The history of Gilead Sciences can be divided into four distinct phases, tracking its evolution from a focused antiviral biotech startup into a global multi-therapeutic pharmaceutical giant.

Phase 1: Foundation and Early Discovery (1987-2000)

- In 1987, the company was founded in California by Michael Riordan, a medical doctor and venture capitalist, initially under the name Oligogen before becoming Gilead Sciences. Early research focused on antisense technology before pivoting to small-molecule antivirals.

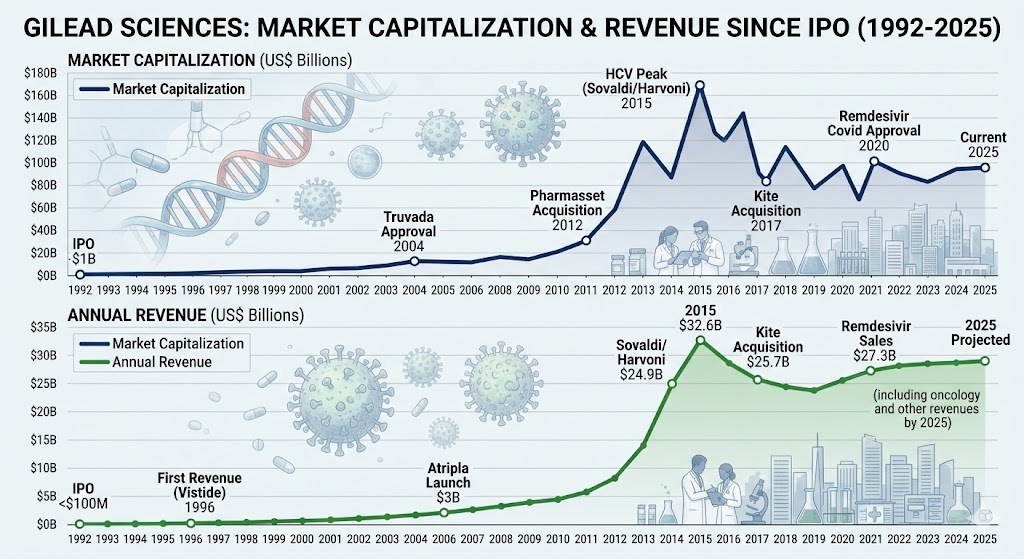

- In 1992, Gilead went public on the NASDAQ, raising 86M.

- In 1996, the company received its first FDA approval for Vistide, a treatment for CMV retinitis in HIV patients. That same year, Gilead licensed Tamiflu (an influenza treatment) to Roche, which later generated massive royalty streams.

- In 1999, the acquisition of NexStar Pharmaceuticals provided Gilead with its first major commercial sales force and European infrastructure.

Phase 2: Establishing HIV Market Dominance (2001-2010)

- In 2001, the landmark drug Viread (tenofovir DF) was approved, becoming the backbone of future HIV combination therapies.

- In 2002, Gilead acquired Triangle Pharmaceuticals, gaining emtricitabine (FTC), which completed their internal combination drug pipeline.

- In 2004, Truvada was launched, combining two key compounds into a single pill.

- In 2006, Gilead introduced Atripla, the world’s first once-daily Single-Tablet Regimen for HIV. This revolutionary cocktail therapy transformed HIV from a fatal disease into a manageable chronic condition, pushing Gilead’s annual revenue past 5B by 2007 and securing absolute leadership in the HIV market.

Phase 3: The Hepatitis C Breakthrough and Revenue Peak (2011-2016)

- In 2011, Gilead made a historic 11B acquisition of Pharmasset, securing the pipeline compound sofosbuvir.

- In 2013 and 2014, the company launched Sovaldi and Harvoni. Boasting cure rates over 95%, these therapies effectively turned Chronic Hepatitis C (HCV) into a completely curable disease, though their high prices sparked global debate.

- In 2015, driven by unprecedented global demand for its HCV cure, Gilead’s annual revenue peaked at a record 32.6B. However, because patients were cured rather than treated long-term, and due to new competitors, HCV revenue began declining rapidly after 2016.

Phase 4: Diversification, Oncology, and the Modern Era (2017-Present)

- In 2017, Gilead acquired Kite Pharma for 11.9B, gaining the CAR-T cell therapy Yescarta and formally establishing its presence in cancer immunotherapy.

- In 2020, the company acquired Immunomedics for 21B, adding the blockbuster Antibody-Drug Conjugate (ADC) Trodelvy for breast cancer, solidifying oncology as its next major growth pillar.

- In 2020, during the COVID-19 pandemic, Veklury (remdesivir) became the first FDA-approved treatment for hospitalized COVID-19 patients, generating over 5B in short-term revenue spikes between 2021 and 2022.

- Moving into 2024-2026, Gilead acquired CymaBay to expand into rare liver diseases while aggressively advancing lenacapavir, a twice-yearly long-acting HIV prevention injectable, balancing its legacy antiviral strength with its expanding oncology pipeline.

Gilead Sciences’ competitive landscape is defined by two distinct market dynamics: defending its high-cash-flow stronghold in the antiviral (HIV) market and aggressively fighting for market share in the crowded, high-growth oncology and cell therapy sectors.

Here is a detailed competitive analysis across Gilead’s primary therapeutic areas:

1. HIV and PrEP Market: The Defensive Stronghold

Gilead dominates the US HIV market with a market share of approximately 70%, driven by its flagship oral regimen Biktarvy, which remains the most prescribed HIV medication globally. However, the market is undergoing a structural shift from daily oral pills to long-acting injectables, sparking intense innovation battles.

- GlaxoSmithKline (GSK / ViiV Healthcare) — The Primary RivalViiV (a joint venture backed by GSK, Pfizer, and Shionogi) is Gilead’s only peer-scale competitor in HIV.

- The Conflict: GSK’s long-acting regimens, Cabenuva (for treatment) and Apretude (a bi-monthly injection for PrEP/prevention), directly challenge Gilead’s oral market share.

- Gilead’s Defense: Gilead launched lenacapavir, a twice-yearly long-acting injectable for PrEP. Its superior six-month dosing window has demonstrated remarkable market penetration capability, projecting robust sales growth into 2026. Gilead is also developing long-acting treatment combinations like Viclen (bictegravir+lenacapavir).

- Merck — The Pipeline DisrupterMerck continues to advance its long-acting nucleoside reverse transcriptase translocation inhibitor, islatravir. While Merck has partnered with Gilead on certain combination studies, it remains a long-term threat to Gilead’s market dominance.

2. Oncology and Cell Therapy Market: Up against Big Pharma

Gilead is executing a strategic pivot toward oncology through multi-billion-dollar acquisitions (such as Kite Pharma and Immunomedics), aiming for cancer therapies to contribute one-third of total revenue by 2030. In this arena, Gilead faces traditional pharmaceutical giants with deeply entrenched clinical networks.

- AstraZeneca / Daiichi Sankyo — The ADC Price WarGilead’s cornerstone Antibody-Drug Conjugate (ADC), Trodelvy (targeting Trop-2), has shown strong growth in triple-negative breast cancer (TNBC) and urothelial carcinoma. However, it faces immense pressure from AstraZeneca and Daiichi Sankyo’s blockbuster ADC, Enhertu. Enhertu’s aggressive clinical expansion into HER2-low indications challenges Trodelvy’s long-term upside in broader solid tumor markets.

- Bristol Myers Squibb (BMS) & Novartis — The CAR-T Street FightGilead’s Kite division leads the cell therapy space with Yescarta and Tecartus, but BMS’s Breyanzi and Novartis’s Kymriah are constantly pushing back.

- The Conflict: The battleground is centered on moving CAR-T into earlier lines of therapy (first- and second-line treatments) and optimizing “vein-to-vein” turnaround manufacturing time. BMS’s capacity expansions and broader label approvals have recently placed structural pricing and volume pressure on Yescarta.

- Johnson & Johnson (J&J) — The New Myeloma FrontierGilead’s partnership with Arcellx on the BCMA-targeting CAR-T asset anito-cel (aiming for an FDA decision by late 2026) positions Gilead to directly challenge J&J and Legend Biotech’s market-leading cell therapy, Carvykti, in multiple myeloma.

3. Liver Disease and Rare Disease Markets: Maximizing Cash & Finding Niches

- AbbVie — The Declining HCV MarketIn the Chronic Hepatitis C (HCV) market, Gilead and AbbVie (Mavyret) split the global remainder of the business. Because these drugs successfully cure patients, the addressable market shrinks every year. This segment has transitioned into a highly profitable cash-cow duopoly with minimal ongoing R&D expenditure.

- The Rare Disease Pivot (Livdelzi)Following the acquisition of CymaBay, Gilead launched Livdelzi for primary biliary cholangitis (PBC). With intercepting challenges facing competitive therapies like Ocaliva, Gilead has secured a lucrative niche liver-disease market with substantial near-term growth runway.

Competitive Summary Matrix

| Therapeutic Area | Core Competitive Moat | Primary Competitors | Key Battlegrounds (2026+) |

| HIV / PrEP | >70% market share, high genetic resistance barrier, 6-month dosing of lenacapavir. | GSK (ViiV) | Six-month long-acting injectables vs. bi-monthly regimens. |

| ADC Oncology | First-mover advantage in TNBC; distinct mechanism of action. | AstraZeneca, Roche | Moving Trodelvy into first-line breast cancer and expanding into non-small cell lung cancer. |

| CAR-T Cell Therapy | Best-in-class commercial manufacturing scale and institutional footprint. | BMS, Novartis, J&J | Commercial launch of anito-cel in multiple myeloma and manufacturing turnaround speed. |

Source:

- https://www.gilead.com/news/news-details/2026/gilead-sciences-announces-first-quarter-financial-results

- https://www.marketbeat.com/earnings/reports/2026-2-10-gilead-sciences-inc-stock/

- https://medicineslawandpolicy.org/2025/06/fda-approval-of-injectable-lenacapavir-for-pre-exposure-prophylaxis-prep-opens-the-road-to-ending-hiv/

- https://www.gilead.com/news/news-details/2026/u-s–fda-grants-priority-review-of-new-drug-application-for-gileads-once-daily-hiv-treatment-of-bictegravir-plus-lenacapavir

- https://www.gilead.com/news/news-details/2026/gilead-sciences-completes-acquisition-of-arcellx-ahead-of-potential-commercial-launch-of-anito-cel

- https://www.cellgenetherapyreview.com/3972-News/625422-Gilead-completes-Arcellx-acquisition/

- https://www.drugs.com/history/livdelzi.html

- https://www.ema.europa.eu/en/medicines/human/EPAR/lyvdelzi

Back to Gilead page