Foundation and Chemical Era (1849-1940s)

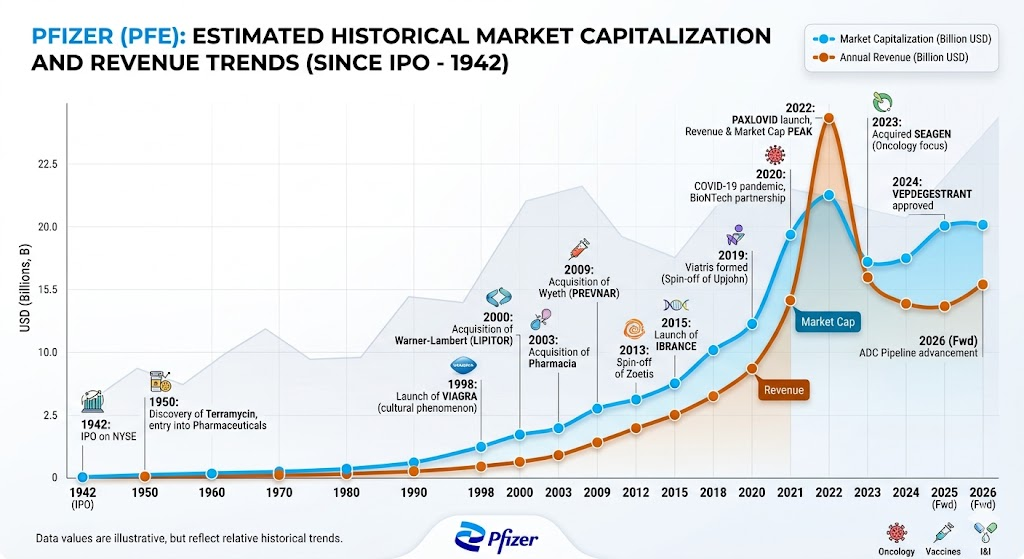

In 1849, German immigrants Charles Pfizer and Charles Erhart founded Pfizer in New York as a fine chemicals business. Their first major success came in 1849 with santonin, an effective antiparasitic medication. During World War I, Pfizer pioneered the mass production of citric acid via fermentation technology. This deep expertise in industrial fermentation proved critical during World War II, enabling Pfizer to successfully mass-produce penicillin and become a primary supplier of the lifesaving antibiotic to Allied forces.

Transition to Pharmaceuticals and Global Expansion (1950s-1980s)

In 1950, Pfizer discovered Terramycin (oxytetracycline), a broad-spectrum antibiotic. This was the first pharmaceutical developed and sold under the Pfizer label, marking the company’s transformation into a research-driven pharmaceutical enterprise. Pfizer rapidly expanded its international presence and built a formidable sales force. By the 1980s, the company launched blockbuster treatments like the anti-inflammatory Feldene and the cardiovascular medication Norvasc, driving annual revenues past 1B for the first time.

Mega-Mergers and the Blockbuster Era (1990s-2010s)

In 1998, Pfizer launched Viagra, a revolutionary treatment for erectile dysfunction that became an instant global cultural and commercial phenomenon. To sustain growth, Pfizer executed a series of massive acquisitions over the next decade. The company acquired Warner-Lambert in 2000 (gaining Lipitor, which became the best-selling drug in pharmaceutical history), Pharmacia in 2003, and Wyeth in 2009 (gaining the Prevnar pneumococcal vaccine). These historic mergers cemented Pfizer as the world’s largest pharmaceutical company.

Biopharma Refocus and the Pandemic Response (2019-Present)

Following the appointment of Albert Bourla as CEO in 2019, Pfizer initiated a strategic spin-off of its off-patent established medicines division (merging it with Mylan to form Viatris) to transform into a streamlined, high-growth biopharmaceutical innovator. When the COVID-19 pandemic emerged, Pfizer partnered with Germany’s BioNTech to develop Comirnaty, the world’s first authorized mRNA vaccine, followed by the oral antiviral Paxlovid. These two products generated unprecedented financial results, pushing Pfizer’s total revenue to a historic peak of over 100B in 2022. Post-pandemic, Pfizer has pivoted its massive capital reserves toward oncology, finalizing its acquisition of cancer specialist Seagen in 2023 to lead the next generation of targeted cancer therapies.

The following is a global competitive analysis of Pfizer, focusing on its four core therapeutic pillars, key rivals, and strategic positioning:

Core Therapeutic Pillars and Competitive Landscape

1. Oncology

- Current Position: This is currently Pfizer’s primary growth engine. The 43B acquisition of Seagen established Pfizer as a global leader in Antibody-Drug Conjugates (ADCs), adding blockbuster assets like Padcev and Adcetris to its portfolio. Additionally, newly approved treatments in early 2026, such as the oral PROTAC Vepdegestrant, have strengthened Pfizer’s leadership in targeted breast cancer therapies.

- Key Rivals: Merck (dominating the field with its anti-PD-1 blockbuster Keytruda), AstraZeneca, Roche, and Daiichi Sankyo (a formidable competitor in ADC technology).

- Strategic Focus: Securing market share through next-generation ADC technology and accelerating clinical pipelines for novel immuno-oncology targets.

2. Vaccines

- Current Position: As COVID-19 vaccine (Comirnaty) revenues stabilized post-pandemic, Pfizer pivoted its focus toward routine infectious diseases. Its pneumococcal conjugate vaccine, Prevnar 20, maintains a market share of over 70% in the US adult segment. In the RSV (Respiratory Syncytial Virus) market, Abrysvo is experiencing steady growth.

- Key Rivals: GSK (whose RSV vaccine, Arexvy, applies intense competitive pressure in retail channels), Sanofi, and Moderna.

- Strategic Focus: Advancing the development of combination mRNA vaccines (such as flu/COVID-19 combos) and capturing market share in the maternal and older adult RSV segments.

3. Inflammation & Immunology (I&I)

- Current Position: Pfizer features a strong oral JAK inhibitor portfolio (including Xeljanz, Litfulo, and Velsipity) targeting rheumatoid arthritis, ulcerative colitis, and alopecia areata.

- Key Rivals: AbbVie (maintaining strong dominance with Skyrizi and Rinvoq as successors to Humira), Johnson & Johnson, and Bristol Myers Squibb (BMS).

- Strategic Focus: Navigating stringent regulatory safety warnings on JAK inhibitors while mitigating margin erosion caused by small-molecule generics impacting legacy assets.

4. Internal Medicine and Metabolic Diseases

- Current Position: The blockbuster anticoagulant Eliquis (co-marketed with BMS) remains a major revenue contributor but is gradually approaching its patent cliff. In the highly lucrative obesity and diabetes (GLP-1) market, Pfizer faced early internal R&D setbacks but is accelerating its timeline through restructuring and external collaborations.

- Key Rivals: Eli Lilly (Mounjaro/Zepbound) and Novo Nordisk (Wegovy/Ozempic).

- Strategic Focus: Securing a foothold in oral GLP-1s and next-generation metabolic candidates to break the current duopoly held by Eli Lilly and Novo Nordisk.

SWOT Matrix Analysis

Strengths

- Unparalleled Capital Reserves: The significant cash reserves generated during the pandemic peak grant Pfizer exceptional “buy-and-scale” M&A capabilities and commercial integration power.

- Global Commercial Infrastructure: Possesses a deeply entrenched, highly efficient supply chain and marketing network spanning nearly 200 countries.

Weaknesses

- Impending Patent Cliffs (LOE):Between 2025 and 2030, several of Pfizer’s core legacy blockbusters, including Eliquis and Ibrance, face patent expirations and subsequent generic erosion.

- Heavy Reliance on Inorganic Growth: Compared to peers like Vertex or Eli Lilly, which boast highly successful internal discovery platforms, Pfizer relies more heavily on expensive acquisitions (e.g., Seagen) to replenish its pipeline.

Opportunities

- AI-Driven R&D Efficiency: Pfizer is deploying enterprise-wide AI and digital clinical trial designs, aiming to reduce clinical trial cycle times by up to 20%.

- Oncology Pipeline Monetization: Continued indication expansions for Seagen’s ADC platform in Phase 3 trials (e.g., bladder and lung cancers) present significant revenue expansion potential.

Threats

- Global Drug Pricing Policies: Legislative actions like the US Inflation Reduction Act (IRA) Medicare price negotiations, European HTA reforms, and volume-based procurement (VBP) programs in Asian markets continue to squeeze profit margins for innovative therapies.

- Biosimilar Competition: Emerging biologics and novel immunotherapies face an increasingly aggressive wave of lower-cost biosimilar competition worldwide.

Source:

- https://www.pfizer.com/news/press-release/press-release-detail/pfizer-invests-43-billion-battle-cancer

- https://www.pfizer.com/news/press-release/press-release-detail/pfizer-completes-acquisition-seagen

- https://www.fda.gov/drugs/resources-information-approved-drugs/fda-approves-vepdegestrant-er-positive-her2-negative-esr1-mutated-advanced-or-metastatic-breast

- https://ir.arvinas.com/news-releases/news-release-details/arvinas-announces-fda-approval-veppanu-vepdegestrant-treatment

Back to Pfizer page