The development history of Eoptolink (300502.SZ) can be divided into the following four main stages based on technical evolution, business transformation, and capital market activities:

Stage 1: Inception and Accumulation (2008 – 2011)

- Founding Background: Founded in 2008 by Gao Guangrong and others, the company integrated resources in the optical communication field, initially focusing on the production and sales of low-to-medium speed optical transceivers.

- Laying the Foundation: During this period, the company established its core R&D direction and set the groundwork for entering mainstream telecommunications markets by implementing standardized quality management systems (such as ISO9001).

- Corporate Restructuring: Completed its joint-stock reform in 2011, renamed to Chengdu Eoptolink Technology Inc., Ltd., and established a wholly-owned subsidiary, Sichuan Eoptolink, to define the operational division between R&D centers and production bases.

Stage 2: Public Listing and Business Expansion (2012 – 2017)

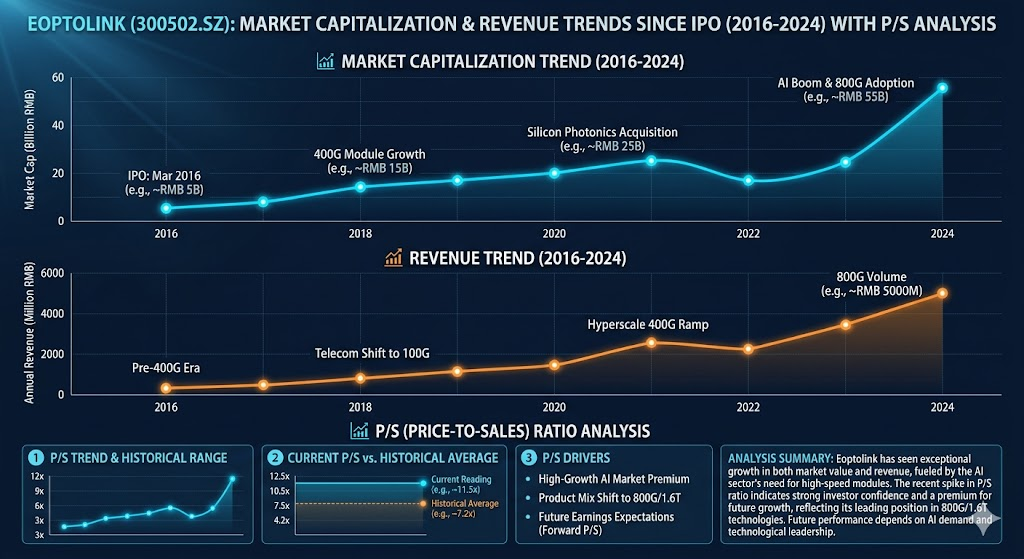

- Going Public: In March 2016, the company officially listed on the Shenzhen Stock Exchange ChiNext board, utilizing raised funds to expand production capacity and enhance automated manufacturing capabilities.

- Technological Breakthrough: In 2017, the company successfully developed and delivered 100G telecommunications backhaul optical transceivers for ZTE, marking a significant technological milestone in the high-end telecom sector and strengthening partnerships with telecommunications equipment manufacturers.

Stage 3: Globalization and Structural Upgrading (2018 – 2023)

- Market Shifting: Facing global digitalization demands, the company successfully expanded its business focus from solely the telecommunications market to overseas data center markets, shifting its product structure toward 400G high-speed modules.

- Strategic Acquisition: In 2021, the company acquired Alpine Optoelectronics, allowing it to master core Silicon Photonics technology platforms and achieve a full industrial chain layout from chip packaging to module manufacturing.

- Industry Status: Starting from 2020, the company’s market share significantly increased, successfully ranking among the top ten global optical transceiver manufacturers.

Stage 4: The Era of Artificial Intelligence Computing (2024 – Present)

- AI-Driven Growth: With the explosion of generative AI, demand for high-bandwidth interconnects in data centers surged. By leveraging its leading position in 800G and even higher-speed optical modules (such as R&D related to 1.6T), the company has become a core supplier for global AI computing infrastructure.

- Deepening Internationalization: The company continues to strengthen its international market presence and, in 2026, announced plans for a secondary listing on the Hong Kong Stock Exchange, aiming to further expand international capital channels to meet rapidly growing global order demand.

Eoptolink (300502.SZ) currently occupies a leading position in the global optical transceiver market, with primary competition concentrated in the field of high-speed optical transceivers for data centers (such as 800G and 1.6T). The following is an analysis of the current competitive landscape:

1. Key Competitors

In the capital markets, Eoptolink, Innolight, and HG Genuine (an optical component supplier) are collectively referred to as the “Yi-Zhong-Tian” trio of the optical transceiver sector.

- Innolight: Currently Eoptolink’s strongest competitor. The two are locked in intense competition for market share in 800G and 1.6T products, as both are core suppliers to top-tier global hyperscalers. Innolight entered the market for large-scale production and overseas capacity layout earlier and holds a dominant market share.

- Coherent (formerly Finisar): A global industry leader. Coherent possesses deep vertical integration capabilities (from chips and lasers to packaging) and maintains a formidable technological stronghold in high-speed optical transceivers and coherent optical communications. Eoptolink primarily competes against it through superior cost control and agile delivery capabilities.

- Other Key Participants:

- Accelink: A major domestic Chinese manufacturer of optical transceivers for both telecommunications and data centers, with solid technical expertise.

- Lumentum: A leader in optical communication components and laser technology, competing with Eoptolink in high-end module products.

- Others: Companies like Cambridge Industries Group (CIG) and HG Genuine are also continuously increasing R&D investment in high-speed rate modules.

2. Core Competitive Dimensions

Eoptolink currently maintains its competitiveness through several key dimensions:

- Product Iteration Capability: Eoptolink has demonstrated extremely rapid volume production of 800G products and is accelerating the certification and mass production of 1.6T products. This is critical for maintaining market share in AI computing infrastructure.

- Technological Strategic Layout: Following the acquisition of Alpine Optoelectronics in 2021, Eoptolink mastered Silicon Photonics technology. This provides an independent R&D advantage in reducing power consumption and increasing transmission efficiency, giving the company a stronger position in meeting the strict energy-efficiency requirements of data centers.

- Overseas Capacity Layout: To mitigate geopolitical risks and meet the needs of overseas customers, Eoptolink is actively advancing the construction and capacity expansion of its factory in Thailand. This is a crucial bargaining chip in competing for global orders against industry leaders.

3. Current Market Challenges

- Technological Fragmentation and Cost Pressure: Exclusive network architectural requirements from various major cloud providers (such as Google, Meta, and AWS) lead to high R&D expenditures. Simultaneously, as mainstream products like 800G enter large-scale mass production, price competition has intensified, challenging gross profit margins.

- Exchange Rate and Supply Chain Volatility: As a highly export-oriented enterprise, fluctuations in exchange rates directly impact net profit performance. Furthermore, securing upstream capacity for critical raw materials and DSP chips is a core test for ensuring delivery stability.

- Shifts in AI Computing Infrastructure: The industry is facing a potential transition in network architecture from InfiniBand to Ethernet, as well as the race for cutting-edge technologies like CPO (Co-Packaged Optics), requiring the company to maintain high-intensity R&D investment.

Conclusion

Eoptolink’s current advantage lies in its rapid response to AI computing demand and its agile delivery capabilities. Whether it can continue to prevail depends on its ability to achieve technological breakthroughs in 1.6T products and further optimize its cost structure through the economies of scale from its expanding capacity, effectively defending against pressure from both international giants and domestic peers.

Source:

- https://www.eoptolink.com/

- https://en.wikipedia.org/wiki/Eoptolink

- https://www.eeworld.com.cn/mp/XSY/a407565.jspx

- https://finance.sina.com.cn/roll/2026-05-16/doc-inhxzzur2856647.shtml

- https://www.geninnov.ai/blog/optical-rivalries-where-one-tech-must-lose-for-the-other-to-win

- https://portersfiveforce.com/blogs/competitors/coherent

Back to Eoptolink page