Foundational Era & Establishment (1837–1910s)

In 1837, blacksmith John Deere invented the self-scouring steel plow in Illinois, solving the problem of sticky prairie soil and launching the company. The business expanded its agricultural implement production and officially incorporated as Deere & Company in 1868. Beginning in 1911, the company executed a series of acquisitions to expand its portfolio from basic implements into multi-functional farm machinery.

The Tractor Age & Diversification (1918–1950s)

The company officially entered the tractor market in 1918 through the acquisition of the Waterloo Boy tractor manufacturer. During the Great Depression, the company supported struggling farmers by extending financing, which forged deep and lasting brand loyalty. Following World War II, the company secured its leadership in agricultural machinery while successfully diversifying into construction, forestry, and industrial equipment.

Global Expansion & Technological Innovation (1950–1990s)

Deere & Company accelerated its international footprint in 1956 by establishing its first overseas factory in Germany. In the 1960s, the launch of the “New Generation of Power” tractor lineup introduced unprecedented horsepower and safety features, cementing its position as the market leader. During this period, the company sustained its agricultural dominance while expanding the technical capabilities of its construction and forestry divisions.

Precision Agriculture & Digital Transformation (2000s–Present)

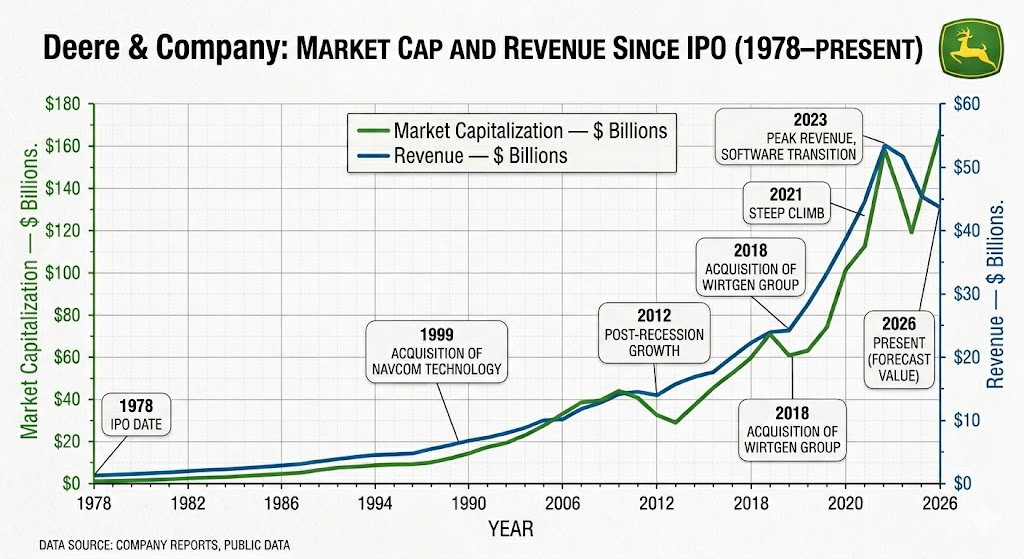

Entering the 21st century, Deere & Company transformed into a technology-driven industrial enterprise. Following the 1999 acquisition of NavCom Technology, the company integrated GPS-guided precision agriculture into its machinery. Today, the corporation actively fuses artificial intelligence, computer vision, and autonomous driving to deploy fully autonomous tractors and targeted spraying systems, utilizing data analytics to advance smart and sustainable global farming.

Deere & Company holds a leading position in the global heavy machinery market. Its competitive landscape is primarily divided into two main battlegrounds: Agricultural Machinery and Construction & Forestry Machinery. The core competitive analysis is detailed below:

1. Agricultural Machinery: The Big Three and Regional Pioneers

In the agricultural equipment market, Deere’s primary rivals are CNH Industrial and AGCO. Together, they form the global Big Three, with each company heavily focusing on the software and hardware integration of precision agriculture in recent years.

- CNH Industrial (Italy/United States)

- Core Brands: Case IH, New Holland.

- Competitive Position: Holding a global market share of around 15%, CNH is Deere’s most direct rival. It possesses immense strength in high-horsepower tractors and combine harvesters. Through its acquisition of Raven Industries, CNH has aggressively accelerated its deployment of autonomous driving and precision ag-tech.

- AGCO Corporation (United States)

- Core Brands: Fendt (premium positioning), Massey Ferguson, Valtra.

- Competitive Position: Holding a global market share of around 10%. Its tech-focused brand PTx (a joint venture with Trimble) is developing rapidly in smart farming, precision seeding, and targeted spraying technologies, posing a direct threat to Deere’s software ecosystem.

- Kubota (Japan)

- Competitive Position: Kubota dominates the global market for small-to-mid-sized tractors and rice cultivation machinery, holding an exceptionally high market share in Asia. Although it overlaps less with Deere in the North American large-scale machinery market, it remains a fierce competitor in the compact tractor segment and turf care equipment.

- Mahindra & Mahindra (India)

- Competitive Position: By volume, Mahindra is the world’s largest tractor manufacturer, focusing heavily on cost-performance value. Its light and utility tractors have achieved cumulative sales exceeding 300,000 units in North America, gradually capturing the entry-level value market.

2. Construction & Forestry Machinery: Challenging the Industrial Giants

While Deere’s Construction & Forestry division generates impressive revenue, it faces well-entrenched global giants with absolute dominance in this sector.

- Caterpillar (United States)

- Competitive Position: The world’s largest manufacturer of construction and mining equipment. Caterpillar commands an unshakeable market share in heavy earthmoving equipment like large excavators and bulldozers, presenting the toughest competition for Deere in the construction sector.

- Komatsu (Japan)

- Competitive Position: The world’s second-largest construction machinery manufacturer. Known for its industry-leading Smart Construction initiatives and remote autonomous mining systems, Komatsu competes fiercely with Deere across the Asia-Pacific and global markets.

3. Core Competitive Advantages of Deere & Company (Moat)

- Precision Agriculture Technology Moat: Deere holds more than 18,000 smart agriculture patents. Its core platform, the John Deere Operations Center, has accumulated hundreds of millions of acres of connected farmland. By deploying technologies like See & Spray intelligent spraying and Level 4 fully autonomous tractors, Deere has successfully transitioned part of its hardware sales into high-margin SaaS subscription revenue, which has already surpassed 1.8B.

- Unrivaled Dealer Network: Deere commands the densest exclusive dealership and aftermarket service network in North America and across key global regions. Heavy machinery relies heavily on immediate maintenance and parts supply, as delays during planting or harvest seasons are incredibly costly. This 24/7 lifecycle support creates massive switching costs for customers.

- Robust Captive Financial Services: John Deere Financial manages over 60B in assets. It provides counter-cyclical, flexible financing and leasing solutions to farmers and construction contractors globally, effectively locking in customer loyalty.

Summary

The strategic core of Deere & Company has successfully shifted from a traditional steel manufacturer to a big data and automation software company. Even as it faces the sheer scale of Caterpillar and the technological pursuit of CNH Industrial, Deere sustains robust pricing power and market leadership in the high-end, intelligent modern agriculture sector through its well-developed ecosystem moat.

Source

- https://www.deere.com

- https://www.cnhindustrial.com

- https://www.agcocorp.com

- https://www.kubota.com

- https://www.mahindratractor.com

- https://www.caterpillar.com

- https://www.komatsu.jp

Back to Deere page