. Price: While Novo and Lilly have finally resolved most supply shortages by early 2026, the entry of oral pills and generics is putting downward pressure on prices in the US.

- New Frontiers: Competitors are now racing to prove benefits in MASH (liver disease), Sleep Apnea, and Kidney Disease to secure insurance coverage as “essential” medicine rather than “lifestyle” drugs.

Source:

- https://www.novonordisk.com/about/who-we-are/history.html

- https://www.jpmorgan.com/insights/global-research/current-events/obesity-drugs

- https://www.iqvia.com/locations/emea/blogs/2026/01/outlook-for-obesity-in-2026

- https://www.macrotrends.net/stocks/charts/NVO/novo-nordisk/revenue

- https://www.macrotrends.net/stocks/charts/NVO/novo-nordisk/stock-price-history

- https://ir.vikingtherapeutics.com/2026-02-11-Viking-Therapeutics-Reports-Fourth-Quarter-and-Year-End-2025-Financial-Results-and-Provides-Corporate-Update

- https://www.amgen.com/newsroom/press-releases/2025/06/results-from-amgens-phase-2-obesity-study-of-monthly-maritide-presented-at-the-american-diabetes-association-85th-scientific-sessions

- https://www.insightaceanalytic.com/report/glp-1-market/2592

- https://annualreport.novonordisk.com/2025/strategic-aspirations/financial-performance.html

- https://pubmed.ncbi.nlm.nih.gov/41508550/

- https://simplywall.st/stocks/us/pharmaceuticals-biotech/nyse-nvo/novo-nordisk/past

Back to Novo Nordisk page