Here is the summary of Lowe’s Companies, Inc. (NYSE: LOW) latest quarterly financial results for the first quarter of 2026, released on May 20, 2026:

Core Financial Performance

- Revenue: 23.1B, up 10.3% year-over-year (YoY).

- Comparable Sales: Increased by 0.6% YoY.

- Adjusted Earnings Per Share (EPS): 3.03, up 3.8% YoY, outperforming the market expectation of 2.02.

Full-Year 2026 Guidance (Reiterated)

The company maintained its previously issued financial outlook for the full fiscal year 2026:

- Total Revenue: Expected to be between 92.0B and 94.0B.

- Comparable Sales: Expected to range from flat to up 2%.

- Adjusted EPS: Expected to be in the range of 12.25 to 12.75.

- Capital Expenditures: Projected to be up to 2.5B.

Here are the key operational changes and market trends highlighted in Lowe’s first quarter 2026 earnings release and conference call:

Strategic Acquisitions Driving Revenue Growth

The notable 10.3% increase in total revenue was primarily driven by the recent acquisitions of Foundation Building Materials (FBM) and Artisan Design Group (ADG). These strategic moves significantly expanded Lowe’s footprint in the pro construction materials and interior design services segments. While these acquisitions created a short-term 70-basis-point headwind on gross margin due to 96 million in pre-tax integration expenses, they successfully accelerated overall top-line volume.

Two-Tiered Customer Performance: Pro vs. DIY

- Pro and Installation Services Expansion: Backed by the ongoing Total Home strategy, demand from professional contractors and installation segments remained robust, serving as the main anchor to keep comparable store sales in positive territory at 0.6%.

- Persistent DIY Weakness: The do-it-yourself market remained soft. Elevated interest rates, sluggish housing turnover, and severe winter storms in February that delayed the start of the spring selling season all contributed to consumers remaining cautious about discretionary, big-ticket home improvement spending.

Digital Expansion and AI Integration Payoffs

Online sales delivered strong performance with a 15.5% YoY increase, supported by expanded fulfillment capabilities such as same-day delivery options. Furthermore, the company expanded the roll-out of its generative AI tools, MyLowe and MyLowe Companion, which now field over 1M customer inquiries monthly. Internal metrics indicate that online shoppers utilizing these AI tools demonstrate a conversion rate three times higher than non-users.

Gross Margin and Operating Margin Compression

Despite progress in e-commerce and pro channels, the gross margin contracted by 70 basis points YoY to 32.7%, while the adjusted operating margin dipped slightly by 43 basis points to 11.5%. This compression was largely due to the initial dilutive impact of the FBM and ADG acquisitions, coupled with promotional pressures in a tight macro environment. However, disciplined management of SG&A expenses, which improved by 17 basis points as a percentage of sales, helped cushion the bottom-line impact.

According to Lowe’s first quarter 2026 earnings call and financial reports, the company expects its growth momentum in the upcoming quarters to be driven by the following four core catalysts:

1. Peak Spring Season Realization and SpringFest Momentum

Due to severe winter storms in February that delayed the typical onset of spring home improvement projects across the United States, the true seasonal peak only began to materialize late in the first quarter.

- Core Catalyst: The third annual “SpringFest” promotional event is expected to fully drive sales in the upcoming quarter, particularly for lawn and garden, outdoor power equipment, and patio categories.

- Expanded Merchandising: The nationwide rollout of dedicated “Workwear” and “Pet” sections within retail locations will continue to scale through the rest of the year, acting as a critical tool to expand average ticket size.

2. Deepening Pro Penetration and “Pro Extended Aisle” Synergy

With the DIY market exhibiting a slower recovery curve, the professional contractor segment remains the primary growth engine.

- Supply Chain Synergies: The company is accelerating the cross-selling capabilities of its recent Foundation Building Materials (FBM) and Artisan Design Group (ADG) acquisitions. Through the “Pro Extended Aisle” initiative, Lowe’s is expanding its wholesale commercial and residential building materials catalog to capture larger project shares.

- Retention Rewards: Tailored incentives within the MyLowe’s Pro Rewards ecosystem, including free same-day delivery for qualifying orders over 25, are designed to maximize repeat purchasing frequency among contractors.

3. Expansion of Home Services and New Subscription Model

As consumers adopt a more cautious stance on large-scale DIY projects, demand for professional installation and Do-It-For-Me (DIFM) programs has strengthened.

- Ticket Drivers: Big-ticket installation services, such as HVAC systems and window replacements, maintain solid pipeline demand.

- Recurring Revenue Streams: The newly introduced “HomeCare+” residential maintenance subscription program seeks to pivot transactional repair needs into consistent recurring revenue, anchoring long-term relationships with homeowners.

4. Digital Conversion and PPI Productivity Enhancements

The digital sales momentum, which posted a 15.5% YoY increase in the first quarter, is projected to sustain its trajectory.

- Monetizing Gen-AI: The MyLowe customer-facing generative AI assistant, which logged over 1M monthly inquiries and demonstrated a 3x higher conversion rate, will see expanded features to further capitalize on digital traffic.

- Internal Efficiency: Store associates utilizing the “MyLowe Companion” tool, paired with Perpetual Productivity Improvement (PPI) initiatives, will accelerate pro quote generation and optimize store-level inventory management to offset near-term gross margin dilution.

Based on Lowe’s Q1 2026 earnings release and updated management guidance, the trajectory of the company’s Earnings Per Share (EPS) over the next year is shaped by the following key dynamics:

Full-Year 2026 EPS Guidance and Market Reaction

- Official Forecast Range:

- Reported Diluted EPS: Expected to be between 11.75 and 12.25.

- Adjusted Diluted EPS: Reiterated at the previously guided range of 12.25 to 12.75.

- Consensus vs. Guidance: While Q1 adjusted EPS of 3.03 came in ahead of Wall Street expectations, management’s decision to maintain rather than lift full-year guidance suggests a cautious stance for the remainder of the year. This reiteration fell slightly below the most optimistic buy-side expectations, prompting minor target price recalibrations from several investment banks post-earnings.

Tailwinds: Drivers of Near-Term EPS Expansion

To push EPS toward the upper bound of the 12.75 target, the company will rely on internal margin-stabilization initiatives:

- Acquisitive Synergy Realization: Q1 earnings were weighed down by 96 million in pre-tax transaction and integration costs from FBM and ADG, which reduced Q1 EPS by approximately 0.13. As these integration headwinds fade in the second half of the year, the acquired top-line volume is expected to flow through to net income.

- Perpetual Productivity Improvement (PPI): Operating efficiency gains driven by corporate cost-control initiatives and associate-facing AI tools are projected to keep the full-year adjusted operating margin stable between 11.6% and 11.8%, helping insulate EPS from macro-driven gross margin compression.

Headwinds: Factors Capping EPS Upside

Analysts point out that significant upward revisions to EPS over the next twelve months face two primary macroeconomic constraints:

- Sustained High Interest Rates and Subdued Housing Turnover: Prolonged pressure on existing home sales continues to depress discretionary, big-ticket DIY categories like major kitchen and bath remodels. The lack of recovery in these high-margin categories acts as a structural drag on profitability.

- Promotional Intensity: To sustain its full-year comparable store sales guidance of flat to up 2%, the company may need to rely on increased promotional discounting within a highly competitive retail environment, potentially squeezing net margins.

Overall, Lowe’s EPS outlook for the coming year reflects a period of transition where top-line expansion from strategic acquisitions is counterbalanced by near-term margin consolidation, shifting the earnings growth engine from organic DIY spending to targeted Pro market share gains.

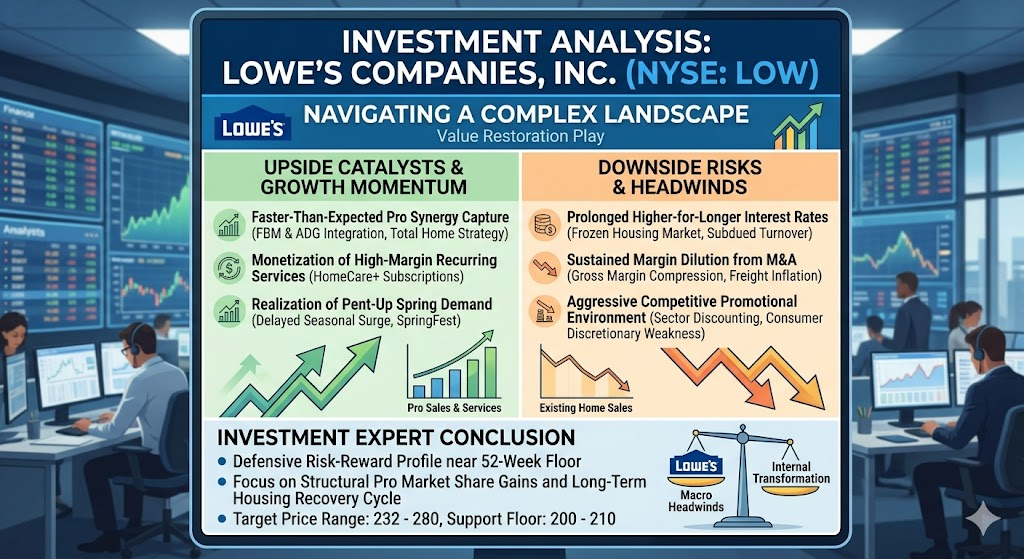

Lowe’s Companies, Inc. (NYSE: LOW) is currently navigating a distinct “macroeconomic crosswind balanced by internal structural transformation.” Following the Q1 2026 earnings release, the stock has been consolidating around the 215 to 221 range, trading close to its 52-week low of approximately 208, and reflecting a year-to-date decline of about 8.6%.

At these levels, LOW trades at a forward P/E of roughly 18.4x, which represents an approximate 13% valuation discount relative to its primary peer, Home Depot (HD). Synthesizing the latest post-earnings commentary from major sell-side firms (including Morgan Stanley, Barclays, Mizuho, and Telsey Advisory Group), the potential upside and downside framework for the stock over the next 12 months shapes up as follows:

Potential Upside Catalysts — Target Price Range: 232 to 280

If internal execution outpaces macro headwinds and the broader housing market begins to stabilize, the upward re-rating will be driven by:

- Faster-Than-Expected Pro Synergy Capture: Through the integration of Foundation Building Materials (FBM) and Artisan Design Group (ADG), Lowe’s is aggressively expanding into the lower-margin but high-volume commercial and production residential repair sectors. Successful cross-selling in the second half of the year will allow the company to leverage fixed costs on expanded top-line volume.

- Monetization of High-Margin Recurring Services: The newly launched HomeCare+ subscription program (99 annual fee) represents a structural shift. If adoption trends mirror the digital AI assistant (MyLowe), which is converting at three times the rate of standard traffic, it could inject high-margin recurring revenue into the mix, expanding the company’s blended valuation multiple.

- Realization of Pent-Up Spring Demand: If the severe weather headwinds from February translate into a powerful, delayed seasonal surge during Q2 and Q3, amplified by the SpringFest promotion, comparable store sales could surprise toward the upper bound of management’s 2% guidance.

Potential Downside Risks — Support Floor Range: 200 to 210

Conversely, if macroeconomic constraints tighten, downward pressure on the stock will stem from:

- Prolonged Higher-for-Longer Interest Rates: If interest rate relief is continually deferred, existing home sales volumes will remain locked up. This structurally freezes discretionary, big-ticket DIY capital deployment (such as major kitchen and bath remodels), capping Lowe’s highest-margin organic growth segment.

- Sustained Margin Dilution from M&A: The 70-basis-point contraction in Q1 gross margin highlights near-term integration friction. Research firms like Mizuho caution that if freight inflation and promotional discounting intensify through Q2, any delay in the second-half operating margin recovery (targeted at 11.6% to 11.8%) will trigger downward EPS revisions.

- Aggressive Competitive Promotional Environment: If general consumer discretionary spending weakens further, the home improvement retail sector may pivot toward aggressive promotional discounting to protect market share, compromising net margins.

Investment Expert Conclusion

- Risk-Reward Assessment: Trading near its 52-week floor, LOW offers a highly defensive risk-reward profile. The downside is fundamentally cushioned by its 42-year track record of consecutive dividend increases (yielding roughly 2.2%) and strong free cash flow generation.

- Tactical Perspective: Lowe’s currently functions as a “value restoration” play. Near-term explosive growth remains capped by the broader housing freeze, explaining the wide divergence in Wall Street sentiment (ranging from RBC’s conservative target downward revision to 232, to Telsey’s more optimistic 280). For investors prioritizing capital preservation, structural Pro market share gains, and an entry point positioned for the eventual housing recovery cycle, the current valuation provides strong downside protection.

Source:

Back to Lowe page