Linde History: Key Evolutionary Stages

Linde plc is currently the world’s largest industrial gas company. Its history is a 140-year journey of engineering excellence, strategic mergers, and market dominance. Here are the four defining stages:

Phase 1: Innovation and Cryogenic Breakthroughs (1879–1914)

The company was founded in 1879 by Carl von Linde in Germany as Gesellschaft für Linde’s Eismaschinen AG. This era was defined by pioneering thermodynamics.

- 1870s: Carl von Linde developed an improved ammonia compressor, revolutionizing refrigeration for breweries and food storage.

- 1895: He achieved a massive scientific breakthrough by liquefying air (the Linde process).

- 1902: The development of a technique to fractionate liquefied air allowed for the industrial production of pure oxygen and nitrogen, birth of the industrial gas industry.

Phase 2: Post-War Recovery and Diversification (1914–1990s)

World War I and II resulted in the loss of many foreign patents and subsidiaries (notably in the US), but the post-war era saw Linde rebuild as a global engineering powerhouse.

- Reconstruction: After 1945, Linde focused on rebuilding its international presence and recovering seized assets.

- Expansion: The company diversified into materials handling (forklifts) and large-scale plant engineering, becoming a critical supplier to the steel, chemical, and aerospace industries.

- Global Reach: Linde established itself as a leader in European and emerging markets during the industrial boom of the 60s and 70s.

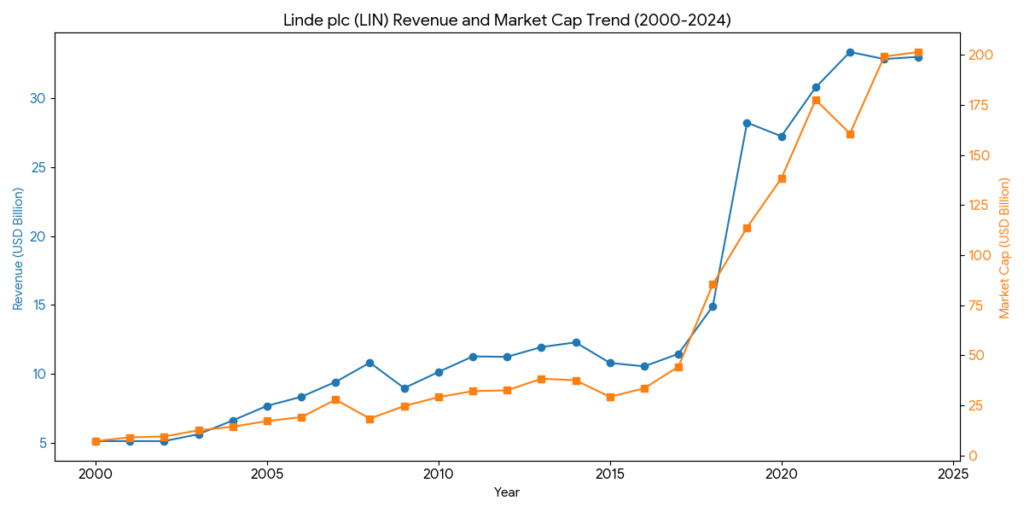

Phase 3: Strategic Acquisitions and Consolidation (2000–2017)

To maintain its lead against rising competitors like Air Liquide, Linde shifted from organic growth to aggressive, large-scale acquisitions.

- 2000: Acquired the Swedish gas company AGA, strengthening its position in Northern Europe and the Americas.

- 2006: Acquired the British BOC Group for approximately £8 billion. This was a transformative deal that made Linde the global market leader at the time.

- Pure-Play Focus: To focus on gases and engineering, Linde spun off its material handling division (now KION Group) in 2006.

Phase 4: The Praxair Merger and Green Energy (2018–Present)

This phase marks the creation of the modern Linde plc and its pivot toward the energy transition.

- 2018: Linde AG merged with the American company Praxair in a $90 billion “merger of equals.” This created a dominant global entity with a massive footprint in both Europe and the Americas.

- The Hydrogen Era: Linde is now a leader in the “Hydrogen Economy,” investing heavily in green hydrogen production, distribution, and carbon capture technologies.

- Stock Market Pivot: In 2023, the company delisted from the Frankfurt Stock Exchange to simplify its structure, maintaining its primary listing on the NYSE.

Competitive Landscape Analysis

Linde plc operates in a highly consolidated global market characterized by high entry barriers due to massive capital requirements and long-term contract structures. The industry is currently defined by the “Big Three” global players.

1. Market Share and Key Competitors

As of early 2026, the industrial gas market remains an oligopoly. Linde maintains the top spot, followed by Air Liquide and Air Products.

| Competitor | Market Share (Est.) | Core Strategic Focus |

| Linde plc | ~28-30% | Operational efficiency, global scale, and integrated engineering/gas solutions. |

| Air Liquide | ~22-24% | Strong focus on Home Healthcare, Electronics, and deep European pipeline networks. |

| Air Products | ~12-15% | High-risk/high-reward strategy focusing on massive blue/green hydrogen energy projects. |

| Nippon Sanso | ~7-9% | Dominance in Japan and specialized focus on the semiconductor sector in Asia. |

2. Strategic Benchmarking

A. The Hydrogen Race (Energy Transition)

- Linde: Focuses on the entire value chain. They produce, liquefy, and distribute hydrogen while also manufacturing the equipment (electrolyzers and fueling stations). Linde’s approach is “infrastructure-first,” leveraging its existing distribution network.

- Air Products: Pursues a “Producer-First” model. They are investing tens of billions into world-scale green hydrogen production (e.g., NEOM in Saudi Arabia). Their goal is to be the lowest-cost producer of clean hydrogen molecules globally.

- Air Liquide: Emphasizes industrial decarbonization. They partner with heavy industries (steel, cement) to capture carbon and replace fossil fuels with hydrogen, particularly in Europe.

B. Semiconductor & Electronics

- Linde: Leverages its global footprint to support the geographic diversification of chipmakers (e.g., supporting new fabs in the US, Germany, and Taiwan).

- Nippon Sanso: This is their “home turf.” They are highly competitive in providing specialty gases and extreme-purity equipment required for advanced node manufacturing.

C. Operational Efficiency

- Linde: Consistently reports the highest operating margins in the industry. Post-Praxair merger, Linde’s management has been ruthless in cost-cutting and optimizing “price over volume,” leading to superior Return on Capital Employed (ROCE).

- Air Products: Recently faced investor pressure regarding its massive capital expenditure (CapEx) on hydrogen, leading to a focus on rebalancing its portfolio to protect near-term cash flows.

3. SWOT Summary for Linde vs. Peers

- Strengths: Unrivaled scale, superior pricing power, and a world-class engineering division (Linde Engineering) that builds the very plants their gas business operates.

- Weaknesses: Regulatory scrutiny. Because of their size, further large-scale M&A is nearly impossible in most jurisdictions.

- Opportunities: Transitioning traditional gray hydrogen customers to blue or green hydrogen at premium margins.

- Threats: Regional players (like those in China) gaining scale and competing on price in emerging markets.

Sources: https://www.linde.com/about-linde/history

Back to Linde page