Based on the first quarter 2026 financial and operational results released by China Mobile (0941.hk), here is the summary:

1. 2026 Q1 Financial Performance Summary

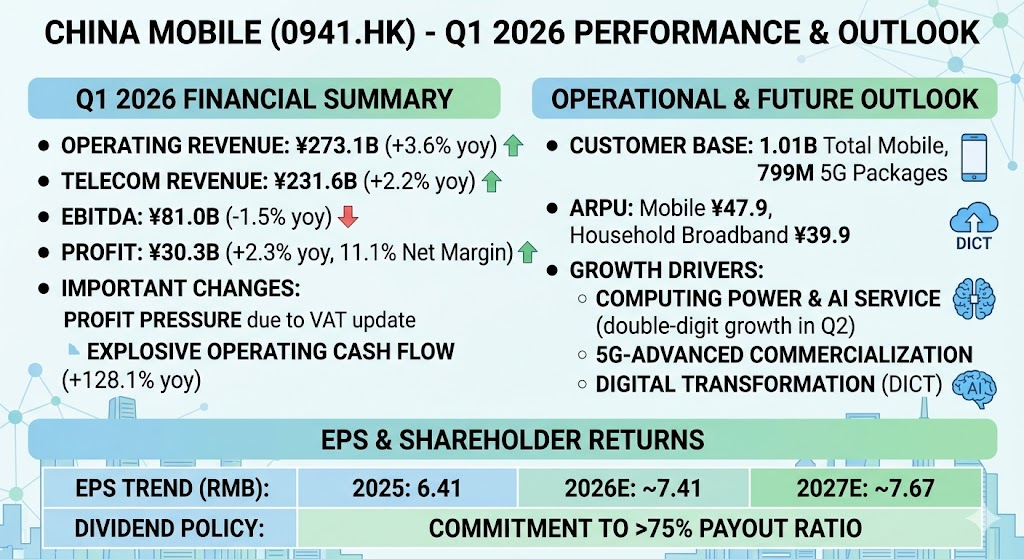

- Operating Revenue: 273.1B RMB, up 3.6% yoy.

- Revenue from Telecommunications Services: 231.6B RMB, up 2.2% yoy.

- Revenue from Sales of Products and Others: 41.5B RMB, up 12.4% yoy.

- EBITDA: 81.0B RMB, down 1.5% yoy.

- Profit Attributable to Equity Holders: 30.3B RMB, up 2.3% yoy, with a net profit margin of 11.1%.

2. Customer Base and Market Performance

- Mobile Customers: Total reached 1.01B, with a net increase of 5.12M in this quarter.

- 5G Package Customers: 799M.

- 5G Network Customers: 503M.

- Mobile ARPU (Average Revenue Per User): 47.9 RMB.

- Wireline Broadband Customers: Total reached 305M, with a net increase of 6.83M in this quarter.

- Household Broadband Customers: 269M, a net increase of 5.28M.

- Household Broadband Blended ARPU: 39.9 RMB.

3. Growth Drivers and Strategy

- Digital Transformation Revenue: Continues to be the primary growth engine, with computing power services maintaining strong momentum.

- Capital Expenditure Trends: As the peak of 5G investment has passed, the company is shifting its investment focus toward computing networks and AI infrastructure.

- Dividend Policy: Maintaining the previous commitment to gradually increase the dividend payout ratio to over 75%.

Based on the first quarter 2026 financial report and market analysis, China Mobile has demonstrated a significant strategic transformation and shifts in its financial structure. The key highlights are as follows:

1. Profit Pressure Due to VAT Adjustments

Profit attributable to equity holders for this quarter was 29.3B RMB, a year-on-year decrease of 4.2%. This was primarily affected by the policy update regarding the increase in Value-Added Tax (VAT) rates for telecommunications services effective from 2026. Excluding this policy factor, the company’s operational profitability remained relatively stable.

2. Qualitative Change in Revenue Structure

- Traditional Business Reaching Peak: Revenue from telecommunications services was 219.9B RMB, down 1.1% yoy. This reflects the saturation of the traditional mobile communications market.

- Strengthening Emerging Drivers: Other business revenue (including cloud computing, computing power leasing, and AI services) reached 46.6B RMB, a significant increase of 12.7%. This segment now accounts for approximately 17.5% of total revenue. The company is transitioning from a “telecom service provider” to an “AI and computing power service provider.”

3. Explosive Growth in Operating Cash Flow

Net cash flow from operating activities for this quarter reached 71.447B RMB, an impressive year-on-year increase of 128.1%. This was mainly driven by optimized supply chain capital management and the results of entering a downward cycle for capital expenditure (CAPEX).

4. Optimization of Capital Expenditure Structure

The CAPEX budget for the full year of 2026 has been adjusted to 136.6B RMB, a 9.5% decrease compared to last year. However, the focus of investment has shifted dramatically:

- Traditional Network Investment: Expected to decrease by 20.3%.

- Computing Network Investment: Expected to increase significantly by 62.4%.

- Artificial Intelligence (AI) Investment: Expected to grow by 19.8%.

5. Sustained Increase in R&D Investment

Research and development expenses grew by 22.3% yoy, reaching 3.904B RMB. This indicates that the company is accelerating its deployment of the “Jiutian” large model and 5G-Advanced technologies. While this puts short-term pressure on profits, it is considered core to long-term competitiveness.

Summary

This quarter can be viewed as a critical turning point for China Mobile, marking the transition into a “post-peak investment harvest period” and a “pivot toward computing services.” Despite short-term profits being hampered by tax policies, the strong cash flow and growth in new business provide a solid foundation for maintaining a high dividend payout ratio of over 75%.

Based on China Mobile’s (0941.hk) latest strategic layout and Q1 2026 performance guidance, the growth momentum for the next quarter (Q2 2026) will focus on these three core areas:

1. Computing Power and AI Services: Transitioning from Infrastructure to Revenue Harvest

- AIDC and Intelligent Computing Center Commissioning: The company plans to accelerate the deployment of AI Data Centers (AIDC) in 2026, particularly the 100MW-level Global Intelligent Computing Center (GIC) recently opened in Hong Kong. This will drive continued double-digit growth in computing power service revenue in Q2.

- Commercialization of “Jiutian” Large Model: As the “AI+” action plan penetrates sectors like the Industrial Internet, government services, and Cloud PCs, more B2B AI application cases are expected to convert into substantial revenue during the second quarter.

2. Deepening 5G-Advanced (5G-A) Business Models

- Scale Commercialization of 5G-A: 2026 is a critical year for China Mobile to strive for full-scale commercialization of 5G-A. Q2 is expected to see the launch of more applications combining Integrated Sensing and Communication (ISAC) and passive IoT, targeting new customers in emerging industries like logistics and the low-altitude economy.

- Structural Optimization of ARPU: Although the traditional communication market is saturated, the company is attempting to maintain or even slightly increase Mobile ARPU (Average Revenue Per User) through high-value-added services brought by 5G-A, such as New Calling and naked-eye 3D.

3. “Mobile Cloud” and Digital Transformation (DICT)

- Accelerated Digital Transformation: The DICT business (Cloud, Big Data, IoT) has already shown strong momentum this quarter, with its revenue share continuing to expand. Q2 will benefit from enterprise demand for cloud migration driven by “Digital China” policies. The growth rate of this segment is expected to far outpace traditional telecommunication services.

- Protection of Shareholder Returns: Strong operating cash flow (up 128.1% yoy in Q1) will continue to play a role in Q2. Since the peak of 5G CAPEX investment has passed, the company has more flexibility to invest in R&D for new technologies while supporting its commitment to increase the dividend payout ratio to over 75%, maintaining its attractiveness as a high-yield stock.

Key Data Points to Watch in the Coming Quarter

| Observation Metric | Expected Trend | Core Significance |

| Digital Transformation Revenue % | Steady Increase | Validates the successful transition into a technology service enterprise |

| Computing Service Growth Rate | Maintain >10% yoy | A tangible profitability indicator for AI and computing networks |

| CAPEX Control | Continued Decline/Optimization | Impacts Free Cash Flow (FCF) and dividend capacity |

Based on market consensus forecasts and the actual performance in the first quarter of 2026, the EPS (Earnings Per Share) trend for China Mobile (0941.hk) over the coming year is expected to maintain steady growth. The key projections and trends are as follows:

1. EPS Forecast Data

The consensus analyst forecast for the full year of 2026 is approximately 7.41 RMB, representing an expected annual increase of about 12.4% compared to 6.41 RMB in 2025.

- 2026 Q2 Forecast: The market expects a single-quarter EPS of approximately 2.36 RMB.

- Long-term Trend (2027): EPS is projected to further increase to around 7.67 RMB, maintaining a moderate growth rate of approximately 3.5%.

2. Positive Factors Supporting EPS Growth

- Reduced Depreciation Pressure: With the peak of 5G investment concluded, the growth of depreciation and amortization expenses is slowing down starting in 2026, directly contributing to the release of profit margins.

- Rising Share of High-Margin New Business: Profit margins for emerging sectors such as cloud computing and AI computing power leasing are gradually optimizing, becoming a new engine for overall EPS growth.

- Operational Efficiency Optimization: The company continues to implement cost-reduction and efficiency-enhancement measures. The strong cash flow performance in 2026 Q1 provides a solid foundation for future profitability.

3. Potential Downside Risks and Disruptions

- Tax Policy Impact: The adjustment of VAT rates for telecommunications services that took effect in 2026 already caused a negative impact of approximately 4% on net profit in the first quarter. This may cause the actual full-year EPS to land at the lower end of analyst projections.

- Increased R&D Spending: The company’s R&D investment in AI large models (such as the Jiutian model) and 5G-A technology continues to maintain double-digit growth, which may offset some operating profits in the short term.

4. Correlation Between Dividends and Value

As EPS is expected to show double-digit or high single-digit growth, coupled with the company’s commitment to increase the payout ratio to over 75%:

- Dividend Increase: The growth in EPS will directly drive an increase in the absolute value of dividends for the 2026 fiscal year.

- Valuation Support: A stable EPS growth path provides reasonable defensive support for the current forward P/E ratio of approximately 10-11x.

Comprehensive Outlook Table

| Period | Estimated EPS (RMB) | Estimated Growth (YoY) |

| 2025 (Actual) | 6.41 | -0.9% |

| 2026 (Forecast) | 7.41 | ~12.4% |

| 2027 (Forecast) | 7.67 | ~3.5% |

Source:

- https://www1.hkexnews.hk/listedco/listconews/sehk/2026/0326/2026032600469_c.pdf

- https://www1.hkexnews.hk/listedco/listconews/sehk/2026/0420/2026042000570_c.pdf

- https://techreviewafrica.com/news/5374/china-mobile-unveils-ai-driven-transformation-strategy-at-2026-mobile-cloud-conference

- https://simplywall.st/stocks/hk/telecom/hkg-941/china-mobile-shares/future

- https://ng.investing.com/pro/SEHK:941/earnings

- https://www.moomoo.com/stock/00941-HK/earnings

Back to China Mobile page