The history of Inditex (Industria de Diseño Textil, S.A.) is a masterclass in supply chain efficiency and retail strategy. Its evolution can be broken down into five distinct phases:

1. The Workshop & Retail Inception (1963–1984)

This period focused on the transition from manufacturing to direct retail.

- 1963: Amancio Ortega Gaona starts Confecciones GOA in A Coruña, Spain, making bathrobes and quilted housecoats.

- 1975: The first Zara store opens in downtown A Coruña. Originally intended to be named “Zorba,” the name was changed to Zara due to a nearby bar already using the name.

- 1984: Investment in computerized logistics begins, setting the stage for the “Just-in-Time” manufacturing model.

2. Corporate Formation & Brand Diversification (1985–2000)

Inditex was established as a holding company to manage a growing portfolio of brands targeting different demographics.

- 1985: Inditex is officially founded.

- 1988–1990: International expansion begins with stores in Porto (Portugal), New York (USA), and Paris (France).

- 1991: Launch of Pull&Bear and the acquisition of 65% of Massimo Dutti.

- 1998: Launch of Bershka, targeting the urban youth market.

- 1999: Acquisition of Stradivarius.

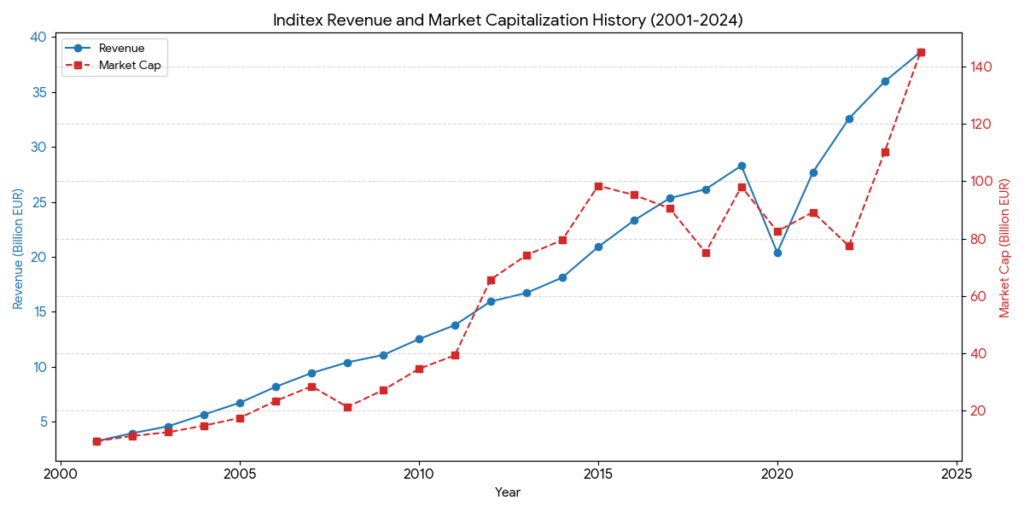

3. IPO & Global Dominance (2001–2009)

Public listing provided the capital for massive global physical expansion.

- 2001: Inditex goes public on the Madrid Stock Exchange (IPO). In the same year, Oysho (lingerie) is launched.

- 2003: Zara Home is launched, entering the interior design market.

- 2004: The group hits a milestone of 2,000 stores worldwide, opening in its 50th country (Hong Kong).

4. Digital Transformation & RFID Integration (2010–2020)

As e-commerce rose, Inditex focused on “Omnichannel” retailing—merging physical and digital inventories.

- 2010: Zara launches its online shop, followed by other brands in the group.

- 2011: Pablo Isla becomes Chairman and CEO, succeeding Ortega.

- 2014: Full rollout of RFID (Radio Frequency Identification) technology, allowing real-time tracking of every garment from the logistics center to the sale point.

- 2018: Commitment that all brands will be available online globally by 2020.

5. Leadership Transition & Sustainability Era (2021–Present)

The current phase focuses on generational leadership and environmental responsibility.

- 2021–2022: Marta Ortega Pérez (daughter of the founder) takes over as Chairwoman, with Óscar García Maceiras as CEO.

- 2023: Launch of “Zara Pre-Owned” (resale/repair platform) to promote a circular economy.

- 2024–2025: Massive investment in logistics (Project Horizon) and a goal to use 100% “preferred” (more sustainable) textile fibers by 2030.

In the 2026 global apparel landscape, Inditex maintains its leadership through a “Premium Fast Fashion” strategy, distancing itself from the race-to-the-bottom pricing while fending off ultra-low-cost disruptors.

1. Competitive Landscape Comparison (2025-2026 Estimates)

| Group / Brand | Core Strategy | Competitive Advantage | Revenue (Est. B) | Operating Margin |

| Inditex (Zara) | Premiumization | Near-shore production, RFID logistics | ~€38.5B | ~18-20% |

| Shein | Ultra-Fast Fashion | Big-data demand sensing, micro-batching | ~$50B+ | ~5-8% |

| Fast Retailing | LifeWear | Textile R&D (Heattech), basic essentials | ~¥3.1T | ~12-14% |

| H&M Group | Value & Sustainability | Broad market reach, circular economy focus | ~SEK 235B | ~7-9% |

2. Strategic Benchmarking: The “Four Pillars” of Competition

A. Speed vs. Volume: Inditex vs. Shein

While Shein wins on volume (uploading thousands of SKUs daily), Inditex wins on relevance and quality.

- The Shein Model: Fully digital, targeting Gen Z with $10 items. It uses a “Real-time Retail” model where algorithms dictate production.

- The Inditex Response: Focusing on “High-Street Premium.” Zara has moved upmarket, increasing average selling prices (ASP) by over 10% since 2023. By offering “runway-inspired” quality at a higher tier than Shein, they avoid direct price wars.

B. Logistics Efficiency: Near-shoring vs. Off-shoring

- Inditex’s Secret: Over 50% of production happens in Spain, Portugal, Morocco, and Turkey. This allows a 2-to-3 week turnaround from design to store floor.

- Competitor Lag: H&M and Gap rely heavily on Asian manufacturing (80%+). While cheaper, it leaves them vulnerable to shipping delays and forces them to commit to trends months in advance, often leading to unsold inventory and heavy discounting.

C. Tech Integration: The “Phygital” Store

Inditex is outspending rivals on store technology.

- RFID & AI: Every garment is tracked globally. If a blazer is sold in Paris, the system immediately knows if a replacement is needed from a nearby store or the central hub.

- Uniqlo’s Threat: Uniqlo is the only rival matching Inditex’s tech efficiency with their self-checkout and specialized fabric R&D, capturing the “functional” segment that Zara lacks.

3. Current Market Outlook (2026)

Inditex currently holds approximately 2.5% of the fragmented global fashion market. Analysts suggest its “moat” is no longer just speed, but its Integrated Store and Online Platform.

- Financial Resilience: As of early 2026, Inditex maintains a net cash position of over €11B, allowing it to invest in massive “Mega-stores” while H&M and other retailers are forced to close smaller, unprofitable locations.

- Sustainability Barrier: New EU regulations (ESPR) regarding textile waste favor Inditex’s “Zara Pre-Owned” and “Circular Hub” initiatives, which are significantly more advanced than Shein’s current environmental compliance.

Sources:

- BoF: The State of Fashion 2026 Report

- Reuters: Inditex Financial Strategy Analysis

- Morgan Stanley: Retail Sector Equity Research 2026

Back to Inditex page