Here is the history of Bank of America divided into key stages:

1.Founding and the People’s Bank (1904-1920s)

- 1904: Amadeo P. Giannini founded the Bank of Italy in San Francisco. His goal was to serve the little fellow—immigrants and small businesses ignored by traditional banks.

- 1906: After the Great San Francisco Earthquake, Giannini famously set up a temporary desk on the wharf to provide loans to residents when other banks were paralyzed.

- 1920s: Giannini pioneered the branch banking system, allowing the bank to spread across California and provide consistent service to rural areas.

Key Business Development: Introduction of Mass-Market Retail Banking. Giannini revolutionized the industry by actively marketing to the “little fellow.” He established the first statewide branch banking system in the U.S., which allowed the bank to diversify its risk across different local economies (e.g., farming, fishing, and manufacturing).

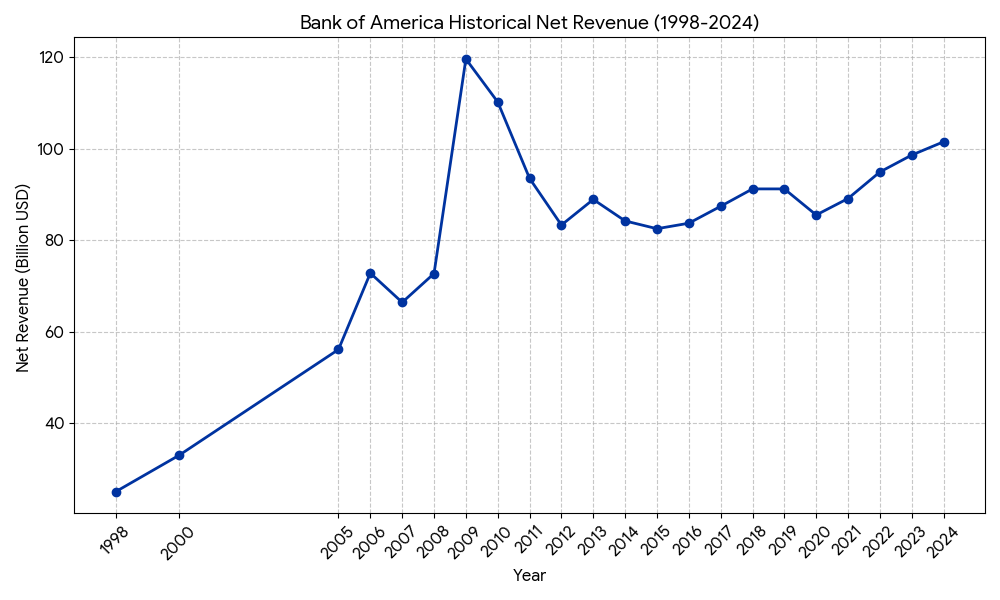

Revenue/Financial Level: By 1920, assets reached approximately 150 million USD. By 1929, the Bank of Italy and its affiliates had total assets exceeding 1 billion USD, making it a dominant force on the West Coast before the official name change.

2.Consolidation and the Birth of Visa (1928-1950s)

- 1928: Giannini merged his bank with Bank of America, Los Angeles.

- 1930: The institution was officially renamed Bank of America National Trust and Savings Association.

- 1945: By the end of WWII, it became the largest commercial bank in the world.

- 1958: The bank launched the BankAmericard, which was the first successful revolving credit card. This system eventually evolved into the global Visa network in 1976.

Key Business Development: The Revolving Credit Model. In 1958, the bank launched the BankAmericard. Unlike previous cards that required full monthly payment, this allowed users to carry a balance. This shifted the business model from pure interest on loans to a high-volume fee and interest model from consumer spending.

Revenue/Financial Level: By the late 1980s, annual revenue was in the 5 billion USD to 8 billion USD range. After the 1992 merger with Security Pacific, revenues jumped toward 10 billion USD.

3.Expansion and Nationwide Mergers (1960s-1990s)

- 1983: The bank expanded outside California for the first time by acquiring Seafirst Corporation in Washington.

- 1992: It merged with Security Pacific Corporation, marking one of the largest bank mergers in history at the time.

- 1998: NationsBank, led by Hugh McColl and based in North Carolina, acquired Bank of America. Despite NationsBank being the survivor, they kept the Bank of America name and moved the headquarters to Charlotte, North Carolina.

Key Business Development: Universal Banking Integration. The 1998 merger with NationsBank created the first coast-to-coast bank in the U.S. The subsequent 2008-2009 acquisitions of Merrill Lynch and Countrywide Financial transformed the bank into a “financial supermarket,” offering retail banking, mortgage lending, and global investment banking under one roof.

Revenue/Financial Level: * 2006 (Pre-Crisis): Revenue was approximately 73 billion USD with a net income of 21 billion USD.

- 2009 (Peak of Crisis): Total revenue surged to 119 billion USD due to the Merrill Lynch acquisition, but net income plummeted to 6.3 billion USD (and a loss for common shareholders) due to toxic mortgage assets.

4.Crisis Management and Modern Era (2000s-Present)

- 2004-2006: The bank acquired FleetBoston Financial and MBNA, becoming a leader in both retail banking and credit cards.

- 2008: Amidst the Global Financial Crisis, BofA acquired the subprime lender Countrywide Financial and the investment giant Merrill Lynch. While Merrill Lynch made BofA a powerhouse in wealth management, the Countrywide acquisition led to years of legal challenges.

- 2010s-2020s: The bank shifted focus to digital transformation, launching its AI assistant Erica and expanding its mobile banking platform to millions of users.

Key Business Development: Operating Leverage & Digital Adoption. Under Brian Moynihan, the bank executed “Project New Bac,” cutting billions in annual expenses. It pivoted to digital-first banking (Erica AI) and leveraged Merrill Lynch to become a global leader in Wealth Management, which provides more stable fee-based income compared to volatile trading.

Revenue/Financial Level: * 2024: Annual revenue surpassed 101 billion USD, with net income stabilizing at 26.5 billion USD.

- 2025: Revenue remains strong at approximately 102 billion USD, with over 59 million active digital users driving down the cost of transactions.