Southern Copper Corporation (SCCO) latest financial performance summary (based on the Q4 and Full-Year 2025 results):

2025 Financial Performance Highlights

- Full-Year Revenue: 13.4B, up 17% YoY.

- Adjusted EBITDA: 7.8B, up 22% YoY.

- Full-Year Net Income: 4.3B, up 28% YoY.

Q4 2025 Financial Highlights

- Quarterly Revenue: 3.9B, an increase of 1.1B compared to the same period last year.

- Quarterly Net Income: 1.038B, up 65% YoY.

Operational Outlook

- Production Forecast: Copper production for 2026 is projected to be 911,400 tons, a 4.7% decrease compared to 2025.

- Key Projects: Continued advancement of the Tia Maria mining project.

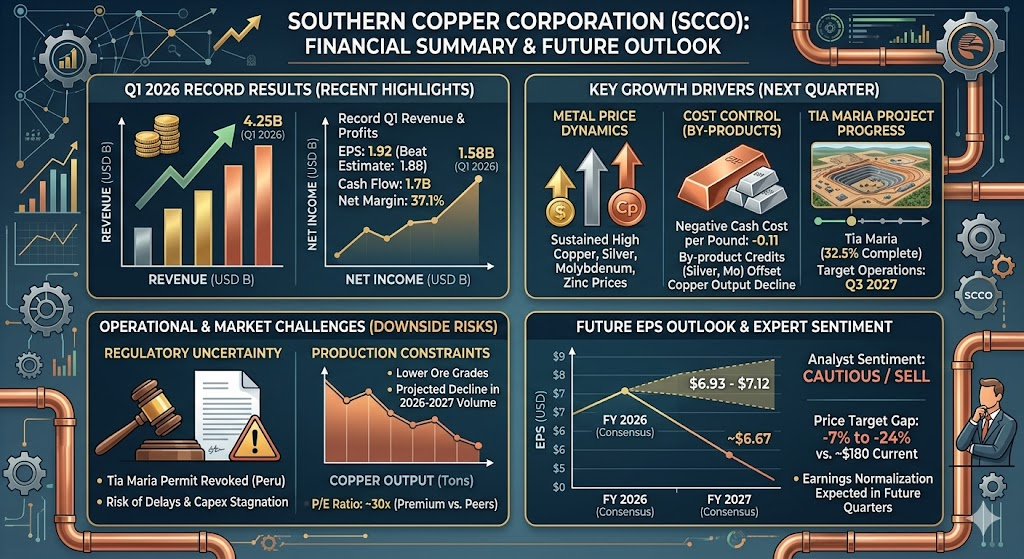

Southern Copper (SCCO) delivered record-breaking results in Q1 2026. Here are the key developments and financial highlights for the quarter:

1. Significant Financial Growth

- Record Revenue and Profits: Revenue reached 4.25B, a 36.2% increase year-over-year (YoY). Net income attributable to the company climbed to 1.58B, up 66.7% from 0.95B in the same quarter last year.

- EPS Performance: Earnings per share (EPS) stood at 1.92, exceeding the analyst consensus estimate of 1.88.

- Cash Flow and Dividends: Strong operating cash flow of 1.7B supported capital expenditures of 441.9M and cash dividend payments of 819.2M. The company announced a cash dividend of 1.00 per share and a 0.01 share stock dividend.

2. Operational Highlights and By-product Contribution

- Impact of By-products: Despite a 4.0% YoY decline in copper production due to lower ore grades in Peruvian mines, revenue growth was driven by higher metal prices and strong by-product performance.

- Silver: Production increased 11.1% YoY. With significant price appreciation, it has become the primary by-product, accounting for 12.5% of total revenue.

- Molybdenum: Production decreased slightly by 2%, though price levels remained supportive.

- Cash Cost Improvement: The cash cost per pound (net of by-product revenues) improved dramatically, shifting from 0.77 in the prior-year quarter to -0.11, demonstrating exceptional cost control and by-product profitability.

3. Major Events and Project Progress

- Tia Maria Project: The Tia Maria copper project has reached 32.5% completion. Following the reaffirmation of mining permits in April, the project remains on track to begin operations in Q3 2027.

- Management Change: Former Chairman and CEO Oscar González Rocha passed away in April 2026.

- Capital Expenditure: The company continues its ten-year capital investment plan, totaling over 20.5B, which encompasses various mining and infrastructure upgrade projects in both Peru and Mexico.

4. Market Sentiment

- Volatility: Despite the strong Q1 report, the stock has faced volatility recently. This is driven by analyst concerns regarding long-term copper price sustainability and a cautious outlook on the company’s current valuation, leading some institutions to maintain Reduce/Sell ratings.

The growth trajectory for Southern Copper (SCCO) is currently defined by a balance between short-term price benefits and long-term project-related uncertainties. Here are the core drivers for the coming quarters:

1. Short-Term Drivers (Price and Cost Advantages)

- Metal Price Dynamics: SCCO’s profitability is highly sensitive to the market prices of copper, silver, molybdenum, and zinc. Q1’s strong results reflect elevated prices across these commodities. Should these prices hold or climb due to continued supply constraints, revenue will remain robust in Q2 and beyond.

- Exceptional Cost Control: The cash cost of -0.11 per pound in Q1 demonstrates significant operational resilience. Even if copper prices experience a short-term correction, the company’s ability to rely on strong by-product (silver and molybdenum) prices ensures high margins (Q1 net margin reached 37.1%).

2. Mid-to-Long-Term Challenges (The Tia Maria Factor)

- Permit Uncertainty: The revocation of the Tia Maria construction permit by the Peruvian government earlier in 2026 remains the primary headwind. Although the company maintains its goal of reaching operation by 2027, this regulatory hurdle could lead to significant project delays.

- Capital Expenditure Burden: The company is committed to a ten-year investment plan totaling over 20.5B. Market attention will focus on the scale and pace of these expenditures. Any project stagnation—whether due to environmental regulations or local community resistance—would weigh on investor confidence regarding the company’s long-term production target of 1.6M tons by 2035.

3. Market Outlook

- Earnings Expectation Adjustments: Despite the earnings beat in Q1, analysts are divided on SCCO’s subsequent growth potential given its current valuation (trading at higher Price/Sales multiples compared to industry peers).

- Macroeconomic Headwinds: Ongoing US-China trade tensions and potential global slowdowns impacting copper demand remain critical external variables that will influence stock performance and demand outlooks in the coming quarters.

Summary

The key for SCCO in the next quarter is not “dramatic production growth” (as production remains constrained by declining ore grades and construction timelines) but rather the sustainability of its price-driven margins and the resolution of the Tia Maria permit dispute. Successfully resolving the permit issue would eliminate the market’s largest overhang and reignite the narrative for long-term value creation.

The trajectory of Southern Copper Corporation’s (SCCO) earnings per share (EPS) over the next year is currently characterized by high uncertainty, with market analysts projecting a potential normalization after a record-breaking first quarter in 2026.

1. EPS Projections for 2026 and 2027

According to recent consensus estimates from financial analysts:

- FY 2026 EPS Estimate: The consensus estimate sits in the range of $6.93 to $7.12 per share.

- FY 2027 EPS Estimate: Projections suggest a potential moderation to approximately $6.67 per share.

The Q1 2026 actual EPS was $1.92, significantly outperforming the market expectation of $1.80. However, analysts are factoring in a degree of “earnings normalization” as the year progresses.

2. Key Drivers Influencing EPS

- Copper Price Sensitivity: While SCCO’s profitability reached record levels due to elevated copper and by-product prices in Q1, the sustainability of these prices remains the most critical variable. Market volatility, influenced by Federal Reserve policy and global demand shifts, could impact margins.

- Production Volume Constraints: The company faces structural production headwinds. A decline in ore grades, particularly in its Peruvian operations, has led to projections of lower copper output for 2026 and 2027 compared to 2025 levels. Unless metal prices continue to surge, this volume decline exerts downward pressure on EPS.

- Tia Maria Project & Capital Expenditure: With over $20.5B in planned long-term capital investments, the company faces significant expenditure commitments. The uncertainty surrounding the Tia Maria project’s regulatory environment and the timing of its contributions to the bottom line (targeted for 2027) weigh on near-term earnings expectations.

3. Analyst Sentiment

- Consensus Rating: As of late May 2026, the aggregate analyst sentiment is notably cautious. A significant portion of analysts maintains a “Sell” or “Reduce” rating on the stock.

- Market Perception: Despite the strong Q1 earnings beat, many analysts believe the stock’s current share price has already priced in the near-term growth, leading to a disconnect between the company’s strong fundamental performance and its valuation, which trades at a premium compared to many industry peers.

Summary Table of Estimates (Consensus)

| Period | EPS Estimate |

| Full Year 2026 | $6.93 – $7.12 |

| Full Year 2027 | $6.67 |

Note: These estimates are based on current analyst consensus as of May 2026 and are subject to change based on commodity price fluctuations and regulatory updates regarding the Tia Maria project.

As a financial expert, my analysis of Southern Copper Corporation (SCCO) is that the stock currently exhibits a disconnect between its strong fundamental operational performance and its market valuation.

Based on data as of late May 2026, the stock presents a classic “priced-for-perfection” scenario, where significant risks are currently creating a high probability of downward volatility.

1. The Bear Case (Downside Risk)

The consensus on Wall Street is notably cautious, with many major firms (including Barclays, Scotiabank, Citi, and Morgan Stanley) maintaining “Sell” or “Reduce” ratings.

- Valuation Stretch: SCCO is currently trading at a P/E ratio of approximately 29x-31x, which is significantly higher than its 5-year historical average (approx. 22x) and its 10-year average (approx. 25x). This premium suggests that investors have already “priced in” aggressive earnings growth that may be difficult to sustain.

- Analyst Target Gap: The average 12-month analyst price target is approximately $144 – $167, which implies a potential downside of 7% to 24% from the current trading price of ~$180.

- Regulatory Overhang: The Peruvian government’s revocation of the Tía María copper project permit is a major structural risk. It injects political and operational uncertainty into the company’s $20.5B expansion pipeline, which is essential to justifying its premium valuation.

- Production Headwinds: Structural declines in ore grades in the Peruvian mines mean that even if copper prices remain high, the company’s ability to grow output volume in the next 12-24 months is limited.

2. The Bull Case (Upside Potential)

While the consensus is bearish, there is a “scarcity premium” narrative that could drive the stock higher if specific conditions are met:

- Structural Supply Tightness: If global copper demand—driven by AI data centers, power grid modernization, and EV infrastructure—continues to outpace supply as aggressively as current trends suggest, copper prices could remain at or above historical highs. This would continue to bolster SCCO’s bottom line, potentially forcing analysts to revise their price targets upward.

- By-product Fortress: SCCO’s ability to reach negative cash costs (net of by-products) due to high silver and molybdenum prices provides an unparalleled margin of safety. If precious and industrial metal prices strengthen, this “hidden” profitability could surprise the market again, as it did in Q1 2026.

Expert Summary

From a risk-reward perspective, SCCO currently looks like a “high-risk, high-expectation” stock.

- For the Tactical Investor: The stock is currently trading well above its fair value estimates, and the market appears to be ignoring clear warning signs regarding production headwinds and regulatory risks. There is a higher risk of a mean-reversion (downward adjustment) to align with historical valuation multiples.

- For the Long-term Holder: If you are holding for the structural “supercycle” in copper, the Tía María project remains the “make-or-break” catalyst. Resolution of the permit issue would likely provide the next major leg up, potentially pushing the stock toward the high-end analyst targets of $230–$244.

Recommendation: Exercise caution. If you are looking to enter or increase a position, waiting for a pullback toward the $145-$150 range—where the stock aligns better with analyst consensus and historical valuation—would offer a much more favorable risk-to-reward ratio.

Disclaimer: This analysis is based on market data as of May 24, 2026, and is for informational purposes only. It does not constitute personalized financial advice. Please consider your own risk tolerance before making investment decisions.

Source:

- https://www.sec.gov/Archives/edgar/data/1001838/000110465926052647/scco-20260331x10q.htm

- https://www.tradingview.com/news/tradingview:0ac2e2154ba83:0-southern-copper-corp-1q-2026-revenue-4-25b-eps-1-92-10-q-summary/

- https://www.marketbeat.com/stocks/NYSE/SCCO/earnings/

- https://seekingalpha.com/symbol/SCCO/earnings/estimates

- https://simplywall.st/stocks/us/materials/nyse-scco/future

- https://public.com/stocks/scco/earnings

Back to Southern Copper page