Here is the historical development of China Mobile categorized into key stages:

Phase 1: Industry Incubation and Corporatization (1987–1999)

- Core Products: 1G analog cellular services, 2G GSM voice.

- Core Strategy: Separation of government functions from enterprise operations. Decoupling mobile services from the original China Telecom to establish a modern corporate system and list on international markets.

- Revenue Level: Startup growth phase. The 1997 IPO in Hong Kong and New York raised approximately $4.2 billion, a record for Chinese enterprises at the time.

Phase 2: Scale Expansion and Branding (2000–2008)

- Core Products: Mobile voice, SMS (Short Message Service), and “Monternet” (WAP) value-added services.

- Core Strategy: “Scale Leads the Way.” Established three distinct brands—GoTone, M-Zone, and Easyown—to target different market segments. Integrated provincial assets to achieve unified nationwide operations.

- Revenue Level: Golden growth era. Revenue jumped from the 100 billion RMB level to over 300 billion RMB. Profitability was high, with EBITDA margins often exceeding 50%.

Phase 3: Technological Leap and Data-Centric Shift (2009–2018)

- Core Products: 3G/4G data plans, smartphone terminals, and VoLTE (Voice over LTE).

- Core Strategy: Transitioning from voice to data. While 3G (TD-SCDMA) was a period of technological transition, the 4G (TD-LTE) era saw China Mobile leverage a first-mover advantage to build the world’s largest 4G network.

- Revenue Level: Steady expansion. Annual revenue surpassed 700 billion RMB. However, traditional SMS and voice revenue began to decline due to the rise of OTT apps like WeChat.

Phase 4: Digital Transformation and Computing Power (2019–Present)

- Core Products: 5G packages, Mobile Cloud, Smart Home solutions (HBN), and industrial internet applications.

- Core Strategy: “Connection + Computing Power + Capability.” Focusing on the CHBN (Customer, Home, Business, New Market) strategy to transform from a traditional carrier into a digital infrastructure and intelligence service provider.

- Revenue Level: The “Trillion-Yuan” Era. Total revenue exceeded 1 trillion RMB in 2023. By 2025, digital transformation revenue (Cloud, AI, Big Data) accounted for over one-third of total service revenue.

Key Financial Metrics (As of Mid-2025)

- Operating Revenue: 543.8 billion RMB (H1 2025).

- Net Profit: 84.2 billion RMB (5.0% YoY growth).

- Dividend Policy: The dividend payout ratio is expected to reach 75% or higher for the 2024-2026 period.

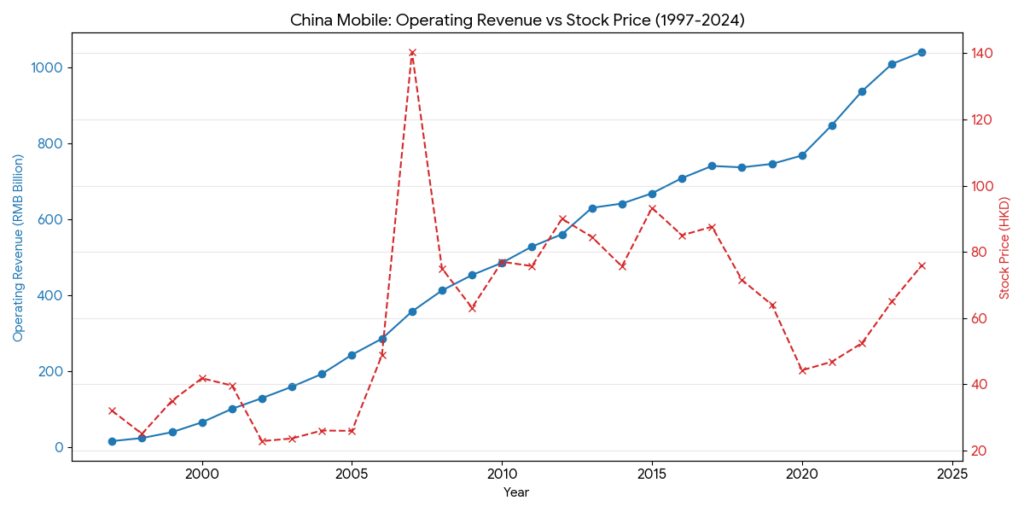

China Mobile: Historical Revenue vs. Stock Price (1997-2024)

In this chart analysis, the blue solid line represents the annual operating revenue (in RMB Billion), reflecting the company’s scale expansion from the voice era to the data era. The red dashed line represents the year-end closing price of its Hong Kong stock (0941.HK) (in HKD), showing the fluctuations in the capital market’s valuation of the company.

Looking at the data trends, China Mobile’s revenue has maintained an almost uninterrupted growth trend over the past 27 years. In particular, after the issuance of 4G licenses in 2013 and the launch of commercial 5G in 2019, the revenue scale reached new milestones, officially surpassing the 1 trillion RMB mark in 2023. Regarding the stock price, 2007 marked a historical peak driven by explosive growth in mobile subscribers and capital market enthusiasm. Subsequent fluctuations reflect intensifying competition in the telecom industry, “speed upgrade and tariff reduction” policies, and the value recovery following its delisting from the US market in recent years.

Competitive Landscape of China’s Telecom Industry

| Dimension | China Mobile (0941.HK) | China Telecom (0728.HK) | China Unicom (0762.HK) |

| Market Position | Absolute Leader. Over 1 billion mobile users; world’s largest 5G subscriber base. | Steady Runner-up. Strong foundation in fixed-line and government/enterprise sectors. | Agile Challenger. Leader in network sharing; focused on innovation and efficiency. |

| Core Strength | Massive capital reserves and base station coverage; first-mover advantage in 4G/5G. | Leading Cloud computing (IDC) capabilities and fiber-optic dominance. | Flexibility from mixed-ownership reform; asset-light operational transformation. |

| 5G Strategy | Leading in 5.5G (5G-A) deployment; owns premium frequency spectrum. | “Co-build and Share” with Unicom to reduce Capex pressure. | Focuses on Industrial Internet and vertical industry integration. |

| Digital Pivot | Mobile Cloud: Growing rapidly, revenue reaching the 100-billion RMB level. | e-Surfing Cloud: Top public cloud share among telcos; dominant in Gov-cloud. | Unicom Cloud: Focuses on Big Data and AI-driven industry empowerment. |

In-Depth Analysis of Core Competencies

1. Consumer & Home Markets (C/H Segments)

- China Mobile: Leveraging its massive user base, its 5G penetration has surpassed 60%. In the home market, its “Mobile Love Home” brand utilizes economies of scale to squeeze competitors’ growth space in broadband.

- Trend: As the mobile market reaches saturation, competition has shifted from “User Acquisition” to ARPU (Average Revenue Per User) preservation and churn reduction.

2. Business & Digital Transformation (B-End) — The Primary Battlefield

This is the “Second Growth Curve” for all three players:

- China Telecom (e-Surfing Cloud): The earliest mover in cloud computing among telcos. It holds the strongest IDC infrastructure and leads the market in government, education, and healthcare cloud services.

- China Mobile (Mobile Cloud): Despite a later start, its aggressive investment and massive sales channel have led to triple-digit growth rates, rapidly narrowing the gap with China Telecom.

- China Unicom: While smaller in scale, it excels in Internet of Things (IoT) and Big Data analytics, specializing in customized industrial solutions.

3. Technological R&D and AI Computing Power

- Computing Power Network: China Mobile is pivoting toward a “Computing Power Network,” building intelligent computing centers nationwide. As of 2025, its computing scale leads the industry, aiming to be the infrastructure provider for the AI era.

- 5G-Advanced (5.5G): China Mobile is the fastest in standard-setting and pilot city construction, with large-scale commercialization expected in 2026, further widening the technical gap with its peers.

Financial Strength & Shareholder Returns (2025-2026 Outlook)

- Capital Expenditure (CAPEX): With the peak of 5G construction passed, CAPEX for all three operators is declining, leading to significantly improved free cash flow.

- Dividend Policy: To attract long-term investors, all three have committed to high payout ratios:

- China Mobile: Payout ratio expected to stay at 75% or higher, making it a classic “high-yield, low-volatility” blue-chip stock.

- China Telecom/Unicom: Payout ratios have also generally increased to around 70%, serving as a top choice for defensive, yield-seeking portfolios.

Summary

China Mobile remains the “Aircraft Carrier” of the industry with the strongest financial resilience and network coverage. China Telecom possesses a structural advantage in Gov-cloud and fixed-line integration, while China Unicom shows high potential for marginal improvement through leaner operations.

Sources:

China Mobile Official – 2025 Interim Results

Futu News: Analysis of China Mobile’s Digital Transformation

Back to China Mobile page