Stage 1: Founding and Military Genesis (1916 – 1930s)

- Wooden Seaplanes and Early Innovation: William Boeing founded the company in Seattle in 1916, initially leveraging the Pacific Northwest’s abundant timber resources to construct twin-wing seaplanes.

- Airmail Contracts and Consolidation: During the 1920s, Boeing secured its financial footing by winning U.S. government airmail routes. The company grew rapidly, designing military fighters and bombers, and eventually formed a massive aviation conglomerate known as United Aircraft and Transport Corporation.

- Anti-Trust Divestiture: In 1934, under U.S. anti-trust legislation, the conglomerate was forced to break apart. Its airline operations became what is known today as United Airlines, while the manufacturing arm remained independent as the Boeing Airplane Company.

Stage 2: The Arsenal of Democracy and WWII Bombers (1939 – 1945)

- Mass Production for the War Effort: With the onset of World War II, Boeing shifted entirely to wartime production, turning its Seattle facilities into high-volume assembly lines.

- Legendary Heavy Bombers: Boeing designed and manufactured thousands of iconic heavy aircraft, notably the B-17 Flying Fortress and the B-29 Superfortress. These planes played a decisive role in both the European and Pacific theaters, establishing Boeing’s reputation for engineering large, multi-engine aircraft.

Stage 3: Entering the Jet Age and Commercial Dominance (1950s – 1970s)

- Pioneering Commercial Jets: Following the war, Boeing adapted its military jet technology for commercial use. The launch of the Boeing 707 in 1957 marked America’s first commercially successful passenger jet, transforming global travel and securing the market lead over British pioneers.

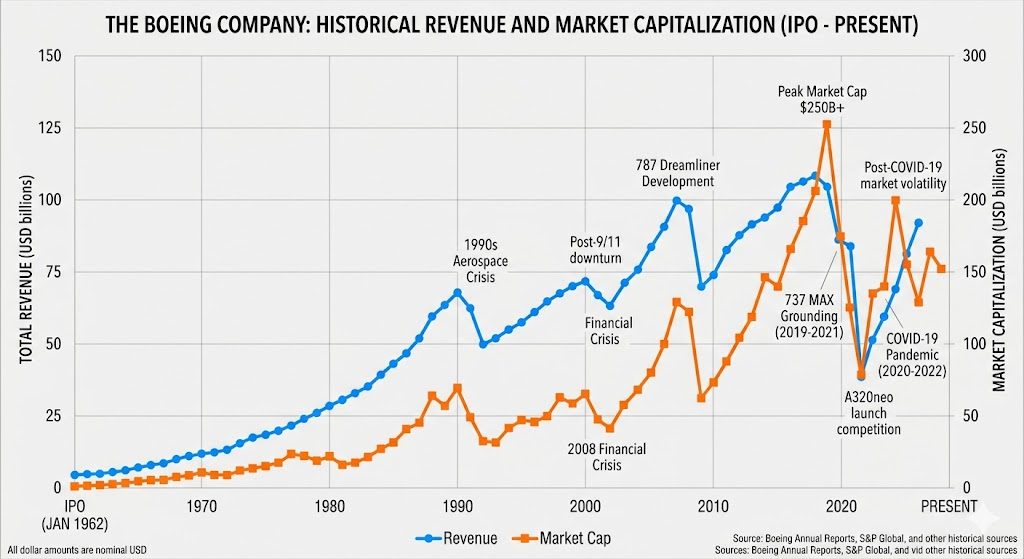

- The Queen of the Skies: In the late 1960s, Boeing took a massive financial gamble by developing the world’s first widebody twin-aisle airliner, the Boeing 747. The success of the “Jumbo Jet” allowed Boeing to monopolize long-haul international routes for decades.

- The Apollo Space Program: Concurrently, Boeing expanded into aerospace exploration, acting as a key contractor for NASA’s Apollo program by building the first stage of the Saturn V rocket.

Stage 4: Consolidation and the Global Duopoly (1980s – late 1990s)

- Fleet Diversification: Boeing built out a comprehensive product catalog, introducing highly successful single-aisle models like the 737 family, alongside advanced twin-engine widebodies including the 757, 767, and the digitally advanced 777.

- The McDonnell Douglas Merger: In 1997, Boeing executed a historic merger by acquiring its long-time domestic defense rival, McDonnell Douglas. This integration expanded Boeing’s military portfolio (bringing in platforms like the F/A-18), but also shifted corporate culture toward Wall Street-driven financial metrics.

- The Rise of Airbus: By the close of the decade, the global aviation landscape consolidated from several competing firms into a fierce, head-to-head duopoly between Boeing and Europe’s Airbus.

Stage 5: Global Supply Chains and the Dreamliner (2000s – 2018)

- The Dreamliner Strategy: In response to the superjumbo Airbus A380, Boeing wagered on mid-sized, highly efficient point-to-point travel, developing the carbon-composite Boeing 787 Dreamliner.

- Outsourced Manufacturing Risks: For the 787, Boeing shifted away from its traditional centralized manufacturing in Seattle, outsourcing major structural design and assembly globally. This strategy led to severe supply chain disconnects, design flaws, and multi-year delivery delays, culminating in early battery-related grounding issues.

- Peak Market Valuation: Despite these initial hurdles, the late 2010s saw Boeing achieve record revenue and market capitalization, driven by robust global travel demand and expanding aerospace programs.

Stage 6: Quality Rectification and Operational Stabilization (2019 – Present)

- The MAX Crisis: The global grounding of the 737 MAX following two tragic accidents in late 2018 and early 2019 severely impacted corporate revenue and institutional trust, offering Airbus an open window to expand its narrowbody market share.

- Pandemic and Supply Chain Headwinds: The subsequent global pandemic ground the commercial aviation sector to a halt, compounding factory quality-control issues and part shortages across the broader aerospace industry.

- Quality and Cultural Reset: Moving through the mid-2020s, Boeing initiated structural leadership transitions to refocus corporate strategy away from financial metrics and back toward manufacturing precision and engineering safety. The company continues to stabilize production lines for the 737 MAX and 787 families while steering the next-generation 777X through international certification pipelines.

Competitive Analysis

Boeing’s competitive landscape is primarily split across its two core business segments: Commercial Airplanes and Defense, Space & Security. In the commercial market, Boeing operates within a duopolistic rivalry, while in the defense sector, it goes head-to-head with established tier-one aerospace defense contractors.

1. Commercial Airplanes Segment

The global mainline commercial aircraft market is fundamentally a duopoly shared between Boeing and Airbus.

- Airbus — The Primary and Direct Competitor

- Narrowbody Market: The Airbus A320neo family, particularly the A321neo, has captured significant market share due to its fuel efficiency and cabin capacity, placing intense competitive pressure on the Boeing 737 MAX series. Although Boeing focused heavily on ramping up its 737 MAX production lines and stabilizing deliveries through early 2026, Airbus maintains a massive order backlog in this category. Airbus also leverages the A220 series to capture the smaller narrowbody segment, where Boeing lacks a direct, clean-sheet equivalent.

- Widebody Market: Boeing’s 787 Dreamliner and the developing 777X series compete directly against the Airbus A350 and A330neo. Historically, Boeing has held a strong position in the widebody and freighter markets, keeping this segment highly contested and evenly matched.

- Regional and Emerging Competitors

- Embraer: Dominates the regional jet market with its E-Jet E2 family. After a planned joint venture between Boeing and Embraer fell through, the two companies continue to operate independently in their respective market tiers.

- COMAC (Commercial Aircraft Corporation of China): The C919 narrowbody jet is expanding its commercial operations within China and actively pursuing international certifications. While it does not immediately disrupt the global duopoly, it represents a long-term challenger in key growth markets.

2. Defense, Space & Security Segment

In the military and aerospace sectors, Boeing competes for defense budgets from the U.S. Department of Defense and international allies against other major defense primes.

- Lockheed Martin

- As the largest global defense contractor, Lockheed Martin exerts significant pressure on Boeing’s tactical fighter business. The F-35 Lightning II program has largely secured the fifth-generation fighter market for the U.S. and allied nations, limiting the market expansion of Boeing’s fighter platforms like the F/A-18 Super Hornet and F-15EX. Lockheed and Boeing also compete fiercely in missile defense systems.

- Northrop Grumman

- Northrop holds deep capabilities in strategic deterrence, strategic bombers (such as the B-21 Raider), and advanced space systems. Boeing competes with Northrop in space exploration systems, satellite payloads, and autonomous unmanned aerial vehicles.

- RTX Corporation (formerly Raytheon Technologies)

- Through its Pratt & Whitney and Collins Aerospace businesses, RTX acts as a critical supplier of propulsion and avionics to Boeing. Simultaneously, its defense units compete with Boeing for contracts involving missile systems, radar networks, and electronic warfare capabilities.

- General Dynamics

- While General Dynamics focuses heavily on marine systems and land combat vehicles, its aerospace unit (Gulfstream) sets the standard for high-end business aviation, competing indirectly with Boeing Business Jets (BBJ) at the premium corporate level.

3. Core Strategic Dynamics

- Balanced Portfolio Advantages: Boeing benefits from a dual-engine corporate structure. When the commercial aviation cycle faces downturns, its stable, multi-year government defense contracts provide a financial buffer. The company possesses an extensive order backlog spanning nearly a decade of production capacity.

- Operational Execution Challenges: Overcoming production bottlenecks, supply chain constraints, and regulatory milestones for new models remains the critical hurdle. Boeing’s primary focus centers on demonstrating manufacturing quality, stabilizing delivery timetables, and accelerating certification schedules to prevent further market share loss to Airbus.

Source:

Back to Boeing page