History of Zhongji Innolight (300308.SZ): Evolution Stages

The development of Zhongji Innolight can be categorized into three distinct phases, marking its transformation from a traditional machinery manufacturer to a global leader in optical communications.

Phase 1: Traditional Motor Manufacturing (2005-2016)

The company was originally founded as Zhongji Equipment in 2005, focusing on the motor winding manufacturing sector. It primarily produced stator winding equipment for motors and was listed on the Shenzhen Stock Exchange in 2012. During this period, the company accumulated technical expertise in precision manufacturing and established the capital foundation that would later support its strategic shift.

Phase 2: Strategic Acquisition and Transformation (2017-2019)

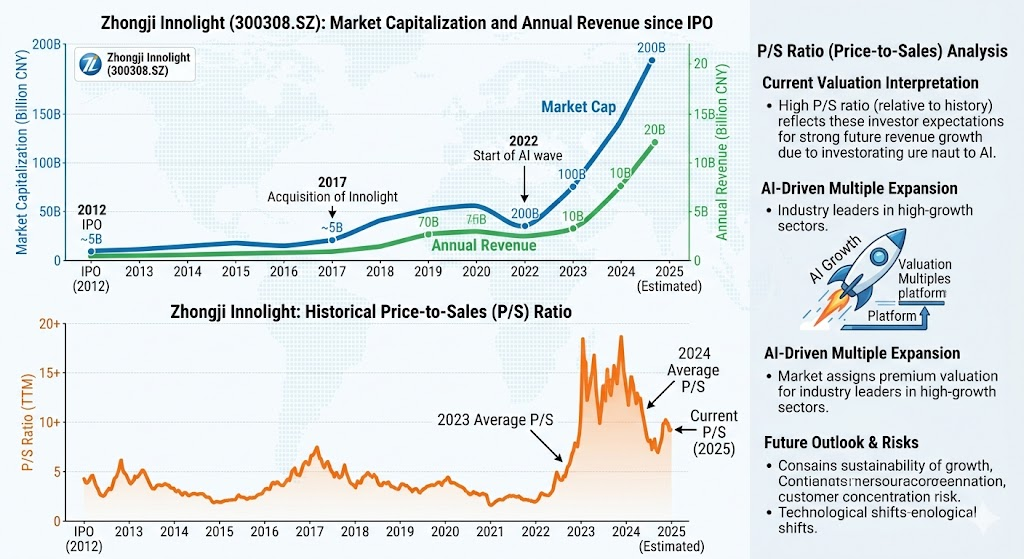

In 2017, the company executed a major asset restructuring by issuing shares to acquire Suzhou Innolight Technology. This move marked its entry into the optical communication industry, followed by a formal name change to Zhongji Innolight. Suzhou Innolight, founded by experts in the optical sector, provided the core R&D and mass production capabilities for high-speed optical modules. This phase solidified the company’s transition from traditional mechanical manufacturing to high-tech optical communications, with a dedicated focus on data center modules.

Phase 3: Global Expansion and AI-Driven Growth (2020-Present)

With the rapid acceleration of global cloud computing and artificial intelligence, the company entered a period of explosive growth. By leveraging its technological leadership in 400G and 800G optical modules, the company successfully secured a position within the supply chains of major North American Cloud Service Providers (CSPs), establishing itself as a core entity in global AI infrastructure. In recent years, the company has actively expanded into 1.6T high-speed modules and silicon photonics, continuing to drive technical innovation across the optical communication industry.

Competitive Analysis of Zhongji Innolight (300308.SZ)

As of 2026, Zhongji Innolight stands as the global leader in the AI optical transceiver market, bolstered by high technical barriers and deep integration within the supply chain.

1. Market Position and Competitive Advantages

- Market Share Dominance: Zhongji Innolight holds a 40%-50% global market share in 800G optical modules and a 50%-70% share in the 1.6T segment. As the core and often exclusive primary supplier to top North American AI infrastructure providers (e.g., NVIDIA, Google), the company wields significant pricing power and technical standard-setting influence.

- Technological Leadership: The company follows a tiered development strategy: mass-producing current generations, refining breakthroughs, and pre-researching future technologies. Beyond 1.6T modules, it is actively deploying next-generation system-level products, including NPO (Near-Packaged Optics), XPO (External Packaged Optics), and OCS (Optical Circuit Switches), shifting its role from a “component supplier” to a “system integrator.”

- Cost and Production Moat: Through vertical integration (e.g., self-developed silicon photonics solutions that reduce costs by 15%-20% compared to traditional EML) and offshore production footprints (e.g., in Thailand), the company effectively mitigates geopolitical risks and cost pressures.

2. Major Competitors

Zhongji Innolight competes primarily with global optical giants that possess comparable vertical integration capabilities and financial strength:

- Coherent (NYSE: COHR): A leader in optical communications, offering optical modules, silicon photonics components, and OCS systems. Coherent possesses strong upstream materials advantages (InP laser chips) and has received significant investment from NVIDIA to ensure supply chain security, making it the primary rival for high-end specifications and key client relationships.

- Lumentum (NASDAQ: LITE): Also deeply entrenched in optical communications and laser technology, Lumentum has secured strategic partnerships with NVIDIA. Its R&D capabilities in silicon photonics and high-end lasers represent a major competitive pressure for Zhongji Innolight during high-speed product iterations.

- Domestic Followers (e.g., HG Tech, FiberHome): While competitive on cost in mid-to-low-end and domestic telecommunications markets, they currently maintain a noticeable technical gap in the yield and readiness of top-tier 800G/1.6T AI data center modules.

3. Key Industry Challenges

- Supply Chain Bottlenecks: With the global AI optical module market estimated at 26B in 2026 (a 57% year-over-year increase), the supply-demand imbalance for key components like high-quality laser chips remains an industry-wide challenge.

- Customer Concentration Risk: Over 75% of revenue comes from the top five clients. While this secures high-end demand, it leaves the company highly sensitive to the capital expenditure (CapEx) policies of major North American cloud providers.

- Technological Path Competition: Industry disagreement persists regarding the future of pluggable modules versus LPO (Linear Drive) and CPO (Co-Packaged Optics). If the transition to next-generation packaging technologies accelerates, it will test the company’s technical agility.

In summary, Zhongji Innolight has built a deep competitive moat by extending its product line into the system layer (OCS), widening the gap with traditional module manufacturers. However, its continued leadership will depend on its ability to maintain technological superiority and supply chain stability against global giants like Coherent that possess deeper vertical integration in the chip space.

Source:

- https://www.innolight.com/

- https://caifuhao.eastmoney.com/news/20260312032442870136140

- https://blog.csdn.net/anpeng3188/article/details/160311777

- https://money.udn.com/money/story/5612/9452815

- https://www.indmoney.com/blog/us-stocks/ai-optical-networking-stocks-nvidia-ai-infrastructure

Back to Innolight page