Arista Networks Q1 2026 Earnings Summary

Financial Performance

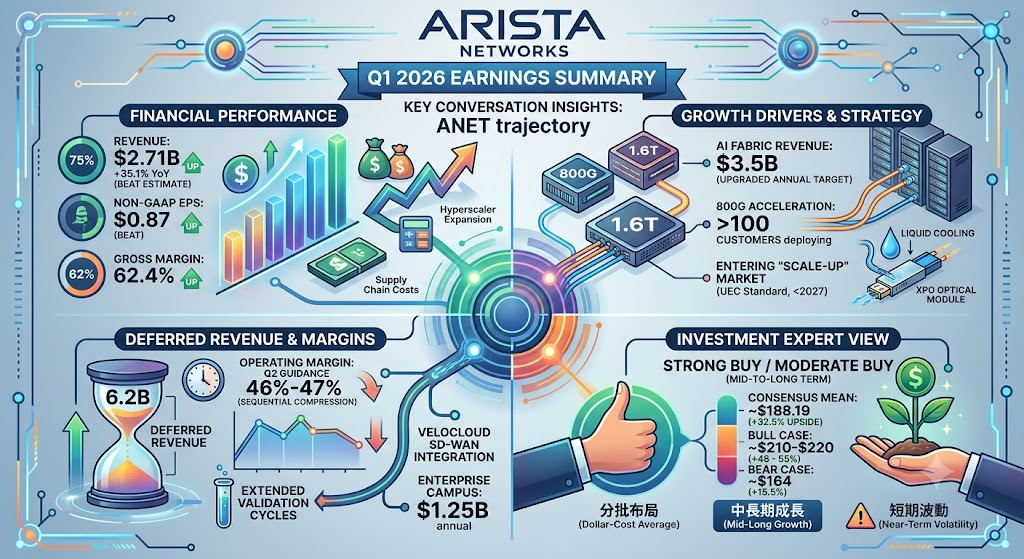

- Revenue: Reached 2.71B, up 35.1% year-over-year, beating market consensus of 2.61B. Product revenue contributed 2.31B, while services revenue brought in 397.7M.

- Gross Margin: GAAP gross margin stood at 61.9%; Non-GAAP gross margin was 62.4%. This represents a slight decline from 64.1% in the prior year’s quarter, driven by shifting customer mix and elevated supply chain costs.

- Operating Margin: GAAP operating margin recorded at 42.7%; Non-GAAP operating margin achieved 47.8%.

- Net Income & EPS: GAAP net income was 1.02B with a diluted EPS of 0.80 dollars. Non-GAAP net income came in at 1.11B, delivering a diluted EPS of 0.87 dollars, outperforming the Wall Street estimate of 0.81 dollars.

- Cash Flow & Balance Sheet: Operating cash flow reached 1.69B. Arista concluded the quarter with 12.35B in total cash, cash equivalents, and marketable securities. Deferred revenue rose to 6.2B.

Business & Product Highlights

- Market Leadership: Management highlighted that Arista has secured the top market share position in the high-speed Ethernet switching market for speeds of 10GbE and above.

- AI Networking Strategy: The company has now cleared more than 100 cumulative customers deploying its 800G Ethernet solutions, paving the way for a transition into 1.6T volume production by 2027.

- New Product Innovation: Introduced the XPO high-density, liquid-cooled pluggable optical module. Engineered for next-generation AI data centers, it cuts network rack space by up to 75% and reduces required floor space by 44% compared to legacy optical setups.

Future Outlook & Guidance

Q2 2026 Guidance

- Expected revenue is projected at approximately 2.8B, slightly ahead of the 2.78B consensus estimate.

- Non-GAAP operating margin is forecasted to land between 46% and 47%.

- Non-GAAP diluted EPS is anticipated to be around 0.88 dollars.

Full-Year 2026 Guidance Update

- Raised the full-year 2026 revenue guidance to 11.5B, translating to roughly 27.7% year-over-year growth, up from the previous projection of 11.25B.

- Revised the full-year AI-driven revenue milestone upward to 3.5B.

- Maintained full-year Non-GAAP gross margin expectations at 62% to 64%, with operating margins expected around 46%.

Market Reaction & Potential Risks

Despite beating quarterly projections and raising full-year targets, Arista’s stock experienced a sharp drop of roughly 14% in after-hours trading. Investors reacted to the full-year revenue growth outlook of 27.7%, which fell short of more aggressive whisper numbers looking for 28% to 30%. Additionally, the anticipated sequential compression in Non-GAAP operating margin for the second quarter (46%-47% vs. 47.8% in Q1) weighed on sentiment. Management also cited persistent upstream supply chain bottlenecks in wafers and chip components, which continue to challenge lead times and margins.

Key Structural Shifts and Strategic Changes This Quarter

Arista Networks disclosed several pivotal strategic shifts and business transformations during this quarter’s (Q1 2026) earnings call, primarily focusing on the expansion of AI network architecture, deferred revenue product cycles, and enterprise market integrations:

1. Entering the “Scale-up” Network Arena

Historically, Arista’s core strength has resided in “Scale-out” networking (the backend fabrics interconnecting multiple AI clusters and switches).

During this earnings call, management explicitly declared their intention to venture into the “Scale-up” networking domain (the ultra-high-speed interconnects within individual GPU servers or single racks) by 2027 and beyond. Leveraging upcoming Ultra Ethernet Consortium (UEC) standards, Arista plans to compete directly with incumbent architectures like proprietary NVLink or PCIe, opening a massive new addressable market.

2. Surge in Deferred Revenue Reflecting Extended Testing Phases

Deferred revenue escalated sharply to 6.2B this quarter, up from 5.37B in the consecutive prior quarter.

This pronounced change is primarily driven by extended testing, acceptance, and validation cycles for next-generation AI pipelines (particularly new 800G product portfolios and updated silicon architectures) deployed at major Hyperscaler accounts. While customer demand remains intact and committed, revenue recognition is pushed out over a longer runway.

3. VeloCloud Integration and Enterprise Go-To-Market Shifts

Within the enterprise and campus/branch networking segments, Arista is accelerating the integration of its recently acquired VeloCloud SD-WAN technology.

This move introduces a new “channel motion” to Arista’s historical sales playbooks, allowing the company to penetrate Managed Service Provider (MSP) networks and diversify its revenue stream away from pure data center environments toward distributed enterprise architectures.

4. Upward Revisions for Full-Year Financial and AI Targets

On the back of robust AI infrastructure momentum, management enacted significant positive revisions to their full-year outlook:

- Lifted full-year 2026 top-line revenue guidance from the previously issued 11.25B to 11.5B.

- Upgraded the full-year “AI Fabric” pure-play revenue target to 3.5B, up from the prior forecast of 3.25B. This updated milestone represents more than a 100% year-over-year increase compared to 2025 AI revenue, cementing AI as the primary engine for the company’s growth.

Growth Drivers for the Upcoming Quarter

During the Q1 2026 earnings conference call, management outlined the core catalysts driving sequential growth for the upcoming second quarter and the back half of fiscal year 2026:

1. Accelerated Volume Shipments and Revenue Recognition of 800G Switches

The substantial increase in deferred revenue to 6.2B in Q1 was primarily due to extended customer validation timelines for next-generation 800G Ethernet platforms. As these deployments clear customer acceptance milestones throughout Q2, this backlogged pipeline will officially convert into recognized revenue, serving as the most immediate top-line catalyst. The cumulative customer base deploying 800G solutions has now surpassed 100 accounts.

2. Hyperscaler Expansion of “AI Spine” Infrastructure

Microsoft and Meta continue to anchor the business as key 10% plus revenue contributors. Management indicated that as shipment volumes scale in Q2, an additional 1 to 2 customers—potentially Tier-2 hyperscalers or specialized GPU cloud providers—could cross the 10% revenue contribution threshold. Hardware upgrades centered on backend “AI Spine” fabrics by these massive scale players will directly fuel Q2 momentum.

3. Increasing Contribution from “Scale Across” Architectural Frameworks

While traditional “Scale-out” horizontal clustering remains the foundation, management noted that “Scale Across” network deployments (engineered to interconnect multiple disparate AI clusters) are projected to account for at least one-third of total AI networking revenue this year. The adoption curve for this architecture is expected to steepen significantly in Q2, serving as a primary lever behind the upward revision of the annual AI Fabric revenue milestone to 3.5B.

4. Initial Commercial Pull for XPO Liquid-Cooled Optics

The newly introduced XPO (64-channel, 12.8Tbps capacity) high-density, liquid-cooled pluggable optical module targets power and space constraints in next-generation high-density AI layouts. As clusters featuring latest-generation, high-thermal-design-power GPU servers expand deployment in Q2 and Q3, commercial demand for these space-saving optical components will begin to materialize.

5. Dual-Track Progress via VeloCloud and Enterprise Campus Networks

Outside of the core AI data center market, Arista’s full-year revenue target for the Enterprise Campus segment remains on track at 1.25B. Second-quarter initiatives will focus on deepening channel partnerships with Managed Service Providers (MSPs), utilizing the recently integrated VeloCloud SD-WAN capabilities to secure a steady secondary growth curve distinct from cloud spending cycles.

Forward EPS Trajectory Over the Next 12 Months

Based on the newly released Q1 earnings results, official management guidance, and updated Wall Street consensus, Arista Networks’ Earnings Per Share (EPS) over the next 12 months is projected to follow a trajectory characterized by “near-term sequential margin compression, robust full-year growth, and an accelerated breakout heading into 2027.”

Here is a detailed breakdown of the key factors shaping the EPS outlook:

1. Near-Term Trajectory: Q2 Sequential Headwinds

While Q1 2026 Non-GAAP EPS delivered a strong beat at 0.87 dollars, expansion in the consecutive quarter (Q2 2026) faces near-term operating constraints:

- Official Q2 EPS Guidance: Projected at approximately 0.88 dollars, representing a modest sequential increase of just 0.01 dollars over Q1.

- Primary Catalysts: Q1 Non-GAAP operating margin surged to a high of 47.8%, but management’s Q2 guidance targets a lower band of 46% to 47%. This quarter-over-quarter compression stems from a shifting customer mix (higher concentration of heavy hyperscaler deployments) alongside upstream supply chain constraints in wafers, memory, and specialized chip components. These factors elevate near-term cost profiles, flattening the immediate EPS growth slope.

2. Full-Year 2026 Outlook: Resilient Double-Digit Expansion

Looking at the broader fiscal year 2026 runway, the underlying earnings foundation remains highly robust, fortified by the upward revision of full-year revenue guidance to 11.5B:

- Full-Year 2026 EPS Consensus: Wall Street consensus estimates for full-year 2026 Non-GAAP EPS currently sit around 3.63 dollars.

- Stable Margin Baselines: Despite lingering supply chain challenges, management reiterated full-year expectations, holding Non-GAAP gross margins at 62% to 64% and operating margins at approximately 46%. With these core profitability baselines intact, the projected 27.7% top-line revenue growth will flow directly into double-digit EPS expansion for the year.

3. Heading into 2027: Deferred Revenue Conversion as an Earnings Catalyst

The potential for an EPS breakout over the outer 12-month boundary is anchored by two major latent catalysts moving into early 2027:

- Unlocking 6.2B in Deferred Revenue: The massive expansion in deferred revenue to 6.2B (up nearly 100% year-over-year) is a function of extended validation cycles for new 800G platforms among hyperscalers. As these architectural footprints clear customer acceptance phases over the coming quarters, these high-margin product layers will generate an accelerated tailwind for EPS late this year and into early 2027.

- Preliminary 2027 EPS Outlook: Early market models project that as 800G shipments reach full run-rate scale and 1.6T production begins initial rollouts, fiscal year 2027 EPS could climb from the 2026 baseline range toward 3.95 dollars or higher, pulling year-over-year EPS growth back into a high-velocity 20%+ trajectory.

Strategic Summary

The 12-month EPS outlook reflects a “steady consolidation before an upward breakout.” Through Q2 and into early Q3, the market will absorb localized margin variations tied to component procurement costs, resulting in relatively flat sequential EPS steps. However, as 8.9B in long-term purchase commitments (securing foundry capacity at partners like TSMC) steadily converts into physical hardware deliveries, the overarching EPS path will trend upward, powered by the dual-engine expansion of the AI Fabric (3.5B annual target) and Enterprise Campus (1.25B annual target) segments.

Following the release of the Q1 2026 earnings report and the subsequent ~14% post-market price correction, several major institutional desks, including Truist Securities and Raymond James, have classified this pullback as an attractive buying opportunity rather than a fundamental breakdown.

Core Investment Thesis

- Supply-Gated Demand Safeguard: The primary headwind cited by management is upstream supply chain capacity—specifically wafer and chip allocation—rather than a cooling demand environment. Raising the full-year AI Fabric revenue milestone to 3.5B (more than 100% YoY growth) proves Arista’s indispensable market share within hyperscaler topologies like Microsoft and Meta.

- The 6.2B Invisible Shield: The surge in deferred revenue to 6.2B is fundamentally positive. It represents committed orders for next-generation 800G platforms undergoing extended verification. This creates a highly visible, robust revenue runway set to recognize over the coming quarters.

- Expansion into a New Total Addressable Market (TAM): Entering the GPU server-internal “Scale-up” networking market by 2027 using Ultra Ethernet Consortium (UEC) standards positions Arista to directly contest proprietary architectures like NVIDIA’s NVLink, opening a massive new growth vector.

Near-Term Risk Factors

- Sequential Margin Compression: The projected decline in Q2 operating margin guidance (46%-47% vs. 47.8% in Q1) due to escalating component procurement costs limits near-term EPS expansion.

- Elevated Valuation Multiples: Trading at an elevated trailing P/E relative to historical averages leaves a low margin for error. Consequently, whenever full-year guidance (27.7% growth) misses the most aggressive whisper numbers (28%-30%), the stock experiences heightened price volatility.

Potential Upside Analysis

Based on the latest models from analysts covering ANET, the 12-month target price projections and calculated returns are structured as follows:

12-Month Price Targets

- Consensus Mean Target: ~188.19 dollars

- Bull Case (High Estimate): 210.00 to 220.00 dollars

- Bear Case (Low Estimate): 164.00 dollars

Projected Return Metrics

- Base Case (Reaching Consensus Mean): Implies an upside potential of approximately +32.5%.

- Bull Case (Reaching High Institutional Target): Implies an upside potential of +48% to +55%.

- Margin of Safety (Reaching Low Target): Still yields an upside of +15.5%, indicating strong downside protection at current adjusted valuation levels.

Tactical Asset Allocation Guidance

For Mid-to-Long-Term Growth Investors

The post-earnings sell-off has effectively flushed out speculative short-term positioning, resetting valuation multiples to a more attractive entry point. A dollar-cost averaging strategy is recommended here to capture the multi-quarter EPS tailwinds generated by the 800G volume ramp-up and the subsequent 1.6T product cycle heading into 2027.

For Short-Term Momentum Traders

Caution is advised. Because Q2 profitability metrics are constrained by near-term supply chain premium costs, sequential EPS progression will stay flat before accelerating later in the year. The stock may consolidate technically between key moving averages over the near term, demanding a higher risk tolerance for sideways price action.

Source:

- https://www.arista.com/en/company/news/press-release/24017-pr-20260505

- https://www.sec.gov/Archives/edgar/data/1596532/000159653226000074/ex991q126-earningsrelease.htm

- https://www.investing.com/news/transcripts/earnings-call-transcript-arista-networks-q1-2026-earnings-exceed-forecasts-stock-rises-93CH-4661324

Back to Arista page