Boeing (BA) reported its first quarter 2026 financial results on April 22, 2026, for the quarter ended March 31, 2026. Driven by a recovery in commercial airplane deliveries and stability in the defense sector, both revenue and net loss performed better than market expectations, showcasing operational recovery momentum.

Here is the executive summary of the Q1 2026 financial results:

Core Financial Metrics

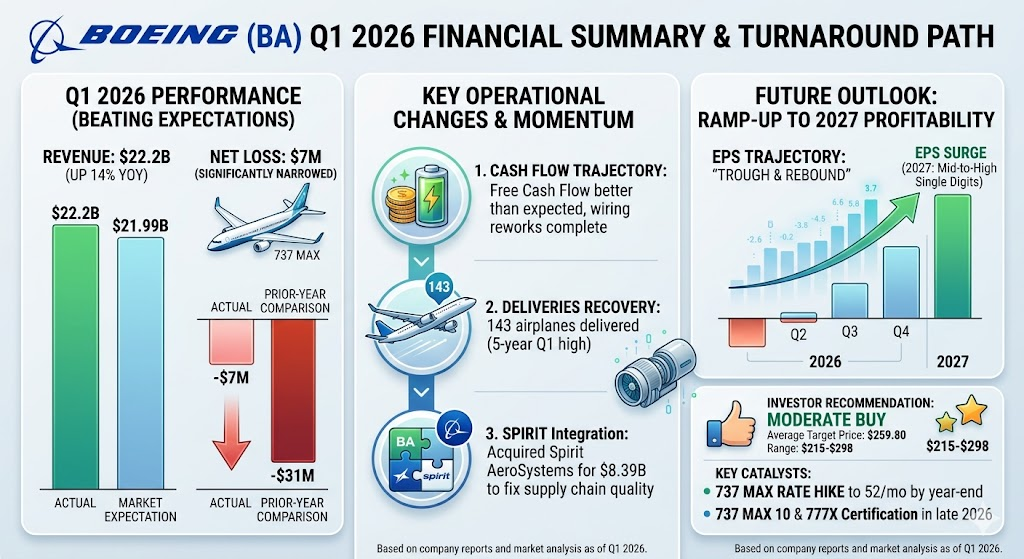

- Revenue: $22.217B, up 14% year-over-year compared to $19.496B in the prior-year period, beating market expectations of $21.99B.

- Net Loss (GAAP): $7M, narrow significantly compared to a net loss of $31M in the same quarter last year.

- EPS (GAAP): Loss of $0.11 per share.

- Core EPS (Non-GAAP): Loss of $0.20 per share, significantly beating market consensus estimates of a loss between $0.66 and $0.83 per share.

- Free Cash Flow (Non-GAAP): Negative $1.454B. Although remaining in a net outflow position, it was substantially better than the negative $2.6B previously estimated by the market.

- Total Backlog: Reached a record high of $695B, including over 6,100 commercial airplanes.

- Debt Position: Total debt decreased to $47.2B, a reduction of $6.9B during the quarter. Cash and marketable securities totaled $2.09B.

Segment Performance

1. Commercial Airplanes

- Revenue: $9.203B, a 13% increase year-over-year.

- Operating Loss: $563M (compared to a loss of $537M in the prior-year period), with an operating margin of negative 6.1%.

- Deliveries: Delivered 143 airplanes during the quarter, up 10% year-over-year, marking the highest first-quarter delivery since 2019. Net orders for the quarter stood at 140 airplanes.

- Production & Timeline: 737 production remained steady at 42 per month, with plans to increase to 47 per month by year-end. Certification for the 737 MAX 7 and MAX 10 is anticipated by late this year, with deliveries scheduled for 2027. 787 production is stable at 8 per month, though short-term output remains constrained by seat and interior cabin component shortages.

2. Defense, Space & Security

- Revenue: $7.599B, up 21% year-over-year.

- Operating Profit: $233M, up 50% year-over-year, with the operating margin improving to 3.1%.

- Highlights: Growth was driven by increased global defense spending and execution stability. Milestones included the successful launch of the NASA Artemis II Moon mission SLS rocket, alongside ongoing momentum from the previously secured F-47 sixth-generation fighter contract and F-15EX programs.

3. Global Services

- Revenue: $5.370B, up 6% year-over-year.

- Operating Profit: $971M, with an operating margin of 18.1% (slightly down from 18.6% last year due to the divestiture of the high-margin subsidiary, Jeppesen).

- Highlights: Signed its largest-ever landing gear exchange program agreement with the Singapore Airlines Group, bringing the segment backlog to a record $33B.

Outlook and Management Commentary

CEO Kelly Ortberg stated that the company achieved a solid start to the year, with operations steadily improving and heading in the right direction.

- Free Cash Flow Guidance: Boeing reiterated its full-year 2026 guidance, expecting positive free cash flow of $1.0B to $3.0B.

- Profitability Timeline: Despite the visible recovery, management delayed the timeline for the Commercial Airplanes segment to return to profitability (positive operating profit) to 2027.

- Near-Term Challenges: Supply chain constraints (such as 787 engine and interior delivery delays), rework required on early-production MAX models due to wiring issues, and the ongoing integration of Spirit AeroSystems remain the primary near-term headwinds.

During the Q1 2026 earnings call, Boeing disclosed several pivotal shifts that are reversing past operational slumps and reshaping the company’s trajectory:

1. Rapid Resolution of Wiring Issues & Sharp FCF Improvement

The most significant positive surprise for the market was the free cash flow performance (negative $1.454B, substantially beating expectations of negative $2.6B). This was primarily driven by Boeing’s rapid completion of reworks on early-production 737 MAX models that had been plagued by wiring issues. Combined with strong quarter-end collections, the company successfully put the brakes on cash burn, establishing a solid foundation to achieve positive cash flow for the full year.

2. Production & Deliveries Hit a 5-Year First-Quarter High

The Commercial Airplanes segment delivered tangible signs of recovery, handing over 143 aircraft during the quarter—a 14% year-over-year increase. This marks the strongest first-quarter delivery performance since the 2019 grounding crisis and the subsequent pandemic. Production of the core 737 program has stabilized at 42 jets per month, with plans to ramp up to 47 per month by summer and hit 52 per month by year-end.

3. Accelerated Integration of Spirit AeroSystems

Boeing is aggressively moving forward with the acquisition and operational integration of its key tier-1 supplier, Spirit AeroSystems (valued at an $8.389B purchase price). This strategic move aims to bring core manufacturing back in-house to fundamentally address the chronic quality control and supply bottlenecks of recent years, though it introduces short-term execution and balance sheet risks.

4. Defense Segment Emerging from Losses with Next-Gen Programs

After quarters of margin erosion driven by inflation on fixed-price contracts, the Defense, Space & Security (BDS) segment saw revenue surge 21% with operating margins recovering to 3.1%. Alongside the successful rollout of the SLS rocket for NASA’s Artemis II Moon mission, long-term momentum was reinforced by the previously secured F-47 sixth-generation fighter contract and Boeing’s selection as a finalist for the Navy’s F/A-XX fighter program.

5. Calibrated Timelines & Pushed-Back Profitability Guidance

Management provided a more pragmatic update regarding core program milestones and financial targets:

- 737 MAX 7 / MAX 10: Flight testing for the engine anti-ice system issue is underway. Certification is anticipated by late this year, but initial deliveries have been officially pushed to 2027.

- 777X Program: Certification testing continues as Boeing works closely with suppliers to resolve the 777X engine durability issues discovered during inspections last quarter.

- Delayed Segment Turnaround: Despite the broader operational rebound, management pushed back the timeline for the Commercial Airplanes segment to achieve positive operating profit to 2027, citing ongoing supply chain shortages (such as 787 engines and cabin seats), production ramp-up costs, and the Spirit integration.

Following the operational inflection point demonstrated in Q1 2026, Boeing’s management and market analysts (such as Citi and TD Cowen) are focusing on several core catalysts and growth drivers for the upcoming quarters.

Boeing’s 2026 financial performance is heavily back-end loaded, meaning that the majority of growth and cash flow acceleration will materialize as production ramps up through the summer and the second half of the year:

1. Core Program Production Ramps (Rate Hikes)

Revenue growth in the Commercial Airplanes (BCA) segment will be directly driven by the planned acceleration of manufacturing rates starting this summer:

- 737 MAX: Having stabilized at 42 aircraft per month this quarter, production is scheduled to ramp up to 47 per month this summer, with the year-end target remaining at 52 per month. This acceleration will drive delivery momentum to meet the company’s full-year commitment of delivering approximately 500 737 aircraft.

- 787 Dreamliner: Production is currently steady at 8 jets per month. As management works through short-term certification and supply chain bottlenecks related to seat and cabin interior components, delivery cadences are expected to pick up in the second half of the year, targeting 90 to 100 deliveries for the full year.

2. Certification Milestones and Flight Testing

Advancing the regulatory approval process for new variants is essential to unlocking the record backlog and securing long-term profitability:

- 737 MAX 7 and MAX 10: Dedicated flight testing is underway to address the engine anti-ice system issue that previously hindered progress. With the 737-10 advancing through Type Inspection Authorization (TIA 2), full FAA certification remains on track for late this year.

- 777X (777-9): Intensive certification flight testing continues. Boeing is collaborating closely with GE Aerospace to resolve the 777X engine durability issues discovered during inspections last quarter, making testing progress a focal point for the second half of the year.

3. High-Value Defense Ramps and Budget Appropriations

The Defense, Space & Security (BDS) segment secured $9.0B in new orders this quarter, boosting its specialized backlog to historic highs. Future momentum will be driven by:

- The winding down of cash drains and overruns associated with legacy fixed-price development contracts, which are expected to largely conclude within 2026, paving the way for operating margins to improve toward the high single-digits.

- Funding allocations from major defense programs transitioning into active production phases, including the next-generation F-47 fighter (allocated $5.0B), the KC-46 tanker ramp ($4.0B), and ongoing development for the Navy’s F/A-XX program.

4. Monetization of Historic Global Services Backlog

As a highly resilient driver of earnings and cash flow, the Global Services (BGS) segment holds a record backlog of $33B. Coming quarters will see initial revenue recognition from its largest-ever landing gear exchange contract with the Singapore Airlines Group. Furthermore, with global passenger yields and fleet utilization rates projected to remain elevated through 2026, demand for commercial aftermarket parts and modifications will remain robust.

5. Geopolitical Catalysts and Market Restarts

Analysts are closely monitoring the long-term positive catalyst of normalized, steady commercial aircraft deliveries to the Chinese market. Additionally, while geopolitical tensions in regions like the Middle East present broader market uncertainties, they have not disrupted Boeing’s commercial shipping schedule; conversely, heightened global security requirements continue to create potential upside for the defense portfolio.

Following the narrower-than-expected loss in Q1 2026, market consensus regarding Boeing’s Earnings Per Share (EPS) trajectory over the next year has shifted toward a clear “trough-and-rebound” narrative. Wall Street treats the remainder of 2026 as a critical operational pivot point, with the true bottom-line explosion projected for fiscal year 2027.

The expected path for Boeing’s Non-GAAP Core EPS unfolds as follows:

1. Fiscal Year 2026: Transitioning to the Black

Following consecutive years of steep annual losses, Boeing is expected to officially snap its losing streak in 2026, though the margin of profitability will remain thin as manufacturing lines undergo reorganization.

- Consensus Estimates: The consensus forecast for full-year 2026 Non-GAAP EPS currently sits in a tight band between $0.47 and $0.63. According to Zacks data, this represents a year-over-year earnings improvement of roughly 98.6%, signaling a definitive transition out of deep structural deficits.

- Quarterly Progression: Q2 earnings are projected to hover around the break-even mark or post a negligible loss. The bulk of fiscal year 2026 profitability is heavily back-end loaded, with visible EPS acceleration concentrated in Q3 and Q4 to match the back-half commercial delivery schedule.

2. Fiscal Year 2027: The Profitability Surge

The true normalization of Boeing’s earnings power is expected to manifest in 2027. Because the earnings baseline for 2026 is so low, consensus estimates point to a massive year-over-year surge (with Zacks modeling a mathematical bounce exceeding 2,800% off the low base).

- Analysts project that full-year 2027 EPS will leap into mid-to-high single-digit dollar territory. This coincides with expectations that total company revenue will surpass its historical peak to hit record territory sometime during 2027.

Core Drivers Shaping the Next 12 Months of EPS

The fulfillment of this EPS trajectory hinges directly on several operational variables:

- Operating Leverage via Production Ramps: The acceleration of 737 MAX production from 42 per month to 47 per month this summer, and an ultimate target of 52 by year-end, serves as the most immediate catalyst for EPS expansion. Higher output allows Boeing to spread substantial fixed overhead across more units, lifting depressed gross margins in the commercial segment.

- Winding Down Fixed-Price Contract Headwinds: The Defense, Space & Security (BDS) segment is gradually putting its cost-overrun liabilities behind it. The margin-eroding impacts of legacy fixed-price development contracts are slated to largely wrap up within 2026. As high-value programs like the F-47 and KC-46 mature into steady-state production, BDS will transition into a more consistent EPS contributor.

- Integration Dilution from Spirit AeroSystems: The ongoing acquisition and structural re-integration of Spirit AeroSystems poses a short-term cap on EPS upside. While critical for long-term quality assurance and supply chain containment, the near-term cash requirements and restructuring outlays will absorb capital that would otherwise drop to the bottom line over the next two to three quarters.

- Pushed-Back Derivative Deliveries: Because management has deferred initial deliveries of the 737 MAX 7, MAX 10, and the widebody 777X into 2027, these programs will act as a net drag on the next year’s EPS due to ongoing certification flight-test expenditures, deferring their multi-million dollar revenue milestones to the following fiscal cycle.

For a complex turnaround play like Boeing (BA), the investment thesis requires weighing near-term operational friction against long-term structural recovery.

Here is the strategic investment appraisal and upside analysis from an institutional and market-consensus perspective.

Wall Street Consensus: Moderate Buy

The overarching sentiment among institutional research firms remains cautiously optimistic. Out of 24 major analysts tracking the stock, 17 rate it a Buy/Strong Buy, 4 rate it a Hold, and 3 rate it a Sell.

- The Bull Case: Q1 2026 earnings confirmed an operational bottom. Free cash flow (FCF) burn slowed dramatically, and the total order backlog hit a record $695B. The Defense (BDS) segment has largely put legacy fixed-price contract losses behind it, and Global Services (BGS) remains a highly resilient cash generator.

- The Bear Case: Regulatory overhang persists. The FAA’s strict 42-per-month production cap on the 737 MAX limits immediate upside, and ongoing class-action safety litigation adds unquantifiable headline risk. Additionally, the mid-May announcement of a 200-jet order from China fell short of Wall Street’s whisper numbers of 500 jets, causing short-term technical fatigue in the stock.

Potential Upside Analysis

With the stock currently consolidating around the $215 to $222 range, Wall Street models project significant valuation expansion over the next 12 months:

- Consensus Target Price: $259.80 (reaffirmed by recent post-earnings updates from Citi and Morgan Stanley). This implies a baseline 12-month potential upside of 17% to 20%.

- Bull Case Target Price: $295.00 to $298.00 (modeled by firms like Bernstein and Tigress Financial). This assumes that summer production successfully transitions to 47 jets/month, the 777X engine issues are resolved, and full-year FCF hits the upper bound of management’s $1.0B to $3.0B guidance. This represents an upside of over 35%.

- Bear Case Floor: $140.00 to $212.00. The absolute bear case rests on the 200-day moving average failing to hold as a critical floor, which would only trigger if severe, unexpected supply chain disruptions derail the 2026 FCF guidance.

Strategic Recommendation: Accumulate on Weakness (Medium-to-Long Term)

Boeing is highly recommended for long-term value/turnaround portfolios (12–24 month horizon) that have the risk tolerance to absorb short-term headline volatility. It is not suitable for short-term momentum traders.

3 Reasons to Buy the Turnaround

- The Earnings Inflection: 2026 is a transition year where EPS is projected to edge back into positive territory ($0.47 to $0.63). The real catalyst is fiscal year 2027, where consensus models predict an exponential jump in EPS as the 737 MAX 10 and 777X enter formal delivery cycles.

- Supply Chain Containment: The $8.389B acquisition of Spirit AeroSystems creates short-term restructuring friction on the balance sheet, but fundamentally fixes the chronic structural quality-control issues that plagued the company for years.

- The Macro Cushion: Global defense budget expansions provide a highly predictable revenue floor for the BDS segment (backed by major next-gen programs like the F-47 and KC-46), offering an excellent hedge against cyclical commercial aviation risks.

Key Execution Metrics to Monitor

Before taking a position, look for two key validation signals in the next quarterly report: first, the formal lifting of the FAA production cap to support the summer rate hikes; second, a steady stabilization of cash flow proving that the legacy MAX wiring reworks are completely finalized.

Source:

- https://investors.boeing.com/investors/news/press-release-details/2026/Boeing-Reports-First-Quarter-Results/default.aspx

- https://www.sec.gov/Archives/edgar/data/12927/000162828026026391/a202603mar318kprex991.htm

- https://www.stocktitan.net/sec-filings/BA/10-q-boeing-co-quarterly-earnings-report-79404377486a.html

- https://www.binance.com/en/square/post/04-22-2026-boeing-s-q1-2026-revenue-exceeds-market-expectations-315254301532497

Back to Boeing page