HDB (HDFC Bank Limited ADR) Q4 FY2026 Earnings Summary

According to the latest financial data for fiscal year 2026, HDFC Bank demonstrated steady performance with the following key financial metrics:

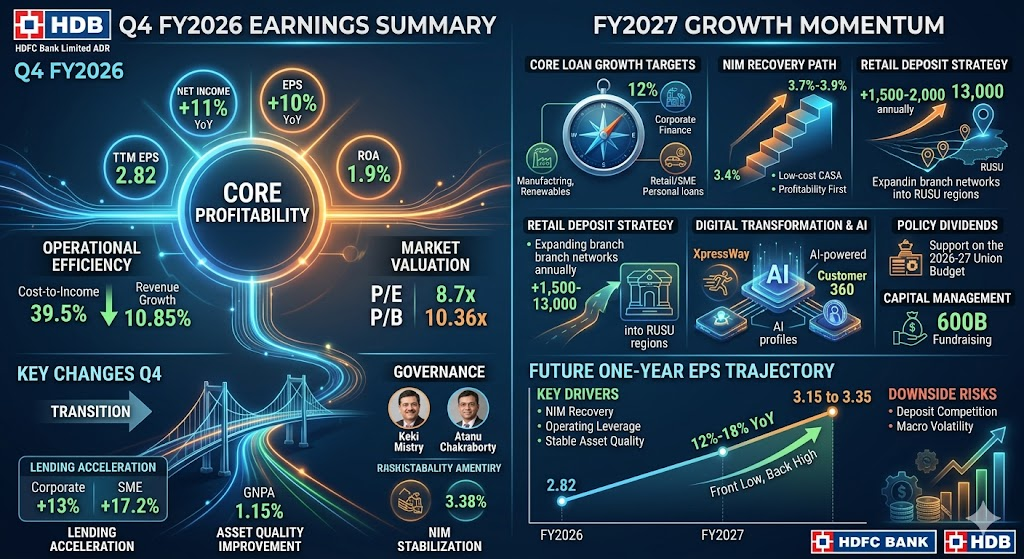

Core Profitability

- Net Income: Increased by 11% compared to the same period last year.

- Earnings Per Share (EPS): Grew by 10% year-on-year.

- Trailing Twelve Months (TTM) EPS: 2.82.

- Return on Assets (ROA): Maintained at a level of 1.9%.

Operational Efficiency and Costs

- Cost-to-Income Ratio: Decreased to 39.5%, indicating improved operational efficiency.

- Quarterly Revenue Growth (YoY): 10.85%.

Market Valuation Reference

- Price-to-Earnings (P/E) Ratio: Approximately 8.7x.

- Price-to-Book (P/B) Ratio: Approximately 10.36x.

- Market Commentary: Despite facing downward pressure on the stock price over the past six months, some analytical institutions (such as InvestingPro) assess the stock as currently being undervalued.

HDB (HDFC Bank) showcased a pivotal shift from the post-merger “transition phase” to a “growth phase” in Q4 FY2026 (ended March 31, 2026).

The following are the most significant operational shifts and financial adjustments this quarter:

1. Strategic Shift: From De-leveraging Back to Accelerating Lending

In previous quarters, the bank focused on reducing the Loan-to-Deposit Ratio (LDR). However, this quarter, management signaled that the LDR is no longer a constraint, and they intend to re-accelerate credit expansion, particularly in Corporate loans (up 13%) and SME loans (up 17.2%).

2. Granularization and Stability of Deposit Structure

- Deposit Growth Outpacing Lending: Deposits grew by 14.4% year-on-year, significantly higher than the 12% growth in loans, indicating ample liquidity.

- Increased Share of Small Deposits: Retail deposits under 30 million Rupees rose from 31% to 47% of the total, which helps lower funding costs and increases the stability of the deposit base.

3. Asset Quality Hits Multi-Year Lows

The performance of asset quality this quarter was exceptional, with Non-Performing Assets (NPA) declining:

- Gross NPA (GNPA): Dropped to 1.15%, the lowest level in the past seven quarters.

- Reduced Provisioning: Due to improved asset quality, provisioning expenses fell by 18.2% year-on-year, directly contributing to profit growth.

4. Signs of Recovery in Net Interest Margin (NIM)

While still below the pre-merger level of 4.1%, the NIM stabilized at 3.38% this quarter and has shown slight expansion for two consecutive quarters. This suggests that the negative impacts of the merger (high-cost borrowings and low-yield mortgages) are being mitigated as funding costs begin to decline.

5. Governance and Financing Plans

- Management Changes: Former Chairman Atanu Chakraborty resigned in mid-March 2026 and was succeeded by veteran banker Keki Mistry. Markets are closely watching for continued board stability.

- Large-Scale Fundraising: The Board approved raising up to 600 billion Rupees (approximately 7.2B) through bond issuances over the next 12 months to fund infrastructure projects and bolster capital.

6. Shareholder Returns

- Dividend Payout: The bank announced a final dividend of 13 Rupees per share. Including the interim dividend already paid, the total payout for the year is 15.5 Rupees, making it one of the higher dividend-yielding options among its peers.

Summary: This quarter’s results indicate that HDFC Bank has largely moved past the shadow of the 2023 mega-merger. With a stronger and cleaner balance sheet, the bank has laid the groundwork for renewed growth in FY2027.

Looking ahead to Fiscal Year 2027 (FY2027), HDFC Bank’s management has explicitly shifted its focus from the post-merger “integration phase” toward “responsible growth.” The anticipated growth momentum will stem from several key dimensions:

1. Core Loan Growth Targets

- Growth Guidance: The bank expects loan growth to remain around 12% in FY2027. While more cautious than previous expectations of “outpacing the system,” this strategy aims to navigate geopolitical uncertainties and ensure earnings quality.

- Key Sectors:

- Corporate Finance: Demand remains robust, driven by Indian government policy subsidies for electronics manufacturing, semiconductors (ISM 2.0 program), and renewable energy.

- Retail and SME: Vehicle loans, personal loans, and business banking have shown significant recovery over the past three quarters and are expected to be major growth engines in 2027.

2. Recovery of Net Interest Margin (NIM) and Profitability

- NIM Recovery Path: Management aims to gradually push the NIM from the current 3.4% level toward a range of 3.7% to 3.9%.

- Execution Strategy:

- Low-cost Funding Replacement: Continuously replacing high-cost bonds inherited during the initial merger phase with low-cost CASA (Current Account Savings Account) deposits.

- Profitability First: Management emphasized they will no longer chase a lower Loan-to-Deposit Ratio (LDR) for its own sake, but rather select lending opportunities based on profitability.

3. “Granularization” Strategy for Retail Deposits

- Network Expansion: Plans to add 1,500 to 2,000 new branches annually, with a goal to double the total branch count to 13,000 in the coming years.

- Deepening Presence in Rural and Semi-Urban (RUSU): Acquiring more stable and lower-cost retail deposits by expanding into these under-penetrated regions.

4. Digital Transformation and AI Applications

- XpressWay Platform: Utilizing fully digital onboarding and lending processes (such as OTP-less verification and instant loan approval) to enhance customer acquisition efficiency and reduce operating costs.

- AI Empowerment: Leveraging AI for precise “Customer 360” profiling to increase the conversion rate of cross-selling credit cards and insurance products to existing customers.

5. Policy Dividends: Union Budget 2026-27

- Infrastructure and Manufacturing: Strong support from the Indian government for manufacturing (such as the Biopharma SHAKTI initiative) in the 2026 budget will directly create business opportunities for HDFC Bank in infrastructure financing and supply chain finance.

6. Capital Management and Shareholder Returns

- Financing Reserves: The Board has approved a bond issuance plan of up to 600B (approximately 7.2B) over the next 12 months, ensuring sufficient fuel for the next round of expansion.

- Stable Returns: As profit growth accelerates, markets expect the bank to maintain a stable dividend policy and potentially offer incentives such as the Bonus Issue seen in FY2026.

Based on consensus from market analysts and brokerage research reports, the EPS for HDFC Bank (HDB) is expected to enter a phase of steady growth in the coming year (FY2027).

The following is a detailed analysis of the EPS trajectory:

1. EPS Growth Forecasts

- FY2027 Estimated EPS: Market analysts expect HDB’s earnings per share to land within the range of 3.15 to 3.35.

- Projected Growth Rate: Compared to 2.82 in FY2026, the year-on-year (YoY) growth rate is expected to be between 12% and 18%.

- Quarterly Momentum: Growth is expected to follow a “lower start, higher finish” pattern. As high-cost liabilities mature and are replaced by low-cost deposits, profit realization will become more pronounced in the second half of the year.

2. Key Drivers for EPS Growth

- Net Interest Margin (NIM) Recovery: Management aims to raise the NIM from 3.4% to above 3.7%. Given the bank’s massive scale, every 10 basis point (0.1%) improvement in NIM provides a significant marginal contribution to EPS.

- Operating Leverage: As the upfront costs of the aggressive branch expansion (1,500 to 2,000 branches per year) over the past two years are gradually amortized and new branches become profitable, the cost-to-income ratio is expected to continue declining, translating into higher net profit.

- Stable Asset Quality: GNPA currently remains at a historical low of 1.15%. Barring major macroeconomic shocks in FY2027, maintaining low credit costs will ensure that profits are not eroded by heavy provisioning.

3. Potential Downside Risks (Factors Pressuring EPS)

- Intense Deposit Competition: If the battle for deposits in the Indian banking sector persists, causing funding costs to fall slower than expected, profit margins will be squeezed.

- Macroeconomic Volatility: Geopolitical risks or a shift in the Reserve Bank of India’s (RBI) monetary policy could suppress loan demand if high interest rates are forced to stay for an extended period.

4. Impact of Equity Capital Changes

- Bonus Issue: There are market rumors that HDFC Bank may consider a bonus issue in FY2027 to reward shareholders. While this would increase the total share count and dilute “EPS per share,” it is generally viewed as a positive signal of management’s confidence in future earnings and helps improve market liquidity.

Summary

The EPS trajectory for HDB over the coming year shows high predictability and growth potential. After shedding the burdens of merger integration, EPS is set to return to a double-digit growth path, driven by the dual engines of margin expansion and improved operational efficiency.

Source:

- https://statementdog.com/analysis/HDB

- https://hk.investing.com/equities/hdfc-bank

- https://m.rediff.com/business/report/hdfc-bank-moderates-fy27-growth-outlook-targets-12-y-o-y/20260420.htm

- https://simplywall.st/community/narratives/in/banks/nse-hdfcbank/hdfc-bank-shares/dt5spadb-hdfc-bank-limited-navigating-the-hdfc-20-integration-era

Back to HDFC Bank page