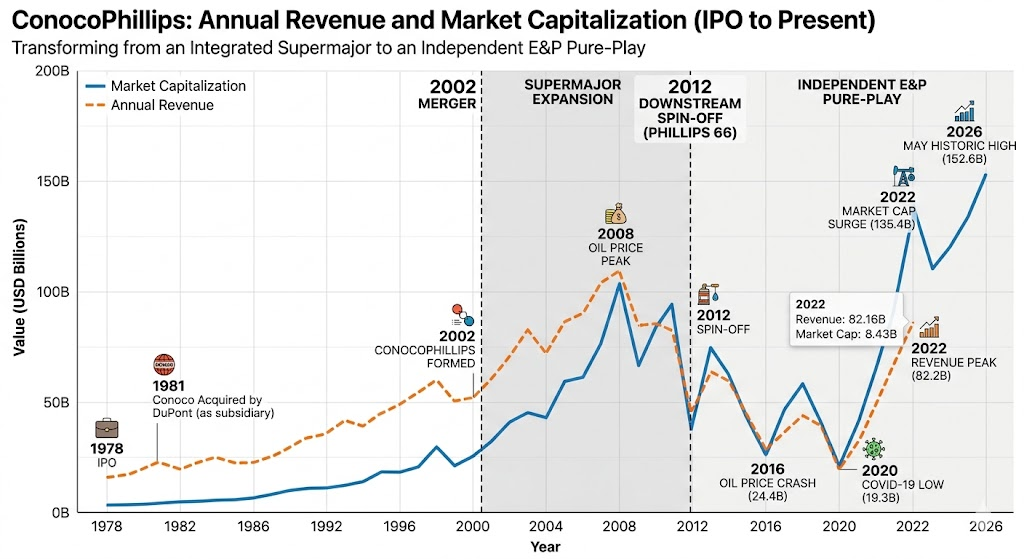

The history of ConocoPhillips is characterized by a long legacy and multiple major transformations, which can be divided into the following four key stages:

Laying the Foundations and the Rise of Two Giants (1875–2001)

The origins of the company date back to the 19th century. Continental Oil Product Company (which later became Conoco) was founded in Utah in 1875, initially distributing kerosene and lubricants. On the other hand, Phillips Petroleum Company was established in Oklahoma in 1917 by the Phillips brothers, expanding rapidly after discovering oil near Bartlesville. Over the following decades, both companies independently grew their refining capacities, retail gas station networks (such as the Phillips 66 brand), and overseas exploration businesses.

Merger of the Century and Full-Chain Expansion (2002–2011)

To enhance international competitiveness and achieve economies of scale, Conoco and Phillips Petroleum officially merged in 2002 to form ConocoPhillips. This mega-merger created the third-largest energy company in the United States at the time and one of the world’s leading integrated supermajors, spanning upstream exploration and production, midstream pipeline transportation, as well as downstream refining and marketing (including the 76 and Phillips 66 brands).

Spinning Off Downstream and Focusing Upstream (2012–2019)

To unlock more market value and optimize its asset structure, the company made a major strategic decision in 2012 to spin off its midstream and downstream refining and marketing businesses into a new, independent publicly traded company named Phillips 66. Following the spin-off, ConocoPhillips became the world’s largest independent exploration and production (E&P) pure-play upstream company, shifting its full focus toward maximizing extraction efficiency and maintaining rigorous capital discipline.

Shale Expansion and Energy Transition (2020–Present)

In recent years, the company has further consolidated its leading position in premier US shale plays through large-scale acquisitions, notably completing the purchase of Concho Resources in 2021 and acquiring Shell’s entire asset portfolio in the Permian Basin. While expanding its low-cost, low-carbon-intensity crude oil and liquefied natural gas (LNG) portfolio, the company has also committed to achieving net-zero operational emissions by 2050.

ConocoPhillips occupies a unique position in the global energy landscape as the world’s largest independent exploration and production (E&P) pure-play upstream company. Its competitive environment is primarily divided into two camps: traditional integrated supermajors and large independent upstream peer companies.

Competitor Classification

The following table provides a comparison of ConocoPhillips’ main peers in the market:

| Competitor Type | Core Companies | Operational Characteristics & Comparison |

| Integrated Supermajors | ExxonMobil ($XOM) Chevron ($CVX) | These giants possess massive downstream refining, chemical, and retail operations, providing greater resilience against oil price volatility. Compared to them, ConocoPhillips lacks downstream hedging but offers higher agility, focus, and capital return efficiency in upstream sectors. |

| Large Independent Upstream Peers | EOG Resources ($EOG) Occidental ($OXY) Devon Energy ($DVN) Diamondback ($FANG) | These companies focus purely on upstream extraction. EOG and Diamondback are heavily concentrated in US shale (such as the Permian Basin), while Occidental incorporates extensive carbon capture (CCUS) and midstream assets. ConocoPhillips stands out with its global asset allocation and significant LNG footprint. |

Core Competitive Advantages of ConocoPhillips

ConocoPhillips maintains its industry leadership through three core pillars:

1. Globally Diversified High-Quality Asset Portfolio

Unlike domestic independent producers that rely solely on US shale (such as Devon or Diamondback), ConocoPhillips boasts a highly diversified asset base. In addition to tier-one acreage in the US Lower 48 (Permian, Eagle Ford, and Bakken), it possesses massive legacy projects in Alaska, along with international deepwater assets and long-term liquefied natural gas (LNG) contracts. This global footprint effectively mitigates the operational risks of relying on a single region.

2. Highly Competitive Low Cost of Supply

ConocoPhillips has long adhered to a rigorous framework of capital discipline, anchoring its average cost of supply for new investments at an exceptionally low level (with many core assets profitable even below $30 to $40 per barrel). Its scale advantage has expanded further following the strategic acquisitions of Concho Resources and Marathon Oil, allowing the company to maintain top-tier margins and free cash flow during periods of oil price volatility.

3. Superior Shareholder Return Mechanism

In balancing volume growth and capital returns, ConocoPhillips leans heavily toward the latter. The company commits to returning around 45% of its cash from operations (CFO) to shareholders through a combination of base dividends, variable return of cash, and share repurchases. Its dividend growth rate and free cash flow yield consistently lead the S&P 500 energy sector.

Strategic and Competitive Challenges

- Lack of Natural Downstream Hedge: During periods of global oil oversupply and collapsing crude prices, integrated majors like ExxonMobil can buffer upstream losses with downstream refining profits. As a pure-play upstream operator, ConocoPhillips takes the full impact of price downturns directly on its top and bottom lines.

- Depletion of Premium US Shale Inventory: As operators aggressively develop the Permian Basin, the race to secure and replenish premium Tier-1 acreage remains fierce. The pace of inventory replacement will dictate the long-term production and cost dynamics between ConocoPhillips and rivals like EOG.

Source:

- https://www.conocophillips.com

- https://www.phillips66.com

- https://www.exxonmobil.com

- https://www.chevron.com

- https://www.eogresources.com

- https://www.oxy.com

- https://www.devonenergy.com

- https://www.diamondbackenergy.com

Back to ConocoPhilips page