Zhongji Innolight (300308.SZ) Latest Quarterly Earnings Summary

Based on public data provided by TradingView, here is a summary of the financial performance for Zhongji Innolight (300308.SZ) for the last quarter:

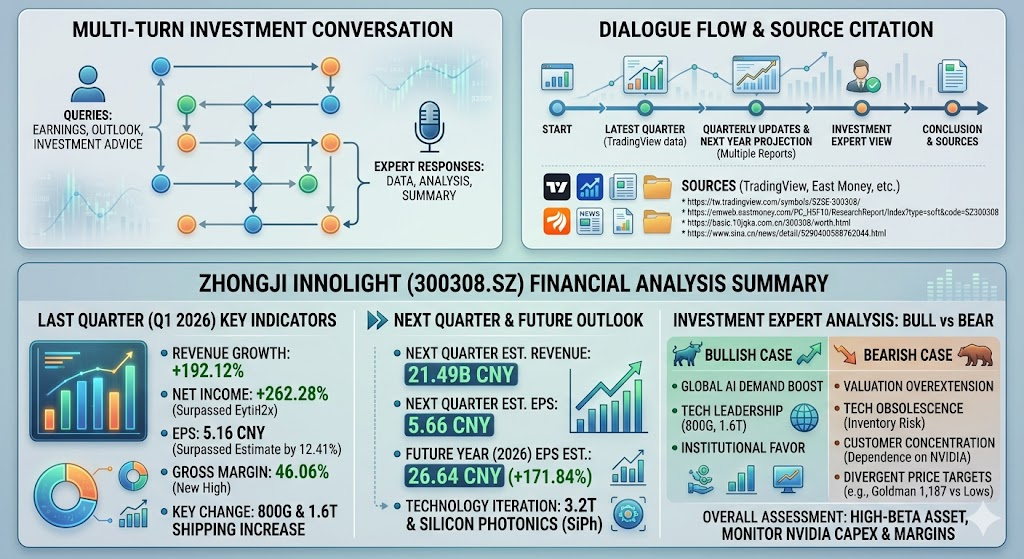

Key Financial Indicators

- Earnings Per Share (EPS): 5.16 CNY (Surpassed the estimated 4.59 CNY, an upside surprise of 12.41%)

- Net Income: 5.73B CNY

Future Outlook

- Next Quarter Estimated EPS: 5.66 CNY

- Next Quarter Estimated Revenue: 21.49B CNY

Zhongji Innolight (300308.SZ) 2026 Q1 Financial Highlights and Outlook

Key Changes This Quarter (2026 Q1)

- Rapid Revenue and Profit Growth: Revenue reached 19.496B CNY, a year-over-year increase of 192.12%. Net income attributable to shareholders was 5.735B CNY, a year-over-year increase of 262.28%.

- Product Mix Upgrades: Driven by robust global investment in computing infrastructure, the shipment proportion of high-speed optical modules such as 800G and 1.6T continued to rise, driving economies of scale and enhanced profitability.

- Record High Gross Margin: The gross margin climbed from 33.81% in 2024 to 46.06% in 2026 Q1, reflecting strong product pricing power.

- Operational Pressure: Despite impressive profits, the growth rate of operating cash flow (55.58%) was lower than the net profit growth rate, reflecting collection pressures. Inventory levels increased to 15.672B CNY, and days sales of inventory rose to 121 days, necessitating monitoring of inventory impairment risks due to rapid technological iteration.

Outlook for Next Quarter

- Demand Support: Terminal customer capital expenditure in the computing field is expected to continue increasing, with 800G and 1.6T optical modules acting as core drivers.

- Capacity Expansion: The company is increasing capacity investment to meet downstream demand and is continuously optimizing supply chain management, ensuring delivery capabilities through tighter agreements and strategic inventory.

- Technological Iteration: Continued promotion of the 3.2T product roadmap and deepening the layout of Silicon Photonics (SiPh) technology to enhance the performance and cost advantages of subsequent products.

Next Year (2026) EPS Forecast

Based on consensus forecasts from various institutions (as of May 24, 2026):

- 2026 Annual Estimated EPS: Approximately 26.64 CNY.

- Year-over-Year Growth Rate: Expected to increase by approximately 171.84% compared to 2025.

Summary of Market Bull and Bear Perspectives

Current market sentiment toward Zhongji Innolight shows a significant split, reflecting both its high growth potential as a core supplier for AI infrastructure and its inherent volatility.

1. Potential Upside (Bullish Case)

- Driven by Strong AI Computing Demand: Benefiting from the evolution of data centers from scale-out to scale-up architectures, demand for high-bandwidth optical interconnects is surging. Analysts (e.g., Goldman Sachs) have raised their price targets to 1,187 CNY, forecasting multi-fold growth in the optical networking market over the next two years.

- Technological Leadership: The company holds a dominant position in the high-end 800G and 1.6T optical module market. Its strong order book and high gross margins demonstrate significant pricing power.

- Institutional Favor: As a core holding for major public funds, the market assigns a high growth premium to its status as a critical “pick-and-shovel” provider in the AI supply chain.

2. Potential Downside (Bearish Case)

- Valuation Overextension and Crowded Trades: Some market observers note that current valuations have front-run growth expectations for the next 1-2 years. Given high institutional concentration, any deceleration in marginal growth (such as a slowdown in revenue growth rates observed in 2025 Q4) could trigger a sell-off.

- Technological Iteration and Inventory Impairment: As the next generation of technologies like 3.2T approaches, existing production lines and inventory face rapid technological obsolescence, which could lead to significant impairment risks and erode profits.

- Customer Concentration Risk: Revenue is highly dependent on global tech giants (particularly NVIDIA). A shift in customer capital expenditure strategies or a pivot toward CPO/OIO technology pathways would directly impact the company’s performance.

- Divergent Price Targets: Although the average analyst price target remains in the 890-915 CNY range, some conservative analysts have issued targets as low as 430-607 CNY, implying a potential correction of over 30%-50%.

Investment Advice and Risk Warnings

- Overview of Potential: Based on consensus forecasts, the average price target is approximately 914 CNY; however, the extreme variance in valuation targets (ranging from 430 CNY to 1,278 CNY) is notable. I advise against relying on a single price target, as the stock is highly sensitive to overall AI industry sentiment.

- Key Metrics to Monitor:

- Gross Margin: Monitor if it can be maintained above the 40% level.

- Days Sales of Inventory (DSI): A continuous increase indicates rising inventory backlog risks, which often serves as a warning for technological obsolescence.

- Operating Cash Flow: If net profit continues to grow while cash flow lags, be wary of collection pressures.

Expert Recommendation: Zhongji Innolight is currently a high-beta asset. For long-term investors, closely monitor NVIDIA’s capital expenditure reports and the optical communication technology replacement cycle. For tactical traders, it is essential to strictly manage position sizing and remain vigilant toward sharp volatility during earnings seasons or institutional rebalancing.

Disclaimer: The information above is for reference only and does not constitute investment advice. Investing involves risk; please make decisions based on your individual risk tolerance.

Source:

- https://tw.tradingview.com/symbols/SZSE-300308/

- https://emweb.eastmoney.com/PC_HSF10/ResearchReport/Index?type=soft&code=SZ300308

- https://basic.10jqka.com.cn/300308/worth.html

- https://www.sina.cn/news/detail/5290400588762044.html

Back to Innolight page