ConocoPhillips (NYSE: COP) has released its latest financial results for the first quarter of 2026, delivering performance that surpassed market expectations. Below is a summary of the key financial and operational highlights for the quarter:

Core Financial Performance

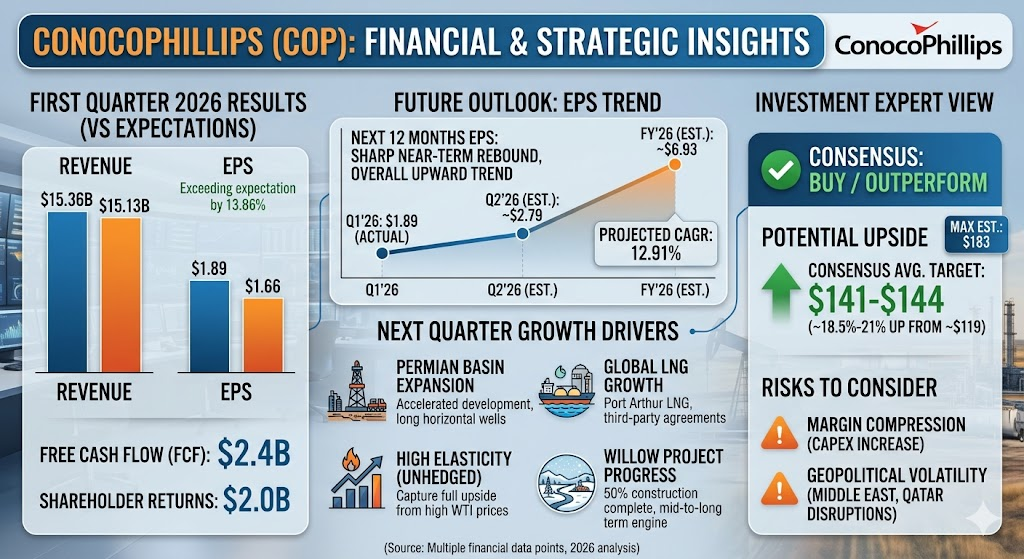

- Revenue: $15.36B, higher than the market expectation of $15.13B.

- Earnings Per Share (EPS): $1.89, beating the market consensus of $1.66 by 13.86%.

- Free Cash Flow (FCF): Generated $2.4B in free cash flow this quarter.

- Shareholder Returns: Returned a total of $2.0B to shareholders during the quarter.

Operations and Capital Expenditure

- Capital Expenditure (CapEx): CapEx for the quarter stood at $2.9B.

- Guidance Adjustment: Driven by increased activity in the Permian Basin, the company raised its full-year CapEx guidance to a range of $12.0B to $12.5B.

- Production Impact: Ongoing conflicts in the Middle East impacted certain production operations, particularly affecting activities in Qatar.

Market Reaction

Despite beating financial estimates, the stock experienced a pre-market decline of 4.45% following the announcement. This was primarily attributed to broader market concerns over geopolitical risks and potential cost pressures from the upward revision in capital expenditure guidance.

According to ConocoPhillips’ first-quarter 2026 earnings release and conference call, the most significant strategic and operational changes this quarter focused on several core areas:

1. Capital Expenditure Guidance Revision and Permian Basin Expansion

The company raised its full-year 2026 capital expenditure (CapEx) guidance to a range of $12.0B to $12.5B. The primary driver behind this adjustment is the decision to add a rig and a frac crew in the Permian Basin to accelerate development and production in the region.

2. Progress on the Marathon Oil Acquisition

A major corporate development this quarter involves the pending acquisition of Marathon Oil. Management stated they are actively complying with the Federal Trade Commission (FTC) regarding the second request review process and remain on track to close the transaction in the second half of 2026. The acquisition is expected to deliver significant synergies.

3. Geopolitical Fluctuations and Middle East Operations

Ongoing geopolitical conflicts and instability in the Middle East had a direct impact on the company’s operations this quarter. Specifically, activities in Qatar, including liquefied natural gas (LNG) related projects, experienced varying degrees of operational and supply chain disruptions.

4. Free Cash Flow Allocation Strategy

Despite strong operational performance, management emphasized that the company is prioritizing excess cash flow to support the aforementioned capital expenditure growth (such as the Permian expansion) rather than further expanding the scale of share repurchases at this time. This strategic shift reflects a near-term focus on capacity growth within core assets.

According to ConocoPhillips’ latest first-quarter 2026 earnings release and conference call, despite short-term challenges such as geopolitical volatility in the Middle East restricting capacity in Qatar, the company’s primary growth drivers and strategic initiatives for the upcoming quarter and the second half of 2026 focus on the following four key areas:

1. Accelerated Development in the Permian Basin

The Lower 48 region in the US achieved 4% year-over-year growth this quarter, with the core driver originating from the Permian Basin. The company announced in its first-quarter earnings report that it will add a drilling rig and a frac crew in the second half of the year to further improve operational efficiency and increase the proportion of long horizontal wells (3-mile plus laterals) drilled. This move will translate directly into more robust volume contributions in the coming quarters and set the operational baseline for 2027.

2. High Elasticity to Rising Oil Prices via Unhedged Assets

Management noted during the call that with Middle East conflicts causing potential capacity disruptions of approximately 10 million barrels per day globally, the physical crude market is expected to face substantial deficits between June and July, lifting the floor for West Texas Intermediate (WTI) prices. Because ConocoPhillips’ crude and liquefied natural gas (LNG) production remains largely unhedged, the company is positioned to fully capture the revenue and cash flow from operations (CFO) upside from higher oil prices in the upcoming quarter.

3. Global Liquefied Natural Gas (LNG) Expansion

Outside the US mainland, LNG projects represent a core growth pillar for the company’s next phase. In addition to signing a new third-party LNG tolling agreement with Equatorial Guinea to extend the life of existing assets, the Port Arthur LNG project in Texas is progressing smoothly, with first LNG production anticipated for next year.

4. Milestone Progress at the Willow Project in Alaska

Construction on the critical strategic development project, “Willow,” in Alaska has reached the 50% completion mark, with the company successfully finishing all planned winter scope. As this major development advances steadily, it will continue moving toward its initial production target over the coming quarters, serving as the company’s primary mid-to-long-term production growth engine.

According to ConocoPhillips’ first-quarter 2026 earnings conference call guidance and the subsequent revisions from Wall Street analysts, the outlook for the company’s earnings per share (EPS) over the next year indicates an optimistic trajectory characterized by a sharp near-term rebound and an overall upward trend for the full year.

Based on the latest market consensus estimates, the core drivers and specific trends for EPS over the next twelve months are outlined below:

1. Strong Rebound Expected in the Next Quarter (Q2 2026)

First-quarter EPS was temporarily weighed down by geopolitical issues restricting Qatari production and weak Permian gas prices, coming in at $1.89. However, as the physical crude market enters a supply deficit period between June and July, combined with Middle East geopolitical risk premiums lifting the floor for WTI prices, the market expects ConocoPhillips to benefit fully due to its unhedged production profile. Consequently, the consensus EPS estimate for the second quarter has been upwardly revised to approximately $2.79.

2. Upward Revision of Full-Year 2026 EPS Consensus

Following the first-quarter results, analysts have become generally more optimistic about the company’s full-year 2026 earnings potential. The Wall Street consensus for full-year 2026 EPS has been significantly adjusted from the previous estimate of around $6.12 to $6.93, primarily reflecting:

- Production volume gains resulting from the addition of an extra drilling rig and frac crew in the Permian Basin.

- Full-year revenue forecasts being raised from the initial $61.6B to $64.3B.

3. Mid-to-Long Term Growth Trajectory Over the Next Year (H2 2026 to H1 2027)

Looking out over the next twelve months, analysts project ConocoPhillips’ EPS compound annual growth rate to reach 12.91%, heavily tied to the execution of two major catalysts:

- The Marathon Oil Acquisition: Expected to close in the second half of 2026, management has committed that this transaction will unlock over $1.0B in annual operational and cost synergies before the end of 2026, which is expected to be substantially accretive to EPS over the coming year.

- Alaska’s Willow Project: With construction reaching 50% completion and advancing smoothly, this project remains a key reason why the market remains bullish on the company’s 2027 baseline production and earnings capacity.

Overall, while geopolitical volatility and higher capital expenditure guidance (raised to a range of $12.0B to $12.5B) created near-term cost pressures on the stock, improved development efficiencies at core assets and the profit margins anticipated from the pending acquisition are expected to drive EPS into an upward channel over the coming year.

Below is an in-depth investment assessment and analysis of the potential upside:

Core Rationale for the Recommendation (Investment Highlights)

- Perfect Elasticity to Rising Oil Prices: Global oil prices (WTI) remain high at over $100/barrel due to Middle East tensions and disruptions in the Strait of Hormuz. Because ConocoPhillips’ production profile is unhedged, its revenue and cash flow will capture the full benefit of this high oil price environment.

- Dual Engines: Permian Basin and Long-Term Projects: The company proactively added a rig and a frac crew to expand production following the first-quarter earnings, raising its full-year CapEx guidance. While this brings near-term cost pressures, it will translate directly into production baseline growth for the second half of the year and 2027. Additionally, the Willow project in Alaska is 50% complete, serving as a highly visible mid-to-long-term growth engine.

- Marathon Oil Acquisition Synergies: Expected to close in the second half of 2026, management anticipates unlocking over $1B in annual cost synergies before year-end, which will be directly accretive to EPS.

Potential Upside and Target Prices

As of mid-May 2026, COP is trading around $119.

Combining the latest post-earnings forecasts from major Wall Street investment banks (including Barclays, Wells Fargo, Morgan Stanley, etc.):

- Consensus Average Target Price: Approximately $141 to $144.

- Potential Upside: Represents a theoretical upside of roughly 18.5% to 21% from current price levels.

- Highest Institutional Estimate: Some institutions highly bullish on the oil market and the Willow project (such as Wells Fargo) have set target prices as high as $183.

Investment Risks to Consider

Despite the attractive upside, investors should monitor the following risks:

- Margin Compression from Increased CapEx: Raising the full-year CapEx guidance to a range of $12.0B to $12.5B means that if oil prices unexpectedly retreat in the second half of the year, higher capital intensity will weigh on free cash flow.

- Geopolitical Double-Edged Sword: While Middle East conflicts drive up oil prices, they have caused tangible disruptions to ConocoPhillips’ LNG operations in Qatar. Monitoring the timeline for capacity recovery in that region is essential.

Source:

- https://hk.investing.com/news/transcripts/article-93CH-1437149

- https://www.conocophillips.com/news-media/story/conocophillips-announces-first-quarter-2026-results-and-quarterly-dividend/

- https://finance.biggo.com/news/US_COP_2026-04-30

- https://simplywall.st/stocks/us/energy/nyse-cop/conocophillips/future

- https://www.tradingview.com/symbols/NYSE-COP/forecast/

Back to ConocoPhilips page