Honeywell (HON) released its Q1 2026 financial results on April 23, 2026. Below is the summary:

Financial Highlights (Q1 2026)

| Item | Data | Notes |

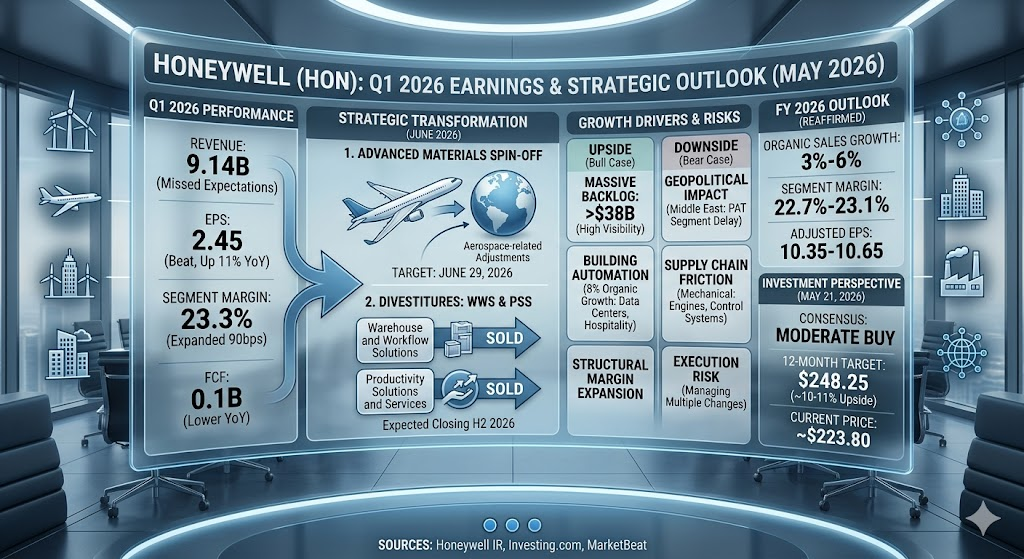

| Revenue | 9.14B | Below expectations of 9.28B, impacted by geopolitical factors |

| EPS | 2.45 | Beat expectations of 2.32, up 11% YoY |

| Segment Margin | 23.3% | Expanded by 90 basis points |

| Free Cash Flow (FCF) | 0.1B | Lower than 0.2B in Q1 2025 |

Business & Operational Highlights

- Revenue Growth: Organic sales grew by 2%, driven primarily by strong performance in Building Automation and Aerospace Technologies.

- Orders & Backlog: Organic orders grew by 7%, with a book-to-bill ratio of over 1.1 and a total backlog exceeding 38B.

- Strategic Divestitures: Announced the divestiture of the Productivity Solutions and Services (PSS) and Warehouse and Workflow Solutions (WWS) businesses, expected to close in the second half of 2026.

- Aerospace Spin-off: The company plans to complete the spin-off of the Advanced Materials business (Aerospace-related adjustments) by June 29, 2026.

- Geopolitical Impact: Performance in the Process Automation and Technology segment was constrained by Middle East tensions; the company anticipates this impact to broaden in the second quarter.

Full-Year 2026 Outlook (Reaffirmed)

The company maintained its full-year guidance for 2026:

- Revenue: 38.8B to 39.8B

- Organic Sales Growth: 3% to 6%

- Segment Margin: 22.7% to 23.1%

- Adjusted EPS: 10.35 to 10.65

Honeywell’s Q1 2026 earnings reflect a critical phase in the company’s organizational transformation. The most significant shifts during this quarter include:

1. Final Stages of Portfolio Transformation

This quarter marked the definitive move toward a leaner, more focused Honeywell:

- Divestitures: The company announced the sale of its Warehouse and Workflow Solutions (WWS) business to American Industrial Partners (AIP). Additionally, it is proceeding with the disposition of the Productivity Solutions and Services (PSS) business, with both transactions expected to close in the second half of 2026.

- Aerospace Spin-off: Honeywell confirmed the target completion date for the spin-off of its Advanced Materials business (Aerospace-related adjustments) is set for June 29, 2026, representing one of the most significant structural changes in the company’s recent history.

2. Resilient Profitability and Structural Margin Expansion

Despite facing geopolitical headwinds and revenue growth challenges, the company achieved structural improvements in profitability:

- Margin Expansion: Segment margins expanded by 90 basis points to 23.3%. This was driven by effective pricing strategies and an acceleration in cleaning up stranded costs ahead of the upcoming business spin-offs.

- Operational Efficiency: Management successfully utilized internal productivity actions to offset inflationary pressures, demonstrating disciplined cost management in a complex operating environment.

3. External Challenges and Divergent Market Demand

Operational performance this quarter was notably impacted by external pressures:

- Geopolitical Headwinds: Tensions in the Middle East created transitory negative impacts on the Process Automation and Technology segment, specifically causing delays in catalyst loading and service upgrades.

- Supply Chain Constraints: While the Aerospace Technologies sector saw robust demand (with organic order growth of 6% and a total backlog exceeding 38B), mechanical supply chain disruptions limited the output of engines and control systems.

- Growth Drivers: The Building Automation segment remained a standout performer, posting 8% organic revenue growth, primarily fueled by strong demand from data center projects and the hospitality sector.

Summary

The Q1 results characterize a quarter of “earnings outperformance against revenue headwinds.” Honeywell’s current core strategy focuses on simplifying the organization through divestitures and spin-offs, while leveraging its massive backlog to navigate geopolitical uncertainty and maintain confidence in its full-year guidance.

Honeywell’s growth outlook for the second quarter and the remainder of 2026 focuses on navigating short-term volatility while capitalizing on structural tailwinds.

Q2 Growth Outlook (2% to 4% Organic Sales Growth)

Management has taken a cautious approach to Q2, forecasting organic sales growth of 2% to 4% due to specific operational headwinds:

- External Resistance: The primary pressure is on the Process Automation and Technology (PAT) segment. Geopolitical tensions in the Middle East have delayed service upgrades and catalyst orders. Management specifically noted that the absence of this high-margin revenue will create a larger impact in Q2.

- Profitability Pressure: Due to the shifting product mix (e.g., lower high-margin catalyst sales) and rising logistics and operational costs driven by geopolitical instability, the company expects segment margins to temporarily adjust to a range of 22.2% to 22.5%.

Second Half and Full-Year Growth Drivers

Despite the short-term fluctuations in Q2, Honeywell reaffirmed its full-year organic sales growth guidance of 3% to 6%, supported by these key levers:

- Massive Backlog: With a total backlog exceeding 38B, the company has exceptional visibility into future revenue. Management emphasizes that as supply chain constraints ease after Q2, these orders will convert more effectively into actual performance.

- Building Automation: This remains one of the company’s strongest growth engines. Driven by data center construction and a sustained recovery in the hospitality sector, this segment posted 8% organic growth in Q1 and is expected to continue acting as a stabilizer for annual performance.

- Robust Aerospace Performance: Although mechanical supply chain bottlenecks impacted Q1, order activity remains strong. Following the targeted spin-off of the Advanced Materials business on June 29, 2026, the remaining aerospace operations will be more independent and focused, facilitating improved operational efficiency.

- Organizational Simplification: Through the divestiture of non-core assets (WWS and PSS), Honeywell expects to further reduce stranded costs in the second half of the year. This will allow the company to focus exclusively on high-growth, high-margin automation and aerospace markets.

Summary

Honeywell’s strategy centers on “weathering the Q2 geopolitical turbulence” while relying on its massive backlog and a leaner, post-transformation organization to accelerate growth in the second half of the year. Market analysts generally maintain a neutral-to-buy outlook, with a primary focus on how the company will utilize resource optimization after the spin-off to achieve its full-year EPS guidance of 10.35 to 10.65.

Honeywell’s trajectory for Adjusted EPS in fiscal year 2026 remains strong, supported by structural transformation and operational discipline. Here are the key data points and strategic drivers:

2026 Full-Year EPS Targets

The company reaffirmed its full-year guidance, signaling confidence in its ability to navigate short-term headwinds:

- Target Range: 10.35 to 10.65.

- Growth Rate: Represents an approximate 6% to 9% year-over-year increase.

- Market Consensus: Wall Street analysts generally estimate 2026 EPS around 10.50, aligning with the midpoint of the company’s guidance.

Drivers of EPS Trajectory

Management’s confidence in achieving these targets is built on three primary pillars:

- Structural Transformation (Spin-offs and Divestitures): The upcoming spin-off of the Advanced Materials business (targeted for June 29, 2026) and the divestiture of WWS and PSS businesses are designed to simplify the organizational structure. This reduces “stranded costs” and allows for a sharper focus on higher-margin core businesses, which is accretive to EPS over the long term.

- Robust Backlog Conversion: As of Q1 2026, the company’s total backlog exceeds 38B. This provides high visibility into future revenue and serves as the primary foundation for EPS stability throughout the remainder of the year.

- Operational Profitability: Despite Q1 revenue slightly missing expectations, the company delivered an EPS of 2.45, beating the consensus estimate of 2.33. This demonstrates the effectiveness of Honeywell’s pricing power and internal productivity actions in maintaining profitability under pressure.

Risks and Monitoring Factors

While the annual outlook remains unchanged, investors should monitor the following factors that could impact the pace of EPS realization:

- Geopolitical Impact: Q1 results indicated that tensions in the Middle East negatively impacted the high-margin Process Automation and Technology (PAT) segment. This pressure is anticipated to persist into Q2.

- Post-Spin-off Transition: As the aerospace-related business units are separated mid-year, the market will closely observe the profitability of the “new” Honeywell and its ability to maintain synergy efficiencies.

- Supply Chain Constraints: Mechanical supply chain bottlenecks continue to limit the speed of conversion from order to revenue. While management expects this to alleviate in the second half of the year, it remains a variable for short-term quarterly performance.

Summary

Honeywell is currently on a path of “organizational simplification and margin expansion.” The EPS guidance reflects strong confidence that, once the temporary geopolitical headwinds subside and the business divestitures are finalized, the company will see an acceleration in operational efficiency and earnings power in the second half of 2026.

Market Overview and Valuation

- Current Stock Price: ~$223.80 (as of May 21, 2026).

- Analyst Consensus: The stock is widely rated as a Moderate Buy.

- Target Price: The consensus 12-month price target is approximately $248.25, implying a potential upside of roughly 10% to 11% from current levels.

- Valuation: Honeywell currently trades at a P/E ratio of approximately 34.9x. While this reflects a premium compared to some traditional industrial peers, it is consistent with the market’s expectation for the company’s high-tech automation and aerospace growth.

Upside Potential (The Bull Case)

- Strategic Portfolio Transformation: The market is optimistic about the upcoming spin-off of the Aerospace division (scheduled for June 29, 2026) and the divestiture of the Warehouse and Workflow Solutions (WWS) and Productivity Solutions and Services (PSS) units. These moves are designed to reduce “stranded costs” and sharpen the company’s focus on high-margin segments, which could lead to a valuation re-rating.

- Backlog Strength: A robust backlog exceeding $38 billion provides exceptional revenue visibility. As supply chain constraints in the mechanical and engine segments ease throughout the remainder of 2026, this backlog is expected to convert into stronger top-line growth.

- Growth Verticals: Honeywell’s strong positioning in data center automation, defense, and AI-enabled building management systems remains a core growth driver, helping offset short-term cyclical volatility.

Downside Risks (The Bear Case)

- Geopolitical Sensitivity: The company is currently facing transitory headwinds in the Process Automation and Technology (PAT) segment due to conflicts in the Middle East, which have delayed service upgrades and catalyst shipments. Further escalation could extend this pressure into the second half of the year.

- Supply Chain Friction: Mechanical supply chain bottlenecks have periodically constrained the company’s ability to maximize output in its aerospace and control systems segments, preventing faster revenue acceleration.

- Execution Risk: The concurrent management of business divestitures and an aerospace spin-off introduces significant operational complexity. Investors are closely watching to ensure the “new” Honeywell maintains its margin expansion targets (22.7%–23.1%) during this transition period.

Investment Perspective

Honeywell is currently viewed as a “transformation play.” Investors are largely looking past short-term Q2 volatility to the benefits of a streamlined, more efficient entity post-spin-off.

- For the Long-Term Investor: The current price sits comfortably within a healthy range compared to its 52-week high of ~$248. The consensus price target suggests that if the company successfully executes its June spin-off and hits its FY2026 EPS guidance of $10.35–$10.65, there is meaningful room for the stock to appreciate toward its fair value.

- Near-Term Caution: The stock may face consolidation or modest pressure until the June 29th spin-off is completed and investors receive clearer guidance on the post-separation operational structure.

Disclaimer: This analysis is for informational purposes only and does not constitute financial advice. All investments involve risk; please conduct your own due diligence or consult with a financial advisor before making investment decisions.

Source:

- https://honeywell.gcs-web.com/

- https://www.investing.com/news/transcripts/earnings-call-transcript-honeywell-q1-2026-beats-eps-expectations-stock-dips-93CH-4632969

- https://www.honeywell.com/us/en/press/2026/04/honeywell-reports-first-quarter-results-and-reaffirms-2026-outlook-announces-sale-of-warehouse-and-workflow-solutions

- https://www.investing.com/news/company-news/honeywell-q1-2026-slides-margin-gains-shine-amid-revenue-headwinds-93CH-4633218

- https://www.marketbeat.com/instant-alerts/honeywell-international-nasdaqhon-releases-fy-2026-earnings-guidance-2026-04-23/

Back to Honeywell page