Nestle has a rich history spanning over 150 years. Its evolution can be categorized into five distinct strategic phases:

Phase 1: Foundations and Rivalry (1866–1904)

The story began with two separate Swiss enterprises. In 1866, the Page brothers established the Anglo-Swiss Condensed Milk Company. A year later, pharmacist Henri Nestlé launched his breakthrough “farine lactée” (flour with milk) in Vevey, a specialized infant cereal that saved a neighbor’s child from malnutrition. For decades, these two companies were fierce competitors in the European milk and infant food markets.

Phase 2: Merger and the Birth of Nescafé (1905–1944)

In 1905, the two rivals merged to form the Nestlé and Anglo-Swiss Condensed Milk Company. World War I initially drove massive demand for condensed milk through government contracts, but the post-war era brought a severe economic crisis in 1921. This forced the company to diversify beyond milk-based products.

- The 1938 Breakthrough: After eight years of research to help Brazil deal with a coffee surplus, Nestlé launched Nescafé. It became an instant hit and a staple for the military during World War II, revolutionizing global coffee consumption.

Phase 3: Post-War Expansion and Acquisition (1945–1980)

Following WWII, Nestlé accelerated its growth by acquiring famous brands to move into culinary and frozen foods.

- 1947: Acquired Maggi (soups and seasonings).

- 1970s Diversification: The company stepped outside the food industry for the first time by acquiring a stake in L’Oréal (1974) and purchasing the ophthalmic leader Alcon (1977).

Phase 4: Global Consolidation (1981–2005)

Under the leadership of Helmut Maucher, Nestlé focused on high-margin acquisitions to solidify its status as the world’s largest food company.

- 1985: Acquired Carnation for 3 billion dollars, one of the largest takeovers in food history at the time.

- 1988: Bought Rowntree Mackintosh, bringing the KitKat brand into the portfolio.

- 2001: Merged with Ralston Purina, making Nestlé a global leader in the pet care sector.

Phase 5: Transition to Nutrition and Health (2006–Present)

In recent years, Nestlé has pivoted toward becoming a “Nutrition, Health and Wellness” company. This involved divesting underperforming or less “healthy” segments (like some confectionery and processed meat businesses) and investing heavily in medical nutrition.

- 2011: Founded Nestlé Health Science to target nutritional therapies for medical conditions.

- 2018: Formed a global alliance with Starbucks, paying 7.15 billion dollars for the perpetual rights to market Starbucks consumer products globally.

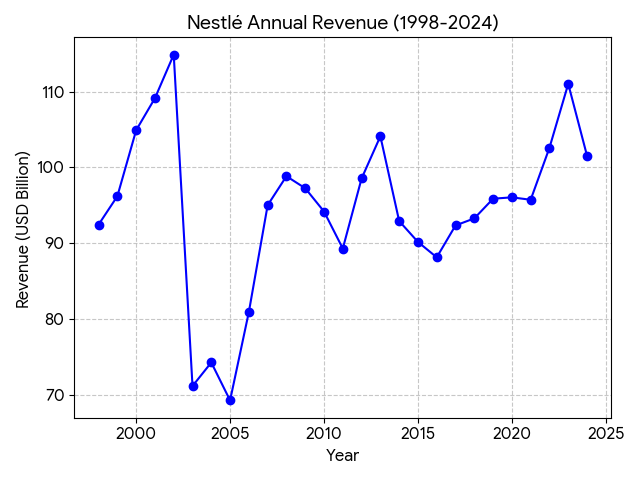

The fluctuations in Nestlé’s revenue line chart reveal a company that has shifted from chasing pure volume to prioritizing high-margin, high-growth categories. Here is a detailed breakdown of the strategic shifts that drove these changes:

1. 2000–2002: The M&A Powered Peak

The sharp incline during this period was fueled by aggressive inorganic growth.

- The Purina Acquisition (2001): Nestlé’s $10.3 billion purchase of Ralston Purina was a game-changer. It instantly made Nestlé a global leader in pet care, adding billions to the top line and creating a high-growth pillar that remains a core driver today.

- Expanding the Footprint: Rapid penetration into Eastern Europe and Asian markets further bolstered sales volumes during this era.

2. 2003–2005: Currency Headwinds and Portfolio Cleaning

The dip seen in the mid-2000s was largely technical and strategic rather than a loss of market share.

- The “Swiss Franc” Effect: Nestlé reports in CHF but earns most of its revenue in USD and EUR. During this window, the strengthening of the Swiss Franc against the Dollar led to significant negative currency translation when converting global sales back to the home currency.

- Divestment of Non-Core Assets: The company began selling off lower-margin businesses (like certain regional European food brands) to focus on more profitable segments.

3. 2011–2013: Emerging Markets and Premium Nutrition

Revenue surged past the $100B mark again due to a “Premiumization” strategy.

- The Wyeth Acquisition (2012): Nestlé paid $11.85 billion for Pfizer’s infant nutrition business (Wyeth). This was a critical move to capture the booming demand for premium baby formula in China and other emerging markets.

- Coffee Dominance: The global explosion of Nespresso and the expansion of soluble coffee in emerging economies reached a tipping point during these years.

4. 2014–2020: “Slimming Down” for Better Health

The plateau or slight decline during this period reflects a deliberate strategy to “shrink to grow.”

- Divesting the “Unhealthy”: Nestlé sold its U.S. confectionery business (including Butterfinger and BabyRuth) and parts of its Herta charcuterie business. These were low-growth, low-margin sectors that did not fit the new “Health and Wellness” mandate.

- COVID-19 Impact (2020): While “at-home” categories like Maggi and Purina thrived, the “out-of-home” sector (supplying restaurants and offices) plummeted due to global lockdowns, creating a drag on total revenue.

5. 2021–2024: Inflation-Driven Growth and Strategic Alliances

The recent recovery in revenue is largely attributed to pricing power and high-value partnerships.

- Pricing Power: In response to record-high inflation in raw materials (cocoa, coffee, and energy), Nestlé implemented significant price increases. Even as volume growth remained flat or slightly negative, higher prices pushed nominal revenue back above $100B.

- The Starbucks Alliance: The 2018 deal with Starbucks began paying off significantly during this window, as Nestlé-produced Starbucks capsules and beans became a major revenue stream in retail channels globally.

In 2026, Nestlé remains the world’s largest food and beverage company, but its competitive landscape has shifted from simple “supermarket shelf wars” to a complex battle for “share of stomach” and health outcomes. Because Nestlé is a massive conglomerate, it faces different rivals in every aisle.

1. The “Big Four” Multi-Category Rivals

Nestlé’s primary competitors are other diversified multinational corporations that possess similar global supply chains and massive R&D budgets.

| Competitor | Key Overlap | Strategic Edge (2025-2026) |

| Unilever | Ice Cream, Seasonings, Tea | Strong focus on sustainability and digital marketing; aggressive portfolio simplification. |

| PepsiCo | Beverages (RTD Coffee), Snacks | Dominance in savory snacks (Frito-Lay); leading the charge in “GLP-1 friendly” snacks. |

| Danone | Dairy, Bottled Water, Infant Nutrition | Global leader in plant-based dairy and specialized medical nutrition. |

| Mars | Pet Care, Snacking/Confectionery | Private ownership allows for long-term investments; vertical integration in pet veterinary clinics. |

2. Vertical Competition by Category

Coffee (The Growth Engine)

- Main Rivals: JAB Holding Company (Peet’s, Keurig, Caribou), Starbucks, and Lavazza.

- Dynamics: While Nestlé transformed its biggest rival, Starbucks, into a partner via the Global Coffee Alliance, it faces intense pressure from JAB-owned brands in the North American pod market (Keurig) and high-end specialty roasters globally.

Pet Care (The Profit Pillar)

- Main Rivals: Mars Petcare, General Mills (Blue Buffalo), and Colgate-Palmolive (Hill’s Science Diet).

- Dynamics: This is Nestlé’s highest-margin segment. While Purina focuses on “science-based” nutrition, Mars has built a defensive moat by acquiring thousands of veterinary clinics (VCA, Banfield), creating a closed ecosystem that Nestlé lacks.

Infant & Medical Nutrition

- Main Rivals: Abbott Laboratories, Reckitt (Mead Johnson), and Danone.

- Dynamics: In 2026, the battleground has shifted to China and Southeast Asia. Nestlé is currently fighting “local-first” sentiment in China (against brands like Feihe) while pivoting toward Metabolic Health products to counter rivals like Abbott.

3. Emerging Threats in 2026

- The GLP-1 “Ozempic” Effect: The rise of weight-loss drugs has structurally lowered caloric intake in developed markets. Nestlé is racing to launch “companion products” (high-protein, nutrient-dense portions) to prevent revenue loss from consumers skipping snacks.

- Private Labels (Store Brands): As inflation persists, retailers like Walmart and Amazon are expanding their premium “private label” offerings. These products often mimic Nestlé’s quality but at a 20-30% lower price point, eroding Nestlé’s middle-market share.

- The “Clean Label” Movement: Smaller, agile “challenger brands” are stealing market share by offering shorter ingredient lists and plastic-free packaging, forcing Nestlé to spend billions on reformulating legacy products.

In 2026, the beverage sector remains Nestlé’s largest and most profitable business unit. The competitive landscape has evolved from a simple volume game into a high-tech battle focused on premiumization, functional health, and closed ecosystems.

Nestlé’s beverage strategy centers on a “Power Trio”: Coffee, Water, and Functional Drinks.

1. The Global Coffee War: A Two-Front Battle

Coffee is Nestlé’s “crown jewel,” but it faces distinct rivals in different sub-segments.

- The System Lock-In (Pods/Capsules):

- Main Rival: JAB Holding Company (Keurig, JDE Peet’s).

- Strategy: Nestlé uses Nespresso to dominate the ultra-premium segment. To counter the threat of third-party compatible pods, Nestlé introduced the Vertuo system, which uses centrifugal technology and barcoded capsules to create a new “closed” ecosystem that is harder for rivals to replicate.

- The Retail Powerhouse:

- Main Rival: Starbucks (Partner) vs. Coca-Cola (Costa Coffee).

- Strategy: Through the Global Coffee Alliance, Nestlé pays royalties to sell Starbucks-branded products in supermarkets. This effectively prevents Starbucks from becoming a direct retail competitor while using their brand prestige to block out mid-tier rivals like Costa Coffee (owned by Coca-Cola).

2. Ready-to-Drink (RTD) and Functional Beverages

This is the fastest-growing sub-segment in 2026, driven by convenience and health-conscious consumers.

- Main Rivals: Coca-Cola, PepsiCo, and Suntory.

- The “GLP-1” Shift: With the rise of weight-loss medications (like Ozempic), consumers are drinking fewer sugary sodas. Nestlé is pivoting its beverage portfolio toward “Companion Drinks”—RTD beverages fortified with protein, fiber, and electrolytes under the Nestlé Health Science umbrella to cater to this new demographic.

- Cold Brew Dominance: While Coca-Cola leads in traditional sodas, Nestlé is winning in Cold Brew and Nitro-Coffee RTD formats, which are perceived as more premium and “natural.”

3. High-End Water Strategy

After divesting its mass-market North American water brands (like Poland Spring) a few years ago, Nestlé now focuses purely on the high-margin “Premium Water” segment.

- Main Rival: Danone (Evian, Volvic).

- Competitive Edge: Nestlé controls the world’s most recognizable sparkling water brands: Perrier and S.Pellegrino. In 2026, the competition has shifted to sustainability-led premiumization. Nestlé is investing heavily in “deforestation-free” supply chains and recycled PET (rPET) to justify the premium price tags and maintain its lead over Danone’s mineral water portfolio.

4. 2026 Strategic Summary: The Tech Edge

What separates Nestlé from its beverage rivals in 2026 is its Deep Tech Center in Switzerland. This allows Nestlé to:

- AI-Driven Flavor Profiling: Predict hyper-local taste trends (e.g., specific plant-milk pairings in Southeast Asia) faster than PepsiCo or Coca-Cola.

- Bio-Transformation: Using proprietary fermentation to reduce sugar in beverages without using artificial sweeteners, a major competitive advantage as “Clean Label” laws tighten.

Competitive Benchmarking (2025-2026 Estimate)

| Feature | Nestlé | Coca-Cola | JAB Holding |

| Market Share (Coffee) | Leader (~22%) | Challenger | Runner-up (~24% in Instant) |

| Sustainability Rating | High (rPET focus) | Moderate (Scale issues) | Moderate |

| Health Alignment | Very High | Moderate (Soda heavy) | Low (Pure Coffee) |

| Pricing Power | Premium / Luxury | Mass / Mid-Market | Mass / Value |

In 2026, the PetCare segment (led by the Purina brand) is the powerhouse of Nestlé’s growth, contributing over 20% of total revenue and maintaining industry-leading margins. The market has matured into a sophisticated “duopoly” between Nestlé and Mars, but the two are moving in different strategic directions.

1. The Titan Clash: Nestlé Purina vs. Mars Petcare

As of 2024–2025, both companies reported annual pet care revenues of approximately $22 billion, effectively splitting nearly 50% of the global market.

| Feature | Nestlé Purina | Mars Petcare |

| Market Share (2025) | ~32% (Slightly leads in U.S. sales) | ~30% (Globally dominant) |

| Strategic Edge | R&D & Science: Leads in “Functional Nutrition” (e.g., Pro Plan). | Vertical Integration: Owns thousands of vet clinics (VCA, Banfield). |

| Channel Strength | Massive dominance in Supermarkets & E-commerce. | Strongest in Veterinary & Specialty channels. |

| Key Brands | Pro Plan, Purina ONE, Fancy Feast, Felix. | Royal Canin, Pedigree, Whiskas, Iams. |

2. Segment-Specific Dominance

A. Cat Food: Nestlé’s Fortress

Nestlé is the undisputed leader in the cat food category, particularly in wet food.

- Market Share: In 2025, Nestlé commanded over 76% of the “economy wet” cat food segment and is the leader in premium brands like Fancy Feast and Gourmet.

- Competitive Moat: Cats are notoriously picky; Nestlé’s flavor science and “palatability” research give it a significant edge over Mars and General Mills in feline nutrition.

B. Therapeutic & Science Diets

- Main Rival: Hill’s Pet Nutrition (Colgate-Palmolive).

- Current Status: While Hill’s is the traditional leader in “Vet-Prescribed” diets, Purina Pro Plan has successfully bridged the gap between retail and clinical. By adding claims like “probiotics for anxiety” or “allergen-reducing food” (LiveClear), Nestlé is capturing the “Pro-sumer” pet owner who wants medical-grade food without a prescription.

C. The “Fresh & Raw” Challenge

- Main Rivals: Freshpet, The Farmer’s Dog.

- The 2026 Shift: Smaller, agile brands are growing at double-digit rates by offering human-grade, refrigerated meals. Nestlé is responding by investing in “Gently Cooked” technology and cold-chain logistics to prevent these “challenger brands” from stealing the premium dog food market.

3. Emerging Trends & Threats in 2026

- The “Ozempic” for Pets: As pet obesity becomes a global crisis, Nestlé is launching metabolic-regulating diets. The competition here is no longer just about “taste” but about clinical outcomes.

- Sustainability & “Green” Proteins: In 2026, the carbon footprint of meat-based pet food is under scrutiny. Nestlé is ahead of Mars in testing insect-based proteins and lab-grown meat alternatives in European markets (e.g., Purina Beyond Nature’s Protein).

- Private Label Pressure: Retail giants like Amazon (Wag) and Walmart are improving their “Premium” private labels. These brands now compete on innovation (grain-free, high-protein) rather than just price, forcing Nestlé to spend more on marketing to justify its brand premium.

Strategic Summary: Why Nestlé Wins

While Mars wins by owning the doctor (vets), Nestlé wins by owning the science (R&D). Nestlé performs over 100,000 quality checks daily and leverages its global R&D network to launch products faster than its competitors.

Source:

- https://me.factory.nestle.com/sites/g/files/pydnoa581/files/2023-11/nestle-company-history-timeline.pdf

- https://www.nestle.com/sites/default/files/2025-02/annual-review-2024-en.pdf

- https://www.nestle.com/sites/default/files/2025-02/full-year-results-investor-presentation-2024.pdf

- https://www.nestle.com/investors/annual-report

- https://www.fortunebusinessinsights.com/wet-pet-food-market-115012

- https://www.mordorintelligence.com/industry-reports/pet-care-market

- https://www.futuremarketinsights.com/reports/south-asia-pet-care-market

- https://www.stellarmr.com/report/pet-food-market/2713

- https://pestel-analysis.com/blogs/competitors/nestle

- https://www.englishteastore.com/pages/history-of-nestle

Back to Nestle page