Abbott Laboratories was founded in 1888 and has a history spanning over 135 years. Its development can be divided into the following key stages:

Phase 1: Founding and the Alkaloidal Revolution (1888-1915)

- 1888: Dr. Wallace C. Abbott, a 30-year-old practicing physician, founded the company in Chicago. At the time, medicines were often liquid and unstable; he used active plant ingredients to create “alkaloidal granules,” which significantly improved dosage precision and stability.

- 1894: Formally incorporated as the Abbott Alkaloidal Company.

- 1907: Expanded overseas for the first time, opening an office in London.

Core Products: Alkaloidal granules (precisely dosed active plant extracts).

Core Strategy: Scientific Standardization. Moving away from unstable liquid medicines to provide doctors with reliable, pre-measured dosages.

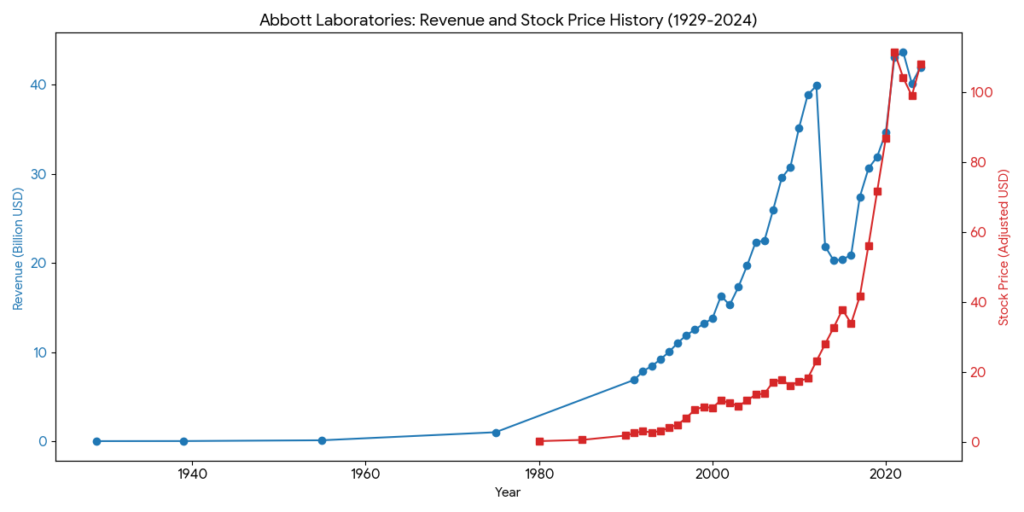

Revenue Level: Very small, early-stage growth. Annual sales reached approximately 200,000 USD by 1900.

Phase 2: Shift to Synthetic Pharmaceuticals and WWI (1915-1963)

- 1915: Renamed Abbott Laboratories to reflect the shift toward research into synthetic compounds.

- 1916: Produced Chlorazene, its first synthetic medicine, an antiseptic used to treat wounded soldiers during World War I.

- 1929: Successfully went public (IPO) during the year of the Wall Street crash; despite the timing, the stock price grew consistently from day one.

- 1935: Launched the famous anesthetic Pentothal (sodium thiopental), which became a global leader in anesthesia.

- 1942: Joined the mass production effort for Penicillin at the request of the U.S. government, with production increasing by over 20,000%.

Core Products: Chlorazene (antiseptic), Pentothal (anesthetic), Penicillin, and Erythrocin (antibiotic).

Core Strategy: Synthetic Chemistry and Scale. Transitioning from plant extraction to lab-synthesized compounds and scaling production to meet global wartime and post-war medical needs.

Revenue Level: Sales were 5M USD at the time of its 1929 IPO, growing to over 150M USD by the early 1960s.

Phase 3: Diversification and Leadership in Nutrition (1964-1971)

- 1964: Acquired M&R Dietetics, obtaining the famous infant formula brand Similac. This acquisition established Abbott’s leadership in the nutrition market.

- Product Expansion: In the following years, the company launched key nutritional products such as Pedialyte and Ensure.

Core Products: Similac (infant formula), Ensure (adult nutrition), and Pedialyte.

Core Strategy: Portfolio Diversification. Entering the medical nutrition market via the M&R Dietetics acquisition to balance the volatility of the pharmaceutical business.

Revenue Level: Reached the 400M to 500M USD range as nutrition became a major pillar of the business.

Phase 4: Rise of Diagnostics and Modern Medical Tech (1972-2012)

- 1972: Launched the ABA-100 blood chemistry analyzer and Ausria (a hepatitis test), marking Abbott’s entry into the modern diagnostics business.

- 1985: Developed the world’s first FDA-approved HIV blood test, a milestone for global blood supply safety.

- 2001: Acquired Knoll Pharmaceuticals, gaining Humira, which later became the world’s best-selling drug.

- 2004: Spun off its hospital products division to create Hospira (later acquired by Pfizer).

Core Products: ABA-100 analyzer, HIV diagnostic tests, Humira (immunology), and drug-eluting stents.

Core Strategy: Innovation-Led Expansion. Heavy investment in diagnostics and high-stakes biopharmaceuticals. This era focused on acquiring “blockbuster” potential (e.g., the Knoll acquisition for Humira).

Revenue Level: Explosive growth. Revenue was 13B USD in 2000, peaking at nearly 40B USD in 2012 just before the AbbVie spinoff.

Phase 5: Spinoff of AbbVie and Focus on MedTech (2013-Present)

- 2013: Conducted a historic strategic split. The proprietary pharmaceutical business was spun off into an independent company, AbbVie, while Abbott retained its medical devices, diagnostics, nutrition, and established pharmaceuticals (branded generics) businesses.

- 2014: Launched FreeStyle Libre, a continuous glucose monitoring system that revolutionized diabetes care.

- 2017: Acquired St. Jude Medical for 25 billion USD, strengthening its position in cardiovascular and neuromodulation sectors; in the same year, it acquired Alere to become a leader in rapid diagnostics.

- 2020: During the COVID-19 pandemic, Abbott quickly developed multiple testing tools (such as BinaxNOW), which became critical for pandemic control.

Core Products: FreeStyle Libre (CGM), Alinity (diagnostic systems), MitraClip, and COVID-19 rapid tests (BinaxNOW).

Core Strategy: MedTech Focus and Cash Flow Stability. Separating the high-risk/high-reward pharma wing (AbbVie) to focus on diversified medical devices, diagnostics, and steady-growth nutrition/generics.

Revenue Level: Post-split revenue started at 21.8B USD in 2013. It surged to over 43B USD during the 2021-2022 pandemic peak and has since stabilized around 40B USD.

As of early 2026, Abbott Laboratories (ABT) maintains a leading position in the global healthcare market through its highly diversified business model. Unlike many peers who focus solely on pharmaceuticals or devices, Abbott spans four distinct sectors, creating a unique competitive landscape.

1. Medical Devices: The Growth Engine

This is Abbott’s most valuable segment, where it competes fiercely with Medtronic, Boston Scientific, and Dexcom.

- Diabetes Care: Abbott is a global leader with its FreeStyle Libre system.

- Primary Rival: Dexcom (G7). While Dexcom is often seen as the “premium” technology leader, Abbott’s strategy focuses on mass-market penetration and affordability.

- 2026 Trend: The battle has shifted to “Health-Tech” for non-diabetics (e.g., Abbott’s Lingo vs. Dexcom’s Stelo), targeting metabolic health and athletes.

- Cardiovascular & Structural Heart:

- Primary Rivals: Boston Scientific and Medtronic.

- The PFA War: In 2026, the industry is transitioning to Pulsed Field Ablation (PFA) for treating AFib. Abbott is currently playing catch-up with its Volt PFA system against Boston Scientific’s Farapulse, which gained significant early market share.

2. Diagnostics: The Post-Pandemic Pivot

After the windfall from COVID-19 testing, Abbott is now refocusing on large-scale hospital lab automation.

- Primary Rivals: Roche, Danaher (Beckman Coulter/Cepheid), and Siemens Healthineers.

- Competitive Edge: Abbott’s Alinity platform is highly regarded for its small footprint and high throughput.

- Point-of-Care (PoC): Abbott remains the dominant force in rapid bedside testing, though Danaher’s Cepheid remains a formidable challenger in rapid molecular diagnostics.

3. Nutrition: Global Consumer Defense

This segment provides steady cash flow but faces lower margins and high regulatory scrutiny.

- Primary Rivals: Nestlé, Reckitt (Mead Johnson), and Danone.

- Market Dynamics: Following the 2022-2023 supply chain disruptions in infant formula, Abbott has regained its U.S. leadership. However, Nestlé remains the larger global player with a more extensive portfolio in specialized medical nutrition (e.g., tube feeding).

4. Established Pharmaceuticals (EPD): Emerging Market Focus

Abbott does not compete with Big Pharma (like Pfizer or Novartis) in drug discovery. Instead, it sells “Branded Generics” in high-growth emerging markets.

- Primary Rivals: Viatris and local giants like Sun Pharma (India).

- Strategy: By leveraging the “Abbott” brand name in regions like India, Brazil, and Russia, the company can charge a premium over unbranded generics, as doctors in these regions often trust multinational quality standards more than local alternatives.

Comparative Competitive Matrix (2026 Outlook)

| Metric | Abbott (ABT) | Medtronic (MDT) | Johnson & Johnson (JNJ) | Dexcom (DXCM) |

| Diversification | Very High | High (Devices only) | High (MedTech + Pharma) | Low (Diabetes only) |

| Growth Driver | FreeStyle Libre / PFA | Robotics / Neuromod | Oncology / MedTech | CGM Expansion |

| P/E Ratio (Est.) | ~24x | ~16x | ~15x | ~45x |

| Dividend Yield | ~1.9% (Aristocrat) | ~3.2% | ~3.0% | 0% |

Summary for Investment Analysis

Abbott’s primary competitive advantage is its “All-Weather” nature. When diagnostic sales fluctuate, medical devices often compensate. In 2026, the critical factor to watch is Abbott’s ability to gain FDA approval for new cardiac technologies to bridge the gap created by Boston Scientific’s recent surge in electrophysiology.

In 2026, the FreeStyle Libre 3 (FSL3) remains the dominant Continuous Glucose Monitor (CGM) globally by market share. However, the competition has intensified as Abbott and its rivals move beyond traditional diabetes care into the “health and wellness” market for non-diabetics.

1. The “Big Three” Comparison (Medical Use)

The primary battle in the prescription market is between Abbott, Dexcom, and Medtronic.

| Feature | FreeStyle Libre 3 (Abbott) | Dexcom G7 | Guardian 4 (Medtronic) |

| Accuracy (MARD) | ~7.9% (Best in some trials) | ~8.0% – 8.2% | ~10.5% |

| Wear Time | 14 – 15 Days | 10 Days (+12hr grace) | 7 Days |

| Data Frequency | Every 1 Minute | Every 5 Minutes | Every 5 Minutes |

| Warm-up Time | 60 Minutes | 30 Minutes (Fastest) | 2 Hours |

| Calibration | Factory (No fingerpricks) | Factory (Optional manual) | Required for some modes |

| Size | Smallest (2 pennies) | Small (1 nickel) | Bulkier (Separate transmitter) |

2. Competitive Edge & Key Differentiators

Abbott’s “Low-Cost, High-Volume” Strategy

Abbott’s primary advantage is affordability and insurance coverage. By positioning FSL3 as a mass-market device, they have captured the majority of Type 2 diabetes users. Their 1-minute data update (compared to Dexcom’s 5 minutes) is a significant technical edge for real-time responsiveness.

The Dexcom Threat: Precision & Ecosystem

Dexcom G7 is widely considered the “premium” choice for Type 1 diabetics. Its software integration is superior, offering better predictive alerts and seamless connections to automated insulin delivery (AID) systems like Omnipod 5 and Tandem t:slim. While Abbott is catching up with “open ecosystem” partnerships, Dexcom started with a lead in pump interoperability.

Medtronic’s Closed Loop

Medtronic remains competitive mainly for users already using their insulin pumps (MiniMed 780G). Their Guardian 4 sensor is designed specifically to work within their proprietary “Closed Loop” system, though it is generally seen as less convenient due to its larger size and shorter wear time.

3. The New Battleground: Over-the-Counter (OTC)

In 2026, the competition has shifted to non-prescription “Bio-wearables” for metabolic health.

- Abbott Lingo vs. Dexcom Stelo:

- Lingo (Abbott): Focuses on coaching and education. It is designed for general wellness, helping users understand how food and exercise impact their metabolism. It updates every minute.

- Stelo (Dexcom): Focuses on Type 2 diabetics not using insulin. It offers a longer 15-day wear time and leverages the high-precision G7 hardware but with a slower 15-minute data update to save battery.

4. SWOT Summary for FreeStyle Libre

- Strengths: Smallest form factor, lowest price point, 14-15 day wear, 1-minute updates.

- Weaknesses: Slightly longer warm-up time (60 min) than G7 (30 min), fewer predictive alert customizations.

- Opportunities: Expansion into the “Lingo” wellness market; dual-sensor technology (Glucose + Ketones).

- Threats: Dexcom’s aggressive pricing with Stelo; rapid adoption of PFA (Pulsed Field Ablation) where competitors have strong diagnostic ties.

In the 2026 IVD (In-Vitro Diagnostics) market, Abbott’s Alinity platform is defined by its core philosophy of “Harmonization.” Unlike competitors who often have fragmented systems for different testing types, Alinity uses a unified interface and hardware design across clinical chemistry, immunoassay, hematology, and molecular diagnostics.

1. The “Big Four” Diagnostic Ecosystems (2026)

Abbott competes primarily with Roche, Danaher, and Siemens Healthineers.

| Domain | Abbott (Alinity) | Roche (cobas) | Danaher (Beckman Coulter) | Siemens (Atellica) |

| Integrated Suite | Alinity ci-series | cobas Pro / Pure | DxC / DxI series | Atellica Solution |

| Molecular | Alinity m | cobas 6800/8800 | Cepheid GeneXpert | Atellica m |

| Hematology | Alinity h-series | cobas m 511 | DxH series | Atellica Hema |

| Key Strength | Space Efficiency | Test Menu Depth | Workflow Automation | AI & Magnetic Track |

2. Strategic Competitive Advantages

A. Footprint and Throughput (The “Space” War)

Alinity’s biggest selling point is its vertical integration. It provides significantly higher throughput per square meter compared to competitors. For urban hospitals where laboratory space is at a premium, Alinity allows for more modules in a smaller area without sacrificing speed.

B. Operational Harmonization

Abbott is the only manufacturer that has truly standardized the user experience. An operator trained on the Alinity c (Chemistry) can operate the Alinity i (Immunoassay) or Alinity m (Molecular) with almost no additional training. This reduces human error and lowers labor costs in an era of global healthcare staffing shortages.

C. The “Random Access” Molecular Revolution

Traditionally, molecular (PCR) testing required “batching” (waiting for enough samples to fill a tray). Alinity m allows for True Random Access, meaning samples can be loaded as they arrive. This directly challenges Danaher’s Cepheid, which dominates rapid testing, by offering the same flexibility but at a massive laboratory scale.

3. Competitor Counter-Strategies

- Roche (The Market Leader): Roche remains the “standard” due to its massive Test Menu. They offer more niche assays (oncology, rare diseases) than Abbott. Their newer cobas Pro is a direct response to Alinity, attempting to match its footprint efficiency.

- Danaher (The Workflow King): Through its DHR/Beckman Coulter division, Danaher focuses on the “Total Lab Automation” (TLA) track. They excel in the pre-analytical phase (sorting and centrifuging samples) better than anyone else.

- Siemens (The Innovator): Their Atellica system uses a patented magnetic sample transport technology that is faster than the traditional belts used by Abbott and Roche.

4. SWOT Analysis: Alinity

- Strengths: Unified software/hardware (Harmonization), highest throughput-to-footprint ratio, rapid molecular turnaround.

- Weaknesses: Switching costs are extremely high (once a lab is “Alinity-standardized,” it is hard to leave), fewer niche oncology markers than Roche.

- Opportunities: The trend toward Lab Consolidation (smaller labs merging into mega-labs) favors Alinity’s modular and scalable design.

- Threats: Aggressive pricing from Chinese domestic competitors (like Mindray) in emerging markets, which may undercut Abbott on cost-per-test.

In 2026, the adult nutrition market is no longer just about “meal replacement.” It has evolved into a high-stakes arena of Medical Nutrition Therapy (MNT) and Metabolic Health. Abbott (Ensure/Glucerna) remains the global leader with roughly a 30-35% market share, but it faces distinct challenges from Nestlé’s clinical focus and Danone’s specialization.

1. Competitive Landscape: The “Big Three” in 2026

| Feature | Abbott (Ensure/Glucerna) | Nestlé Health Science (Boost/Peptamen) | Danone (Nutricia/Fortisip) |

| Dominant Philosophy | Muscle Health & Aging | Therapeutic & Gut Health | Specialized Clinical Care |

| Hero Ingredient | HMB (Muscle preservation) | MCT & Probiotics | Disease-specific protein blends |

| Key Advantage | Mass market trust; hospital-to-home continuity. | Expertise in “Medical Foods” for GI and allergy. | Market leader in Europe; strong oncology portfolio. |

| New 2026 Focus | GLP-1 Muscle Support | Personalized Bio-hacking | Plant-based Medical Nutrition |

2. Strategic Battlegrounds

A. The GLP-1 “Muscle Preservation” War

The rise of weight-loss drugs (Wegovy, Zepbound) has created a massive new sub-segment.

- Abbott’s Strategy: In early 2026, Abbott launched Ensure Max Protein 2-in-1, specifically marketed to help the millions of GLP-1 users maintain lean muscle mass while losing weight. They leverage their HMB (beta-hydroxy-beta-methylbutyrate) patent to claim superior muscle protection compared to standard high-protein shakes.

- Competitor Move: Nestlé countered by launching a “GLP-1 Companion” line under its Boost brand, focusing on high fiber and micro-nutrient density to combat the “stomach paralysis” (gastroparesis) side effects common with these drugs.

B. Personalized and “Connected” Nutrition

- Abbott’s Edge: Abbott is uniquely positioned because it owns the FreeStyle Libre and Lingo biowearables. In 2026, they are integrating these tools so that a “glucose spike” or “dip” detected by the sensor can trigger a personalized recommendation for a Glucerna shake via the user’s smartphone.

- Nestlé’s Edge: Nestlé is investing heavily in Nutrigenomics (nutrition based on your DNA). They are moving toward “Medical Foods” that require a prescription, targeting specific metabolic errors that Abbott’s mass-market Ensure does not address.

C. The “Clean Label” and Plant-Based Shift

- Danone’s Stronghold: Danone (Nutricia) has taken the lead in the “Plant-Based Medical” sector. As the “anti-processed food” movement grows among the younger elderly (Baby Boomers), Danone’s use of pea and soy proteins in medical-grade formats is gaining traction in Europe and North America.

- Abbott’s Response: Abbott has expanded its “Ensure Plant-Based” line but still relies heavily on milk-based proteins for its core clinical products, prioritizing calorie density and shelf stability over “organic” labels.

3. SWOT Analysis for Abbott Nutrition (2026)

- Strengths: HMB Patent provides a scientific “hook” that competitors find hard to replicate. Massive distribution in retail (Walmart/Costco) and hospitals gives them a 2-for-1 advantage.

- Weaknesses: Perceived as “highly processed.” High sugar content in standard Ensure versions is a target for competitors like Glucerna’s own rivals.

- Opportunities: The “Aging-in-Place” trend. As more care moves from hospitals to homes, Abbott’s home-delivery subscription models for Ensure are seeing 15% YoY growth.

- Threats: Private Label Growth. Retailers like Amazon and CVS are launching their own “Compare to Ensure” versions at 40% lower price points, eating into the “standard” nutrition segment.

Sources:

Back to Abbott page