The history of Airbus is a remarkable saga of European industrial integration, evolving from a consortium designed to challenge the American dominance of Boeing and McDonnell Douglas into the world’s leading commercial aircraft manufacturer. Its history can be categorized into several key stages:

1. Foundation and Early Struggles (Late 1960s – 1970s): Breaking the Monopoly

The primary goal during this period was to establish a European alternative to U.S.-made aircraft.

- The Birth of Collaboration: In 1967, the governments of France, Germany, and the UK signed a Memorandum of Understanding to develop a short-to-medium range, wide-body, twin-engine jet. In 1970, Airbus Industrie was formally established in Toulouse, France, as a “Groupement d’Intérêt Économique” (GIE).

- The A300 Landmark: In 1972, the A300B—the world’s first twin-engine wide-body aircraft—made its first flight. Despite slow initial sales, its fuel efficiency eventually won over the market, especially after a breakthrough order from Eastern Airlines in 1977, which opened the door to the U.S. market.

2. Technological Revolution (Late 1970s – 1980s): Digital Innovation

Airbus began to differentiate itself through cutting-edge technology, cementing its competitive edge.

- The A310 Evolution: Launched in 1978, the A310 was a shorter version of the A300 but featured higher range and the first digital flight deck for a wide-body aircraft.

- The A320 and Fly-By-Wire: Launched in 1984, the A320 series became one of the most successful aircraft families in history. It pioneered Fly-By-Wire (FBW) technology and side-stick controllers in commercial aviation, replacing traditional mechanical linkages and setting the standard for all future Airbus cockpits.

3. Full Market Expansion (1990s): Completing the Family

Airbus expanded its product line to cover all market segments, from narrow-body to long-haul wide-body jets.

- A330 & A340 Partnership: Launched simultaneously in 1987 to target medium-to-long-range markets. By sharing the same wing and fuselage design, Airbus drastically reduced development costs while offering airlines a choice between two engines (A330) or four (A340).

- Corporate Restructuring: In 2001, Airbus transitioned from a loose consortium to a single integrated company (Airbus SAS), majority-owned by EADS (now Airbus Group), which significantly improved operational efficiency.

4. The Giant and Composite Era (2000s – 2015): Challenging Limits

This era saw the birth of the largest passenger aircraft ever built and a shift toward extreme fuel efficiency.

- The A380 “Superjumbo”: To directly challenge the Boeing 747, Airbus developed the full double-deck A380. While a technical masterpiece, the market shifted toward “point-to-point” flying rather than “hub-and-spoke,” and the four-engine design became less economical. Production eventually ended in 2021.

- The A350 XWB: Responding to the Boeing 787, Airbus developed the A350, utilizing over 50% composite materials (carbon fiber reinforced polymer) to drastically reduce weight and fuel consumption.

5. Sustainability and the Digital Future (2016 – Present): The Decarbonization Goal

Airbus is currently leading the charge toward a zero-emission aviation industry.

- A320neo Dominance: By introducing the “New Engine Option” (neo), the A320 family became the fastest-selling aircraft in history due to its 15–20% improvement in fuel efficiency.

- ZEROe Project: In 2020, Airbus unveiled three concepts for the world’s first zero-emission commercial aircraft powered by hydrogen, aiming for entry into service by 2035.

The competitive landscape between Airbus and Boeing in 2026 has evolved into a battle of “Production Stability” versus “Order Recovery.” While Airbus maintains a lead in total deliveries and backlog, Boeing has shown significant signs of a turnaround.

1. Key Performance Metrics (2025 – Early 2026)

The gap between the two giants is narrowing in terms of sales momentum, though Airbus still holds the crown for industrial output.

| Metric | Airbus | Boeing | Competitive Insight |

| 2025 Deliveries | 793 units | 600 units | Airbus leads in supply chain execution. |

| 2025 Net Orders | 889 units | 1,173 units | Boeing won the “Order War” for the first time since 2018. |

| Jan 2026 Deliveries | 19 units | 46 units | Boeing’s early 2026 surge shows production lines are stabilizing. |

| Backlog | ~8,754 units | ~6,000+ units | Airbus has a more secured long-term revenue stream. |

2. Narrow-body Battle: A320neo vs. 737 MAX

This remains the most profitable sector, currently defined by the dominance of the A321neo.

- The A321neo Hegemony: The A321neo (specifically the A321XLR) has virtually no direct competitor in the “Middle of the Market” segment. It offers long-range capabilities with narrow-body economics. Airbus is pushing to reach a production rate of 75 aircraft per month by 2027.

- 737 MAX Recovery: Boeing is aggressively clearing its inventory and aiming to deliver 500 MAX jets in 2026. While it lacks a direct rival to the A321XLR’s range, the 737 MAX 8 remains a workhorse for low-cost carriers globally.

3. Wide-body Strategy: A350/A330neo vs. 787/777X

Boeing historically dominates this segment, and it remains their strongest counter-attack point.

- Boeing’s Wide-body Lead: In 2025, Boeing delivered 153 wide-body aircraft compared to Airbus’s 93. The 787 Dreamliner continues to be the preferred choice for long-haul efficiency, and the certification progress of the 777X is the most watched milestone for 2026.

- Airbus’s Response: Airbus is focusing on the A350-1000 to capture the high-capacity market and the A350F to challenge Boeing’s long-standing dominance in the dedicated freighter market.

4. Strategic Challenges for 2026

- Airbus: The Supply Chain Bottleneck. Airbus’s primary struggle is not finding customers, but building the planes. Engine delays (notably the Pratt & Whitney GTF) and component shortages have hampered its ability to fully capitalize on its massive backlog.

- Boeing: Rebuilding Trust and Quality. Boeing is in a “Cultural Transformation” phase. After years of regulatory scrutiny, the company must prove to the FAA and global airlines that its quality management systems are flawless while simultaneously trying to reach a cash-flow-positive state.

5. Future Technology: Hydrogen vs. Sustainable Fuels

- Airbus (ZEROe): Taking a “Moonshot” approach by investing heavily in hydrogen-powered propulsion for 2035.

- Boeing (Sustainable Tech): Focusing on Sustainable Aviation Fuel (SAF) and the Transonic Truss-Braced Wing (TTBW) design in partnership with NASA, focusing on making current aerodynamic shapes significantly more efficient.

Summary: Airbus currently wins on Scale and Reliability, making it the market leader. Boeing is winning on Momentum and Recovery. If Boeing can sustain its early 2026 delivery rates, the duopoly will return to a much more balanced equilibrium by year-end.

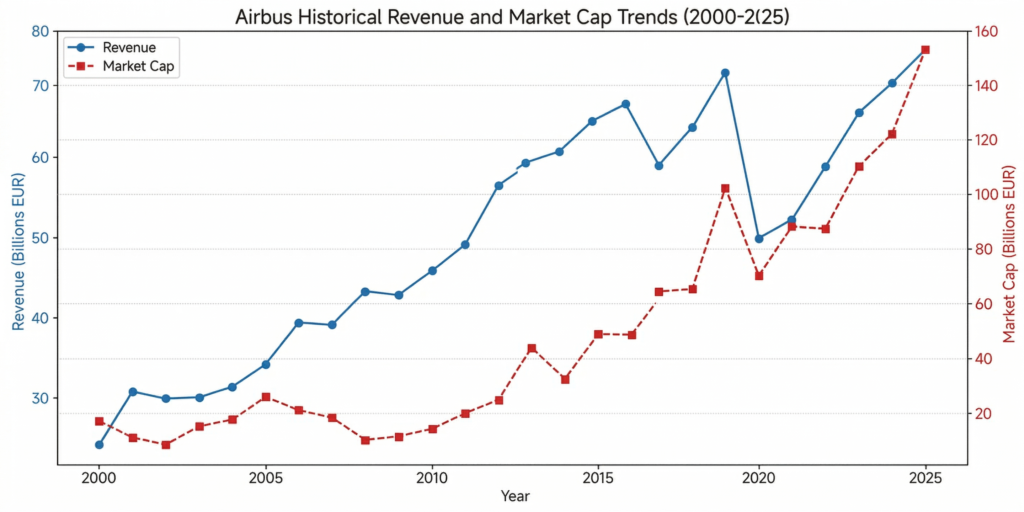

Source:

- https://www.airbus.com/en/investors

- https://www.macrotrends.net/stocks/charts/EADSY/airbus-se–/revenue

- https://www.macrotrends.net/stocks/charts/EADSY/airbus-se–/market-cap

- https://stockanalysis.com/quote/otc/EADSF/revenue/

- https://www.boeing.com/investors/

- https://www.reuters.com/business/aerospace-defense/airbus-vs-boeing-orders-deliveries-2025-2026/

Back to Airbus page