Booking Holdings reported its first quarter 2026 financial results in late April, showing resilience despite challenges from the Middle East conflict, with both revenue and earnings exceeding market expectations. Note that the company has completed a 25-for-1 stock split.

Below is the summary of the Q1 2026 financial results:

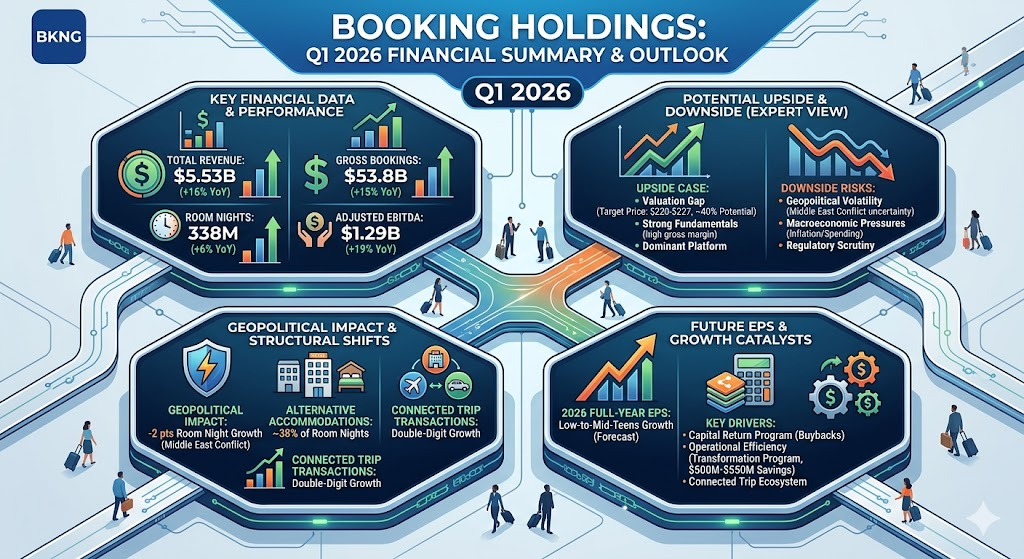

Key Financial Data

| Item | Value | YoY Growth |

| Revenue | 5.53B USD | 16% |

| Gross Bookings | 53.8B USD | 15% |

| Room Nights | 338M | 6% |

| Adjusted EBITDA | 1.29B USD | 19% |

| GAAP Net Income | 1.08B USD | 225% |

| Adjusted EPS | 1.14 USD | 14% |

Business Highlights and Geopolitical Impact

- Geopolitical Headwinds: The company estimated that the Middle East conflict negatively impacted room night growth by approximately 2 percentage points in Q1. Excluding this impact, room night growth would have been approximately 8%.

- Market Performance: The U.S. market showed strong performance with low-double-digit growth, while regions outside the U.S. were relatively softer.

- Strategic Progress:

- Alternative accommodations (vacation rentals, etc.) rose to approximately 38% of the room night mix.

- Mobile app penetration remains strong, sustained in the above 50% range.

- The Connected Trip initiative continues to see double-digit transaction growth.

Capital Allocation and Outlook

- Capital Allocation: The company executed 3.6B USD in share repurchases during the quarter.

- Outlook: The company expects the impact of the Middle East conflict to persist through the end of June. For Q2 2026, room night growth is forecasted between 2% and 4%, with revenue, gross bookings, and adjusted EBITDA expected to grow by 4% to 6%.

In Booking Holdings’ first quarter 2026 results, several key strategic and operational shifts stood out compared to previous quarters:

1. Capital Structure: Completion of Stock Split

The company officially completed a 25-for-1 stock split. This adjustment was designed to lower the barrier to entry for individual investors, aiming to improve liquidity and retail participation.

2. Quantifying Geopolitical Risks

Management provided a specific quantification of geopolitical headwinds for the first time. They noted that the Middle East conflict negatively impacted room night growth by approximately 2 percentage points. This indicates that, excluding these external shocks, the company’s underlying core growth momentum remained at a healthy 8% level, reflecting more precise control over its business performance despite regional instability.

3. Structural Shifts in Business Mix

- Rise in Alternative Accommodations: The share of room nights from vacation rentals and non-hotel accommodations reached 38%. This highlights the company’s continued success in capturing market share in non-traditional lodging, narrowing the gap with competitors like Airbnb.

- Deepening of the Connected Trip: Transactions under the Connected Trip initiative maintained double-digit growth. This confirms the company’s shift from a simple booking engine toward a comprehensive travel ecosystem where customers integrate flights, car rentals, and lodging to increase transaction frequency and stickiness.

4. Divergent Market Performance

The results revealed a clear regional disparity, with the U.S. market delivering low-double-digit growth, significantly outperforming international markets. This gap reflects varying levels of consumer spending power and economic recovery paces across different regions, serving as a key indicator for how global travel demand is currently evolving.

5. High-Intensity Capital Return Program

Despite external uncertainties, the company executed 3.6B USD in share repurchases during the quarter. This underscores management’s confidence in the company’s robust cash flow generation and long-term intrinsic value, prioritizing shareholder returns even amidst global macro headwinds.

Booking Holdings’ outlook for the second quarter (Q2) of 2026 is characterized by a cautious stance due to the ongoing geopolitical climate. Below is a summary of the growth drivers and forward guidance for Q2:

1. Growth Guidance (Q2 2026)

Management has issued conservative guidance for the second quarter, anticipating a slowdown compared to the robust performance in Q1:

- Room Nights: Expected growth of 2% to 4% year-over-year.

- Gross Bookings: Expected growth of 4% to 6%.

- Revenue and Adjusted EBITDA: Both projected to grow by 4% to 6%.

2. Key Growth Variables & Headwinds

- Geopolitical Impact: The primary factor tempering Q2 expectations is the Middle East conflict. Management assumes the direct and indirect effects of this situation will persist through the end of June. This was the primary driver for a downward revision in full-year guidance during the Q1 earnings call.

- Recovery Assumptions: The outlook is built on the premise that, following the anticipated pressure through June, global travel demand will begin a recovery phase in the second half of the year.

- Strategic Investments: The company continues to prioritize long-term growth through the “Connected Trip” initiative, AI-driven platform enhancements, and global market expansion. These investments are intended to drive customer loyalty and operational efficiency, even if macroeconomic headwinds persist in the short term.

3. Market Focus Areas

- Regional Performance Gap: Investors are closely watching whether the strength in the U.S. market (which saw low-double-digit growth in Q1) can continue to offset softer performance in international markets affected by geopolitical instability.

- Margin & Efficiency: With revenue growth moderating, the market is monitoring how the company leverages AI and its transformation program to maintain EBITDA margins. The company aims for margin expansion of 0 to 25 basis points for the full year.

- Regulatory Environment: Ongoing scrutiny from European regulators remains a key external risk that could impact the company’s platform positioning and commercial flexibility.

Summary

Booking Holdings is currently operating with a “defend and transform” strategy. In the short term, Q2 growth is clearly capped by geopolitical uncertainty. However, management maintains that the fundamental drivers of travel demand remain intact, and they are leveraging the company’s financial strength (including record share repurchases) to sustain long-term competitive advantages through AI and platform integration.

The outlook for Booking Holdings’ (BKNG) EPS over the next year is shaped by a mix of resilient core demand, ongoing operational restructuring, and the resolution of regional geopolitical headwinds.

1. 2026 Earnings Forecast

- Consensus Estimates: Analysts currently project a full-year 2026 EPS of approximately 10.70 USD to 10.82 USD. This figure accounts for the 25-for-1 stock split implemented on April 6, 2026.

- Growth Trend: While the first half of the year is characterized by volatility and lower-than-expected guidance due to the Middle East conflict, analysts anticipate an earnings recovery trajectory. The EPS is expected to grow by roughly 17% to 24% per annum over the next three years as the company scales its AI-driven platform and benefits from normalized travel demand.

2. Primary EPS Drivers

- Capital Return Program: The company’s record-setting share buyback program remains a major catalyst for EPS expansion. By significantly reducing the share count, Booking effectively boosts earnings per share even if net income growth remains steady.

- Operational Efficiency: The ongoing “Transformation Program” aims to achieve annual savings of 500M to 550M USD. As these structural cost reductions take hold throughout 2026, they are expected to expand operating margins, which are forecasted to reach approximately 32.8%.

- Connected Trip Strategy: The shift toward a comprehensive “Connected Trip” ecosystem is intended to increase customer lifetime value and transaction frequency, which should support higher revenue per user and stronger bottom-line results once geopolitical disruption subsides.

3. Key Risks to the Outlook

- Geopolitical Volatility: The current EPS guidance is highly sensitive to the duration of the conflict in the Middle East. Management expects the pressure on room-night growth to persist through June 2026; any escalation beyond this timeline could lead to further adjustments in full-year earnings expectations.

- Macroeconomic Headwinds: Higher energy costs and broader inflationary pressures continue to weigh on consumer travel budgets, particularly in international markets, potentially moderating the pace of demand recovery.

- Regulatory Scrutiny: As a global platform, Booking faces ongoing scrutiny from regulators in Europe and elsewhere regarding market dominance and data practices, which may impose additional compliance costs or necessitate changes to their commercial model.

Summary

The market outlook for BKNG remains generally optimistic, with a “Strong Buy” consensus among many analysts. The prevailing view is that the recent stock price drawdown—driven by conservative Q2 guidance—has created a valuation disconnect, as the underlying business continues to demonstrate high gross margins (around 87%) and robust cash flow generation. The path to higher EPS in 2027 and beyond is largely predicated on the assumption that global travel demand will normalize and the company will successfully leverage its AI-driven efficiencies to capture greater market share.

As of late May 2026, Booking Holdings (BKNG) is navigating a period of heightened volatility, with its stock price recently hitting a 52-week low near $150–$155 per share. Here is an expert breakdown of the potential upside and downside scenarios:

1. Upside Potential: “The Valuation Gap”

Analysts generally view the stock as significantly undervalued, pointing to a consensus price target in the $220–$225 range, which implies an upside potential of approximately 40% from current levels ($159.68).

- Strong Fundamentals: The company maintains an impressive ~87% gross margin and robust free cash flow, which some valuation models value at an intrinsic price significantly higher than the current market price (with some DCF models suggesting fair values exceeding $300).

- Capital Return Engine: Booking’s aggressive share buyback program—including a $3.6B execution in Q1 alone—serves as a powerful tailwind for EPS growth by consistently reducing the share count.

- Platform Dominance: The “Connected Trip” strategy and AI-driven platform enhancements are viewed as long-term competitive advantages that will likely lead to margin expansion once macro conditions normalize.

2. Downside Risks: “The Geopolitical Headwind”

The primary reason for the stock’s recent ~27% year-to-date decline is the uncertainty surrounding the Middle East conflict, which management explicitly cited as a drag on Q2 growth.

- Guidance Sensitivity: The company’s conservative Q2 outlook (2–4% room night growth) is a clear departure from previous years. If the conflict extends beyond June or escalates, it could force further guidance revisions, putting pressure on the stock to re-test its $150 floor.

- Macroeconomic and Regulatory Pressures: Global travel demand is sensitive to consumer spending resilience. Additionally, regulatory scrutiny in Europe regarding Booking’s platform practices remains a “hidden” risk that could impact future commercial flexibility and operational costs.

Summary Analysis

| Metric | Status / Outlook |

| Current Price | ~$160 |

| Consensus Price Target | ~$224 (+40% potential) |

| Analyst Sentiment | Strong Buy / Buy (among 37 analysts, 0 Sells) |

| Primary Catalyst | Q2 earnings (late July) – stabilization of H2 outlook |

Expert Perspective:

The prevailing view on Wall Street is that the current sell-off is a valuation dislocation rather than a structural breakdown of the business. Investors are currently pricing in a “worst-case” geopolitical scenario.

- For Long-term Investors: The current price is widely seen as an entry point for those betting on the resilience of global travel and the company’s ability to leverage AI for efficiency.

- For Short-term Traders: The stock is likely to remain range-bound until the Q2 earnings release in late July. Management’s commentary on “stabilizing cancellations” or “H2 recovery” will be the primary signal for a potential trend reversal.

Disclaimer: Stock investments carry risks, and you should perform your own due diligence or consult with a professional advisor regarding your specific financial situation.

Source:

- https://s201.q4cdn.com/865305287/files/doc_financials/2026/q1/Q1-2026-BKNG-Earnings-Release.pdf

- https://simplywall.st/stocks/us/consumer-services/nasdaq-bkng/booking-holdings/news/assessing-booking-holdings-bkng-valuation-after-q1-earnings

- https://hk.investing.com/news/transcripts/article-93CH-1431262

- https://www.hstong.com/news/hk/detail/26042912104649867

- https://www.nasdaq.com/market-activity/stocks/bkng/analyst-research

Back to Booking page